PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065505

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065505

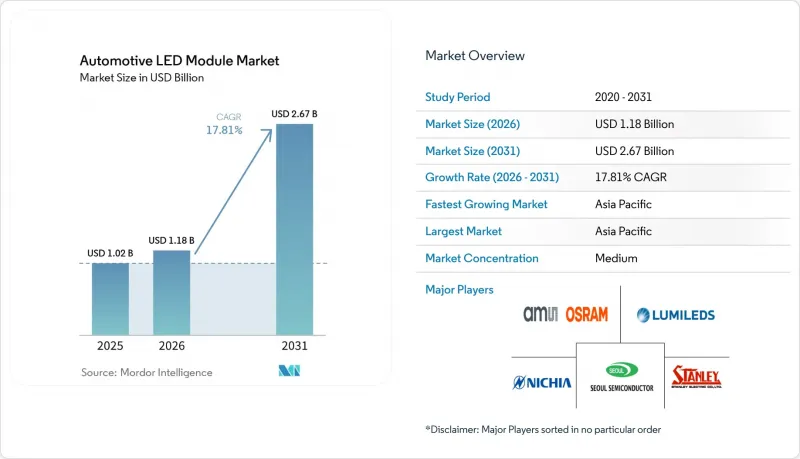

Automotive LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the automotive lED module market size is projected to be USD 1.18 billion in 2026 and reach USD 2.67 billion by 2031, growing at a CAGR of 17.81% from 2026 to 2031.

This report is Segmented by Module Type (COB LED Modules, SMD LED Modules, Matrix/Pixel LED Modules, and More), Lighting Function (Exterior Lighting, Interior Lighting, and More), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive LED Module Market Trends and Insights

Growing Adoption of Advanced Driver-Assistance Systems (ADAS)

Pixel-level beam control prevents camera and LiDAR wash-out, so OEMs are installing high-definition modules with more than 25,000 addressable points. Selective illumination cuts energy use by up to 30% and extends lifetime by reducing thermal stress. Software-programmable beams also enable left- and right-hand-drive compliance without mechanical parts, thereby shortening development cycles. As Level 3 and Level 4 features appear, lighting that communicates vehicle intent to pedestrians becomes essential, further entrenching pixel arrays as the default headlamp technology.

Shift Toward Electric Vehicles Requiring Energy-Efficient Lighting

LED modules draw 40-60 watts versus 110-130 watts for halogens, adding 2-4 kilometers of range per charge in compact EVs. Premium ambient systems now operate at 30% lower power while maintaining color-rendering indices above 95, easing load on battery cooling loops. Every watt saved in lighting is reallocated to drivetrain or climate control, so OEMs specify LEDs on nearly all new electric platforms, pushing both volume and content per vehicle higher.

Thermal Management Challenges in High-Power LED Modules

Currents above 1 ampere push junction temperatures past 150 °C, accelerating lumen loss and shortening life below the 50,000-hour target. Advanced substrates, carbon-nanotube fluids, and active cooling reduce heat but add USD 8-12 per module and increase warranty complexity. Hot climates intensify the problem, forcing premium cars to adopt liquid plates or micro-fans that remain uneconomic for mass models, thereby slowing pixel adoption in volume segments.

Other drivers and restraints analyzed in the detailed report include:

- OEM Preference for Modular, Scalable Lighting Architecture

- Declining LED Cost per Lumen Boosting Penetration

- High Up-Front Tooling Cost for Matrix/Pixel Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMD LED modules accounted for 32.67% of the Automotive LED Module market share in 2025, thanks to mature supply chains and reliable thermal performance. The Automotive LED Module market size for pixel and matrix systems is projected to expand at an 18.47% CAGR, supported by software-defined beams that satisfy UN ECE R149 and NHTSA adaptive rules without mechanical parts. Pixel engines with more than 16,000 micro-LEDs now monitor current and temperature per emitter, enabling predictive maintenance and extending service life. COB packages serve high-intensity spot and fog functions, especially in commercial vehicles where vibration resistance matters more than cost. Laser-assisted hybrids remain niche until phosphor stability and cooling costs improve, with series production slated beyond 2027.

Pixel architectures advance partly because they enable firmware updates that add new animations or communication symbols post-sale, a feature SMD arrays cannot deliver. Suppliers offering integrated driver ICs and sub-0.5 K/W thermal resistance win premium EV programs, while pure SMD assemblers defend volume ICE models but face price compression. The transition timeline hinges on thermal breakthroughs and further cost declines, but the direction toward high-pixel-count modules is clear.

Geography Analysis

Asia Pacific commanded a 68.73% share in 2025 and will advance at a 17.97% CAGR through 2031, as China, Japan, and India together exceed a large amount of global output. Concentrated fabrication of Mini and Micro LED wafers shortens lead times and lowers package costs, reinforcing the region's dominance. Subsidies tied to China's 25% new-energy-vehicle penetration catalyze gains in LED content per car. Japan scales application-processor modules, positioning local plants as hubs for driver ICs and Mini LED backlights used in both interior lighting and cockpit displays. India accelerates tool-heavy rear-lamp programs thanks to new high-tonnage presses capable of two-meter light bars.

North America is catalyzed by consumer appetite for customizable cabins and software-defined vehicle platforms. NHTSA's cautious enforcement of its adaptive-beam rule slows ultra-high pixel counts but ensures stable demand for matrix arrays. Supplier investments cluster near Mexico and the United States to mitigate tariff and logistics risk while serving domestic assembly plants.

Europe sets the regulatory pace with UN ECE R149, allowing matrix beams across the continent under unified testing, encouraging OEMs to fit LEDs even on entry trims to meet CO2 and safety targets. South America and the Middle East show smaller bases but above-average gains, as exporters align with EU lighting standards and regional premium buyers specify LED daytime running lights. Africa remains nascent; premium segments in South Africa adopt LEDs, while mass models still rely on halogen to keep vehicle prices down.

- Nichia Corporation

- Stanley Electric Co., Ltd.

- OSRAM GmbH

- LG Innotek Co., Ltd.

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Valeo SA

- Koito Manufacturing Co., Ltd.

- Hella GmbH & Co. KGaA

- Marelli Holdings Co., Ltd.

- Continental AG

- Denso Corporation

- Hyundai Mobis Co., Ltd.

- Varroc Engineering Limited

- ZKW Group GmbH

- Cree LED, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Advanced Driver-Assistance Systems (ADAS)

- 4.2.2 Shift Toward Electric Vehicles Requiring Energy-Efficient Lighting

- 4.2.3 OEM Preference for Modular, Scalable Lighting Architecture

- 4.2.4 Declining LED Cost per Lumen Boosting Penetration

- 4.2.5 Integration of Dynamic Pixel Lighting for Vehicle-to-X Communication

- 4.2.6 Regional Subsidies for Night-time Road-Safety Technologies

- 4.3 Market Restraints

- 4.3.1 Thermal Management Challenges in High-Power LED Modules

- 4.3.2 High Up-Front Tooling Cost for Matrix/Pixel Platforms

- 4.3.3 Supply-Chain Volatility of Key Phosphor and Epitaxy Materials

- 4.3.4 Regulatory Uncertainty Around Adaptive Beam Standards

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products or Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB LED Modules

- 5.1.2 SMD LED Modules

- 5.1.3 Matrix / Pixel LED Modules

- 5.1.4 Other Module Type (laser-assisted, adaptive modules)

- 5.2 By Lighting Function

- 5.2.1 Exterior Lighting

- 5.2.1.1 Headlamps

- 5.2.1.2 Tail Lamps

- 5.2.1.3 Daytime Running Lights (DRL)

- 5.2.1.4 Others Exterior Lighting

- 5.2.2 Interior Lighting

- 5.2.3 Others Interior Lighting (ambient signature, logo projection)

- 5.2.1 Exterior Lighting

- 5.3 By Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Stanley Electric Co., Ltd.

- 6.4.3 OSRAM GmbH

- 6.4.4 LG Innotek Co., Ltd.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 Valeo SA

- 6.4.9 Koito Manufacturing Co., Ltd.

- 6.4.10 Hella GmbH & Co. KGaA

- 6.4.11 Marelli Holdings Co., Ltd.

- 6.4.12 Continental AG

- 6.4.13 Denso Corporation

- 6.4.14 Hyundai Mobis Co., Ltd.

- 6.4.15 Varroc Engineering Limited

- 6.4.16 ZKW Group GmbH

- 6.4.17 Cree LED, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment