PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061786

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061786

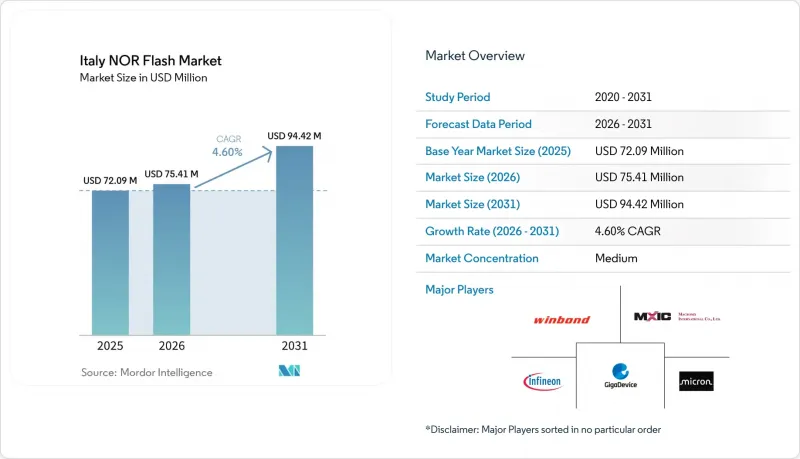

Italy NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the italy nOR flash market size is expected to increase from USD 72.09 million in 2025 to USD 75.41 million in 2026 and reach USD 94.42 million by 2031, growing at a CAGR of 4.60% over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, Parallel NOR Flash), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, and More), End-User Application (Communication, and More), Process Node (90nm and Older, and More), Packaging Type (WLCSP/CSP, and More), and Geography (Italy). Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Italy NOR Flash Market Trends and Insights

Expansion of ADAS and Autonomous Platforms in Italian Automotive OEMs

Stellantis joined the AI4I consortium in 2026, locking in co-development paths that embed NOR Flash into next-generation zonal controllers. The group already demonstrated Level 3 capabilities in late 2025 and earmarked USD 10 billion in semiconductor sourcing to 2030, including 256 Megabit-plus devices for deterministic boot. Ferrari and Lamborghini follow similar roadmaps, integrating predictive maintenance stacks that also demand secure, instant-on storage. Parallel NOR Flash thus gains favor because its fixed-latency read path satisfies ISO 26262 ASIL-D worst-case execution targets. The shift to octal 200 MHz buses delivers 400 MB/s throughput, reducing OTA downtime from hours to minutes and enhancing dealer service economics.

Growing Deployment of Smart Energy Meters by Italian Utilities

Enel's Open Meter II program, backed by a EUR 500 million (USD 540 million) European Investment Bank loan, targets 41 million endpoints with automotive-grade Serial NOR inside each meter. A2A's 1.3 million-unit rollout in Milan and Brescia follows the same architecture. Second-generation meters operate from -25 °C to +70 °C and require 100,000 program-erase cycles plus 20-year retention, specifications aligned with AEC-Q100 Grade 1 Flash. As the regulator ARERA pushes the remaining meters toward a 2027 deadline, demand concentrates in Lombardy, Lazio, and Emilia-Romagna. Suppliers able to certify wide-temperature, low-pin-count devices gain a durable advantage.

High Front-End Fab Costs Versus Limited Domestic Wafer Capacity

Italy depends on Asian foundries whose allocation rules favor higher-volume customers. European fabs sit at a 20-30% cost disadvantage, and the EU NanoIC pilot line remains focused on 5 nm nodes, not used for NOR Flash. The cancellation of Intel's Magdeburg megafab further underscores regional fragility, while STMicroelectronics' EUR 5 billion (USD 5.40 billion) SiC campus focuses on power devices rather than memory. Consequently, local integrators face longer lead times and higher purchasing costs, eroding competitiveness in export-oriented machinery.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Industrial IoT Under Transizione 4.0

- Rising Demand for Secure OTA Updates in Connected Two-Wheelers

- Stringent EU REACH and RoHS Compliance Raising Qualification Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Parallel NOR accounted for a smaller share of the Italian NOR Flash market in 2025, yet its 7.40% CAGR underscores rising demand for advanced driver assistance systems. Automotive domain controllers cannot tolerate boot latency above 100 ms, so deterministic read performance takes precedence over pin-count savings. Infineon and Winbond both released AEC-Q100 Grade 1 Parallel devices that sustain instant-on operation at 150 °C junction temperatures. Serial NOR remains indispensable for compact telematics and wearables, but its market growth rate lags because safety-critical modules are moving to wider buses.

Parallel NOR also benefits from execute-in-place firmware execution, reducing cost by eliminating external DRAM in safety islands. As Stellantis consolidates 30-plus control units into zonal architectures, each node requires dual-redundant Parallel NOR banks for A/B firmware images. Conversely, the SKU diversity of Serial NOR ensures it will keep at least half of total unit shipments, covering industrial sensors and smart meters that value low cost per pin and streamlined PCB routing.

Quad SPI owns the largest slice of the Italian NOR Flash market share, yet its 40.90% position is set to erode as Octal and xSPI climb at 9.60% CAGR. GigaDevice's GD25NX line pushes 400 MB/s read speeds at 200 MHz, a fivefold leap over legacy Dual SPI. Italian OEMs adopt these parts to slash OTA update time and cellular data-plan costs. Stellantis benchmarks show a 2 GB firmware package downloading in under six minutes when hosted on xSPI Flash compared with 30 minutes on Quad SPI.

Standard and Dual SPI continue in set-top boxes and industrial controllers with annual code revisions. However, as UN R155 mandates secure update pipelines, the xSPI protocol's 8-bit DDR signaling plus side-band pins for authentication become persuasive features. Microcontroller vendors such as Renesas now ship reference designs pairing automotive MCUs with on-board Octal Flash pre-loaded with secure-boot loaders, smoothing adoption across Tier 1 suppliers.

Italy NOR Flash market size data show 32 Megabit-and-smaller devices dominate volume, especially in smart meters and industrial gateways. Still, the 256 Megabit bracket advances 7.20% per year as ADAS stacks swell. Infineon's Semper family offers 25-year data retention or 1 million cycle endurance on the same die, de-risking long field life. Tier 1 suppliers now dual-source 256 Megabit xSPI Flash for both infotainment and safety islands, reducing qualification overhead.

As data rates rise from 512 Megabits to 1 Gigabit, discussions intensify over the cost-per-bit between NOR and NAND. NOR technology continues to hold its ground due to its ability to meet the stringent requirements of random-read stability and execute-in-place functionalities, which are critical in ASIL-D environments. These features make NOR a reliable choice for applications where safety and performance cannot be compromised. Italian OEMs have strategically adopted a dual-storage approach, securing the primary boot process in NOR to ensure deterministic and reliable start-up. Meanwhile, they utilize NAND for storing bulk map data, capitalizing on its high-capacity storage capabilities. This combination allows manufacturers to balance performance, cost, and storage efficiency effectively.

List of Companies Covered in this Report:

- Infineon Technologies AG

- Micron Technology Inc.

- GigaDevice Semiconductor Inc.

- Macronix International Co. Ltd

- Winbond Electronics Corp.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC

- Puya Semiconductor Co. Ltd.

- STMicroelectronics N.V.

- ISSI Italia S.r.l.

- SK hynix Inc.

- Powerchip Semiconductor Manufacturing Corporation

- AMIC Technology Corporation

- EON Silicon Solution Inc.

- Espressif Systems Shanghai Co. Ltd.

- Elite Memory Systems S.r.l.

- PUFsecurity Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of ADAS and Autonomous Platforms in Italian Automotive OEMs

- 4.2.2 Growing Deployment of Smart Energy Meters by Italian Utilities

- 4.2.3 Transition of Italian Broadcasting Infrastructure to DVB-T2 Firmware Upgrades

- 4.2.4 Government Incentives for Industrial IoT under Transizione 4.0

- 4.2.5 Rising Demand for Secure OTA Updates in Connected Two-Wheelers

- 4.2.6 Miniaturization Push in Italian Medical Device Start-Ups Wearables

- 4.3 Market Restraints

- 4.3.1 High Front-End Fab Costs vs Limited Domestic Wafer Capacity

- 4.3.2 Stringent EU REACH/RoHS Compliance Raising Qualification Costs

- 4.3.3 Skill Shortages in Embedded NOR Flash Design in Italian SMEs

- 4.3.4 Euro Depreciation Volatility Affecting Memory Component Pricing

- 4.4 Industry Value and Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less NOR

- 5.3.2 4 Megabit and Less NOR greater than 2 Mb

- 5.3.3 8 Megabit and Less NOR greater than 4 Mb

- 5.3.4 16 Megabit and Less NOR greater than 8 Mb

- 5.3.5 32 Megabit and Less NOR greater than 16 Mb

- 5.3.6 64 Megabit and Less NOR greater than 32 Mb

- 5.3.7 128 Megabit and Less NOR greater than 64 Mb

- 5.3.8 256 Megabit and Less NOR greater than 128 Mb

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage 1.65 V - 3.6 V

- 5.4.4 Other Voltage Classes 1.2 V 2.5 V 5 V

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm including 58 nm

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles

- 6.4.1 Infineon Technologies AG

- 6.4.2 Micron Technology Inc.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Macronix International Co. Ltd

- 6.4.5 Winbond Electronics Corp.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Wuhan XMC

- 6.4.11 Puya Semiconductor Co. Ltd.

- 6.4.12 STMicroelectronics N.V.

- 6.4.13 ISSI Italia S.r.l.

- 6.4.14 SK hynix Inc.

- 6.4.15 Powerchip Semiconductor Manufacturing Corporation

- 6.4.16 AMIC Technology Corporation

- 6.4.17 EON Silicon Solution Inc.

- 6.4.18 Espressif Systems Shanghai Co. Ltd.

- 6.4.19 Elite Memory Systems S.r.l.

- 6.4.20 PUFsecurity Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment