PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061728

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061728

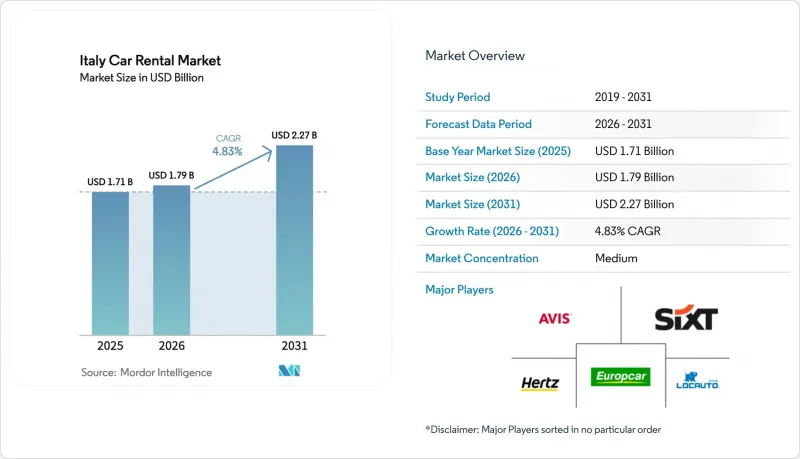

Italy Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the italian car rental market size is expected to increase from USD 1.71 billion in 2025 to USD 1.79 billion in 2026 and reach USD 2.27 billion by 2031, growing at a CAGR of 4.83% over 2026-2031.

This report is Segmented by Booking Mode (Offline and Online), Application (Leisure and Business), End User (Self-Drive Individual, Chauffeur-Drive, and More), Vehicle Type (Mini and Economy Cars, and More), Rental Length (Short-Term, Medium-Term, and Long-Term), and Geography (Northern Italy, Central Italy, Southern Italy and Islands). The Market Forecasts are Provided in Terms of Value (USD).

Italy Car Rental Market Trends and Insights

Tourism Rebound And Pent-Up Travel Demand

International arrivals rose 6.8% in Q4 2024 to 250.1 million overnight stays, lengthening the high season beyond July-August. Fleet utilization benefits from higher shoulder-month volumes, helping to avoid winter troughs that previously dipped significantly. The leisure segment, projected to capture a significant revenue share and achieve steady growth, is banking on maintaining its visitor momentum. In response to new transparency regulations, operators are now packaging fuel and insurance into flat-rate deals, enhancing average ticket values. While rising airfare and lodging costs might dampen discretionary travel, a surge in pent-up demand and the rise of flexible work patterns are bolstering off-peak bookings.

Corporate Travel Recovery In Key Italian Business Hubs

Rental transaction volumes remain below the pre-crisis baseline, while spending per rental has increased significantly, reflecting a robust shift towards premium EV adoption. Multinational corporations are consolidating their procurement strategies, favoring nationwide networks that seamlessly integrate with SAP Concur for automated expense tracking. While Milan's Malpensa and Rome's Fiumicino airports continue to serve as primary hubs, Bologna and Turin are emerging as popular alternatives as companies decentralize their offices. Mid-tier independent firms, often with fragmented operations, are feeling the squeeze from corporate volume discounts. The trajectory of growth assumptions hinges on the stabilization of hybrid work models, rather than any further contraction.

Seasonality And Demand Concentration

In recent months, overnight stays have increased significantly. However, during the winter, utilization lagged and remained low. Operators, facing peak summer demands, found themselves with idle fleets during the winter months. This not only squeezed their profit margins but also compelled them to offer steep discounts. While southern islands experienced high utilization rates during the summer, they dropped significantly in the winter. This drastic shift incurred repositioning costs as vehicles were moved northward to meet rising demand. The significant revenue share from short-term rentals amplifies market volatility. This instability is expected to persist until subscriptions and long-term leases stabilize the demand curves.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Omni-Channel and App-Based Booking Platforms

- Rise of EV Rentals Driven By ZTL Incentives

- High Fleet Procurement and Insurance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online reservations accounted for 54.76% of the Italian car rental market share in 2025, rising at 7.11% CAGR to 2031 as smartphone penetration and metasearch transparency shift buyer behavior. Offline counters are projected to see their market share dip, though modest growth is expected. While commission pressures from aggregators are squeezing near-term margins, direct-app incentives and loyalty tiers are strategically positioned to reclaim that lost value.

Digital fee disclosures, in line with AGCM directives, are bolstering trust and accelerating adoption. Airports remain a stronghold for physical counters, accounting for a significant portion of transactions, underscoring the need for a hybrid operational model. By reallocating staff from traditional desks to kerbside meet-and-greet services, operators are successfully reducing queue times and transitioning upsell opportunities to app notifications. Bolstered by dynamic pricing algorithms and in-app ancillary bundling, the Italian car rental market's digital channel revenue is set to grow significantly.

Leisure use accounted for 64.11% of the Italian car rental market share in 2025 and will expand at a 7.44% CAGR, driven by growth in foreign overnights and broader shoulder seasons. Business rentals, although experiencing modest growth, are yielding higher daily returns as corporations increasingly opt for premium EVs aligned with ESG standards.

Key airport corridors, including Malpensa-Milan, Fiumicino-Rome, and Venice Marco Polo, dominate dual-purpose travel. Operators strategically segment their fleets: offering economy cars for families and connectivity-enhanced sedans for executives, ensuring neither under- nor over-sizing. While leisure's share of the Italian car rental market may increase slightly, it's the growth in business rentals that bolsters profitability and fuels vendor consolidation deals.

List of Companies Covered in this Report:

- EUROPCAR INTERNATIONAL SASU

- The Hertz Corporation

- Avis Rent A Car System, LLC

- Sixt SE

- Locauto Group

- Drivalia (Leasys Rent)

- Maggiore

- Goldcar Italy

- Sicily by Car

- Autovia

- Noleggiare

- B-Rent

- Rent Smart24

- Surprice Car Rentals Italy

- Enjoy (ENI)

- Share Now Italy

- Free2Move

- Enterprise-Alamo National Italy

- GreenMotion Italy

- Euronoleggio

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tourism Rebound and Pent-Up Travel Demand

- 4.2.2 Corporate Travel Recovery in Key Italian Business Hubs

- 4.2.3 Expansion Of Omni-Channel and App-Based Booking Platforms

- 4.2.4 Rise Of EV Rentals Driven by ZTL (Restricted-Traffic) Incentives

- 4.2.5 Sustainability-Linked Corporate Fleet Agreements

- 4.2.6 Mobility-As-A-Service Subscription Models Gaining Traction

- 4.3 Market Restraints

- 4.3.1 Seasonality and Demand Concentration

- 4.3.2 High Fleet Procurement and Insurance Costs

- 4.3.3 Competition From Ride-Hailing and Shared-Mobility Options

- 4.3.4 Semiconductor Shortage Delaying Vehicle Renewals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Booking Mode

- 5.1.1 Offline

- 5.1.2 Online

- 5.2 By Application

- 5.2.1 Leisure

- 5.2.2 Business

- 5.3 By End User

- 5.3.1 Self-Drive Individual

- 5.3.2 Chauffeur-Drive

- 5.3.3 Corporate Fleet Subscription

- 5.3.4 Peer-to-Peer Rental

- 5.4 By Vehicle Type

- 5.4.1 Mini and Economy Cars

- 5.4.2 Compact and Intermediate Cars

- 5.4.3 Standard and Full-Size Cars

- 5.4.4 SUVs and MPVs

- 5.4.5 Luxury / Premium Cars

- 5.5 By Rental Length

- 5.5.1 Short-Term (Less than 30 days)

- 5.5.2 Medium-Term (1-12 months)

- 5.5.3 Long-Term (Above 12 months)

- 5.6 By Region

- 5.6.1 Northern Italy

- 5.6.2 Central Italy

- 5.6.3 Southern Italy and Islands

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 EUROPCAR INTERNATIONAL SASU

- 6.4.2 The Hertz Corporation

- 6.4.3 Avis Rent A Car System, LLC

- 6.4.4 Sixt SE

- 6.4.5 Locauto Group

- 6.4.6 Drivalia (Leasys Rent)

- 6.4.7 Maggiore

- 6.4.8 Goldcar Italy

- 6.4.9 Sicily by Car

- 6.4.10 Autovia

- 6.4.11 Noleggiare

- 6.4.12 B-Rent

- 6.4.13 Rent Smart24

- 6.4.14 Surprice Car Rentals Italy

- 6.4.15 Enjoy (ENI)

- 6.4.16 Share Now Italy

- 6.4.17 Free2Move

- 6.4.18 Enterprise-Alamo National Italy

- 6.4.19 GreenMotion Italy

- 6.4.20 Euronoleggio

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment