PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061769

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061769

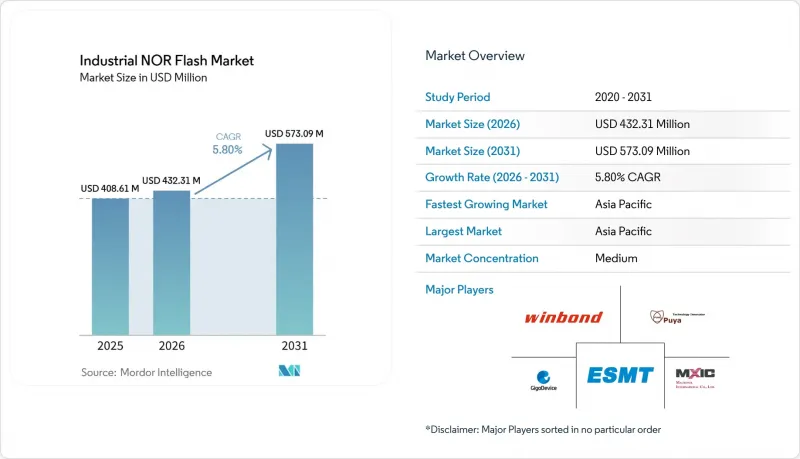

Industrial NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the industrial nOR flash market size is expected to increase from USD 408.61 million in 2025 to USD 432.31 million in 2026 and reach USD 573.09 million by 2031, growing at a CAGR of 5.80% over 2026-2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, 1. 8V Class, and More), Process Technology Node (65 Nm, 45 Nm, and More), Packaging Type (WLCSP/CSP, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Industrial NOR Flash Market Trends and Insights

Quad And Octal SPI Adoption Unlocking Higher Throughput at the IoT Edge

Quad SPI already supports a large installed base of code-storage sockets, and the move toward Octal SPI and xSPI is raising sustained read bandwidth to 400 MB/s for edge platforms that need faster boot and execution behavior. GigaDevice launched its GD25NX series in November 2025 with a 1.8 V core and 1.2 V I/O design, and the company said the product delivered 30% faster programming speed and 10% shorter erase time than conventional 1.8 V octal flash in 200 MHz double transfer rate mode. In the industrial NOR flash market, this shift matters because larger firmware images are making bandwidth a more visible design bottleneck than raw capacity in many AI edge nodes. Vendors that combine xSPI support with execute-in-place behavior are extending the role of NOR flash into applications that previously leaned on external SRAM to keep response times low. That is tightening platform qualification windows and giving an advantage to suppliers that already have certified high-speed portfolios in the industrial NOR flash market.

China 55 Nm And 40 Nm Indigenous Process Reshaping The Supply Equilibrium

China is reshaping the supply side of the industrial NOR flash market by expanding local production at 55 nm and 40 nm, with the goal of reducing dependence on Taiwan-based and U.S.-linked sources. Wuhan XMC had its IPO application accepted by the Shanghai STAR Market in September 2024, and the company offers foundry services for NOR flash at 40 nm and above. GigaDevice and Puya are also broadening domestic supply options, which is increasing the strategic weight of local sourcing in standard and mid-density products. This build-out is not only replacing imports, but it is also creating a parallel pricing environment that is more aggressive in commodity tiers than in premium categories. The industrial NOR flash market is therefore becoming more clearly split between price-led domestic supply and qualification-led premium supply, where safety, security, and long design history still matter more than price alone.

Cost Premium Over NAND Constraining Adoption At The Density Ceiling

The industrial NOR flash market still faces a structural cost-per-bit disadvantage against NAND once density requirements exceed 256 Mb, which limits adoption in designs where storage economics matter more than fast random read access. The 2D NOR roadmap also remains difficult beyond 45 nm, and meaningful density scaling would require more advanced structures that are still far from broad-volume deployment. Macronix delayed its 3D NOR development program by about 2 years in 2026 to redirect resources toward supply-constrained mid-density NOR and eMMC products. That decision highlights the trade-off between long-term scaling investments and near-term revenue opportunities in segments that are already supply-constrained. The result is a dual-track industrial NOR flash market where 128-512 Mb products continue to grow in infrastructure, industrial, and automotive applications, but low-density consumer volumes are harder to expand when NAND alternatives are cheaper.

Other drivers and restraints analyzed in the detailed report include:

- Secure-Boot And OTA-Update Mandates Creating Compliance-Driven Demand Pull

- Constellation-Scale LEO Satellites Creating A Durable Premium-ASP Pocket

- Scaling Ceilings Opening Architectural Entry Points For MRAM And ReRAM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR flash held 66.1% of the industrial NOR flash market size in 2025 and is projected to grow at a 6.7% CAGR through 2031. Its lead reflects the preference of current IoT and automotive SoCs for low-pin-count serial interfaces that support execute-in-place without a dedicated memory bus. The industrial NOR flash market has moved steadily toward serial designs, as they better fit tighter board layouts and lower power budgets in new products. GigaDevice said its GD25NX xSPI NOR series achieved 400 MB/s throughput and reduced read power by up to 50% compared with conventional 1.8 V octal alternatives.

Parallel NOR flash is losing share, but it still retains a durable position in legacy programmable logic controllers, selected defense electronics, and some automotive safety modules. Those sockets often need synchronous parallel access and a wide bus width, and they also tend to stay in service for many years after initial qualification. That gives parallel products a stable revenue floor even as most new designs in the industrial NOR flash industry move to serial architectures. The overall pattern shows a market where serial dominates new demand, while parallel remains relevant in applications that value continuity and proven fit over redesign.

Quad SPI accounted for 52.3% of the industrial NOR flash market share in 2025 because it offered the best balance between bandwidth, board simplicity, and controller compatibility. It remains the default choice across a wide installed base of industrial edge devices and microcontroller platforms. JEDEC standardization has supported this position by giving equipment makers a clear framework for serial flash interoperability. The SPI Single and Dual category still serves low-density and cost-sensitive sockets where legacy designs are not being refreshed quickly.

Octal and xSPI are the fastest-growing interface segments, with a 6.9% CAGR projected through 2031. That growth reflects demand from AI inference nodes and automotive domain controllers that need instant-on behavior and higher sustained read speed. In the industrial NOR flash market, vendors that embed ECC and CRC features into octal products are improving their chances in automotive safety programs where external support logic adds cost and design complexity. JEDEC xSPI protocol alignment is also becoming a practical gatekeeper for premium platform qualification. Vendors without a credible xSPI roadmap are likely to stay concentrated in standard sockets rather than the highest-margin part of the industrial NOR flash market.

Geography Analysis

Asia-Pacific held 55.2% of the industrial NOR flash market share in 2025 and is projected to grow at a 7.2% CAGR through 2031, which keeps it firmly in the lead by both production scale and demand depth. China remains the largest domestic demand center in the region and is also the most active supply-side challenger, as local players expand 55 nm and 40 nm production for domestic self-sufficiency. Taiwan continues to anchor the IDM base in the industrial NOR flash market, and Winbond was reported to hold 23% of global NOR flash revenue while targeting a 30%-40% rise in NOR flash shipments in 2026. Macronix also restarted a TWD 22 billion (USD 699.1 million) investment plan to expand 12-inch factory output by 50% in 2026. Japan and South Korea add stable demand through automotive and industrial electronics, while India and Southeast Asia are becoming more important as electronics assembly expands under China-plus-one procurement strategies.

North America and Europe together form the second-largest demand block, and this part of the industrial NOR flash market is defined more by application value than by manufacturing scale. Demand is concentrated in automotive ADAS, defense, aerospace, and industrial automation, which supports higher average selling prices than standard consumer-driven memory segments. Infineon has reinforced this position with ASIL-D-aligned SEMPER NOR products and its 512 Mbit QML-qualified radiation-hardened NOR flash for space programs. Europe also benefits from a dense base of connected industrial equipment, and the Cyber Resilience Act is increasing procurement of secure NOR flash across the region's industrial device ecosystem.

The Rest of the World remains smaller, but it is still adding new demand in telecommunications infrastructure and industrial IoT deployments. Each 4G and 5G base station rollout creates an incremental need for NOR flash to store boot firmware and system configuration in network equipment. The Middle East is also becoming a meaningful secondary outlet for ruggedized industrial electronics tied to oil and gas automation and smart city programs. South America is more closely linked to electronics assembly and appliance manufacturing, so its growth tends to follow broader global demand shifts rather than define them within the industrial NOR flash market.

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC Co. Ltd.

- Zbit Semiconductor Inc.

- Eon Silicon Solution Inc.

- Integrated Silicon Solution Inc.

- Alliance Memory Inc.

- AMIC Technology Corp.

- XTX Technology (Shenzhen) Ltd.

- Fudan Microelectronics Group Co. Ltd.

- Giantec Semiconductor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Quad/Octal SPI Adoption for Fast-Boot IoT Edge Devices across Global Manufacturing Hubs

- 4.2.2 Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- 4.2.3 China 55 nm and 40 nm Indigenous Process Push for NOR Self-Sufficiency

- 4.2.4 Secure-Boot and OTA-Update Mandates in Industry 4.0 Factories

- 4.2.5 Low-Power 1.8 V Serial NOR for Wearable and Point-of-Care Healthcare Electronics

- 4.2.6 Real-Time Sensor Fusion in Autonomous Mobile Robots Driving Demand for 128-512 Mb NOR

- 4.3 Market Restraints

- 4.3.1 Cost Premium over NAND above 256 Mb Limiting High-Density Consumer Adoption

- 4.3.2 Scaling Ceilings beyond 45 nm Steering OEM Roadmaps toward MRAM / ReRAM Substitutes

- 4.3.3 Foundry Concentration in Taiwan Exposing Supply-Chain Disruption Risk

- 4.3.4 ASP Compression from Expanding Chinese Capacity Impacting Vendor Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory and Technological Outlook

- 4.7 Reliability and Qualification Standards Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65-3.6 V)

- 5.4.4 <=1.2 V and Other Specialty Voltages

- 5.5 By Process Technology Node (Value)

- 5.5.1 90 nm and More

- 5.5.2 65 nm

- 5.5.3 55 nm (incl. 58 nm)

- 5.5.4 45 nm

- 5.5.5 28 nm and Below

- 5.6 By Packaging Type (Value)

- 5.6.1 WLCSP / CSP

- 5.6.2 QFN / SOIC

- 5.6.3 BGA / FBGA

- 5.6.4 Other Industrial Grade Packages

- 5.7 By Geography (Value, Volume)

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 France

- 5.7.2.3 United Kingdom

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 South Korea

- 5.7.3.4 Taiwan

- 5.7.3.5 India

- 5.7.3.6 South East Asia

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 Rest of the World

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.5 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.6 Wuhan XMC Co. Ltd.

- 6.4.7 Zbit Semiconductor Inc.

- 6.4.8 Eon Silicon Solution Inc.

- 6.4.9 Integrated Silicon Solution Inc.

- 6.4.10 Alliance Memory Inc.

- 6.4.11 AMIC Technology Corp.

- 6.4.12 XTX Technology (Shenzhen) Ltd.

- 6.4.13 Fudan Microelectronics Group Co. Ltd.

- 6.4.14 Giantec Semiconductor Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis