PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061770

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061770

NOR Flash For Consumer Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

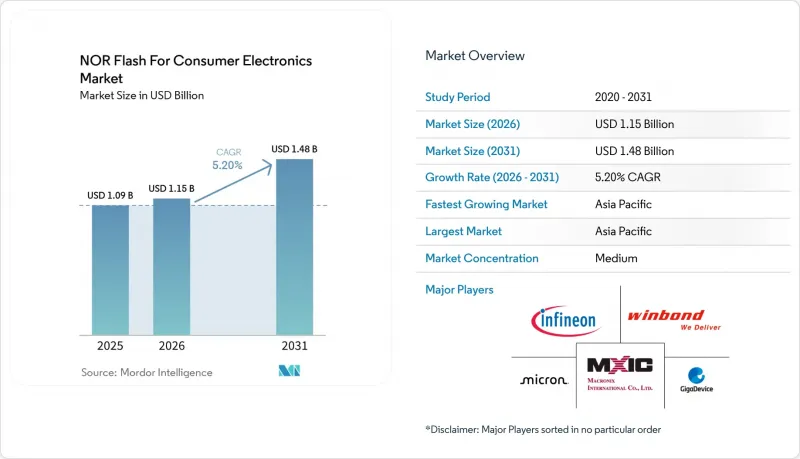

According to Mordor Intelligence, the nOR flash for consumer electronics market size is expected to increase from USD 1.09 billion in 2025 to USD 1.15 billion in 2026 and reach USD 1.48 billion by 2031, growing at a CAGR of 5.20% over 2026-2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Density (2 Megabit and Less, and More), Voltage (3V Class, 1. 8V Class, and More), Process Technology Node (55/58 Nm, 65 Nm, and More), Packaging Type (WLCSP/CSP, QFN/SOIC, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global NOR Flash For Consumer Electronics Market Trends and Insights

Edge-AI IoT Appliances Adopting XiP Architecture Favor High-Density Serial NOR

The NOR flash market for consumer electronics is benefiting from a broader base of edge-AI appliances, such as smart displays, ambient computing hubs, and connected home cameras, that require code storage with fast boot performance. These products are moving toward in-place execution of memory because firmware and inference-related functions need to remain accessible without excessive RAM overhead, which makes high-density serial NOR more attractive in the design cycle. The product direction also favors suppliers that can combine higher densities with low-voltage operation and compact footprints for miniaturized consumer hardware. GigaDevice expanded its GD25UF 1.2 V ultra-low-power SPI NOR flash family in March 2026 to cover 8 Mb to 256 Mb densities and positioned the series for AI computing, wearables, hearables, and ASIC-based platforms. That kind of product expansion supports the view that the NOR flash for the consumer electronics market is shifting toward denser serial devices with better power efficiency rather than basic code-storage parts with limited performance headroom.

Proliferation of Voice-First Smart-Home Hubs Requiring Instant-On Firmware

The NOR flash for the consumer electronics market is also supported by voice-first smart-home devices that need local firmware to stay available for near-instant response after wake events. Smart speakers, display hubs, AI doorbells, and smart plugs depend on code storage that can support fast start-up without the longer load sequence associated with other memory types. This demand pattern matters because many brands now manage several assistant ecosystems on related hardware platforms, which raises the amount of firmware support each design must carry. Winbond identified smart home as a key growth area in its investor materials and stated that its F45 nm process improved die-size efficiency for TWS and IoT applications compared with the older F58 nm generation. Winbond also reported that consumer electronics represented 29% of its 2025 application mix, showing that these device categories remain commercially important to the NOR flash for consumer electronics market and to the leading supplier base.

Cost Premium Versus NAND Above 256 Mb Limiting High-Resolution Camera Adoption

The NOR flash for the consumer electronics market still faces a practical density limit in applications where code storage needs move well beyond 256 Mb. High-resolution camera modules in smartphones, action cameras, and home surveillance products can quickly push memory requirements into a range where NAND remains more cost-effective for larger payloads. That cost gap reduces NOR usage in imaging-heavy device designs even when fast boot characteristics still matter at system level. Macronix stated in its 2024 annual report that its 3D NOR development is intended to improve cost and density positioning, and the company discussed sampling in the second half of 2026 with mass production targeted for 2027. Until such products reach broader commercial use, the NOR flash for the consumer electronics market is likely to remain strongest in low to mid-density code storage rather than in the highest-capacity imaging-related memory needs.

Other drivers and restraints analyzed in the detailed report include:

- Secure-Boot and OTA-Update Mandates in Connected TVs and Gaming Consoles

- China's 55 nm and 40 nm Localization Push Supporting Mid-Density NOR for Smartphones

- ASP Compression From Rising Chinese Capacity Pressuring Vendor Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR commanded 80.4% of the 2025 NOR flash for the consumer electronics market share and is also the fastest-growing type segment, with a projected 6.7% CAGR through 2031. This lead reflects how completely consumer platform design has moved away from parallel memory controllers in current SoC roadmaps. Serial configurations use fewer traces, fit better into tighter board layouts, and align more closely with the low-voltage operating conditions now common in smart speakers, wearables, streaming devices, and connected home products. These traits keep serial NOR at the center of the NOR flash market for consumer electronics, as brands seek smaller, lower-power, and easier-to-qualify memory solutions for high-volume products.

Winbond's 2025 annual results showed that flash memory accounted for 35% of the company's revenue, consistent with the large role of serial NOR in its portfolio and the weight of code-storage products in consumer electronics demand. The category is also helped by stronger adoption in AI-capable household devices, where firmware is expanding as voice, vision, and local processing features are added. Parallel NOR still serves older set-top boxes, fixed-function appliances, and simple remote-control designs where redesign costs are hard to justify. Even so, that installed base is gradually shrinking because newer silicon generations do not prioritize parallel memory support, which limits the long-term room for legacy formats in the NOR flash for consumer electronics market. The direction of travel remains clear, with serial products carrying both the volume base and the forward product roadmap for most modern consumer device designs.

Quad SPI accounted for 42.3% of the 2025 NOR flash market share in consumer electronics and remained the standard interface for a broad range of mid-range devices. It serves smartphones, smart TVs, gaming accessories, and streaming hardware that require higher throughput than single- or dual-SPI can provide without moving to the higher cost and tighter design requirements of full Octal support. The wide controller compatibility of Quad SPI reduces integration risk for OEMs and helps shorten qualification cycles in products with large annual volumes. This keeps Quad SPI firmly positioned as the workhorse interface across the NOR flash for the consumer electronics market.

At the performance end, Octal and xSPI are forecast to grow at a 6.9% CAGR through 2031 as devices demand faster boot times and higher execution speeds for advanced firmware. GigaDevice launched the GD25NX series in November 2025 with a dual-voltage design, 200 MHz Octal SPI support, throughput up to 400 MB/s, and a stated 30% faster program speed than conventional 1.8 V Octal devices. The product also eliminated the need for an external boost circuit in thin wearable platforms by pairing a 1.8 V core with 1.2 V I/O, which is important in space-limited devices. Single and dual SPI still matter in simpler IoT nodes and basic appliances, but the growth path in the NOR flash for consumer electronics market is moving toward interfaces that support more demanding firmware loads and richer device responsiveness. As the product mix shifts toward AI-enabled and display-heavy platforms, Octal and xSPI should take a larger share of new premium design wins.

Geography Analysis

Asia-Pacific accounted for 52.8% of NOR flash market share in the consumer electronics market in 2025 and is also the fastest-growing regional block, with a 7.2% CAGR through 2031. China remains the main anchor because it combines the largest consumer electronics assembly base with a growing domestic memory supply position in smartphones, TWS devices, smart speakers, and smart-home hardware. Taiwan adds major wafer capacity and design depth, and Winbond said its Taichung site is moving toward 57,000 to 58,000 monthly wafer starts by late 2026 to support flash demand. Japan supports the region through premium electronics design and low-power memory know-how, while Renesas has highlighted serial NOR solutions with sleep current as low as 0.2 µA in its memory portfolio materials. South Korea remains important in flagship smartphones and connected display products, where higher-throughput interfaces and denser firmware storage are more common.

North America and Europe formed the second-largest demand cluster in the NOR flash for consumer electronics market, driven by premium device demand, gaming ecosystems, smart-home hardware, and connected home security products. The United States remains the largest single-country market in this group because of strong smart-speaker penetration, console refresh cycles, and connected-home platform upgrades. Europe has a stronger regulatory impact on memory content because firmware integrity and secure update capabilities carry greater weight in connected device design and documentation. The EU Cyber Resilience Act is central to that shift because it brings a more formal security framework to products that rely on managed firmware behavior.

South America, the Middle East, and Africa remained smaller in absolute demand, but they continue to add volume in affordable smartphones, value-tier streaming products, and connected appliances. Brazil stands out in South America because domestic electronics incentives support local manufacturing and assembly, providing a stable demand base for mid-range serial NOR products. Saudi Arabia and the United Arab Emirates are strengthening connected-device use through smart-city and digital infrastructure programs that support secure consumer gateways and home systems. Across Africa, demand tracks smartphone adoption and import assembly patterns, which favor established suppliers offering reliable mid-density parts with long lifecycle support. These regions do not yet set the technology pace for NOR flash in the consumer electronics market, but they do expand the addressable customer base for standard-serial products at mainstream density and voltage points.

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Micron Technology Inc.

- Infineon Technologies AG

- Microchip Technology Inc.

- Integrated Silicon Solution Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Electronics Co. Ltd.

- Alliance Memory Inc.

- Zbit Semiconductor Inc.

- Xi'an Longsys Co. Ltd.

- Cypress Semiconductor Corp.

- AMIC Technology Corp.

- Fudan Microelectronics Group Co. Ltd.

- EON Silicon Solution Inc.

- Unigroup Guoxin Microelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation Of Voice-First Smart-Home Hubs Requiring Instant-On Firmware

- 4.2.2 Ultra-Low-Power Wearables Driving Sub-45 nm Demand

- 4.2.3 Secure-Boot And OTA-Update Mandates In Connected TVs And Gaming Consoles

- 4.2.4 China's 55/40 nm Localization Push Boosting Mid-Density NOR For Smartphones

- 4.2.5 Quad/Octal SPI Interfaces Enabling 4K Camera And Drone Fast-Boot Architectures

- 4.2.6 Edge-AI IoT Appliances Adopting XiP Architecture Favouring Hi-Density Serial NOR

- 4.3 Market Restraints

- 4.3.1 Cost Premium Vs NAND Above 256 Mb Limiting Hi-Resolution Camera Adoption

- 4.3.2 Scaling Ceilings Beyond 45 nm Steering OEMs Toward MRAM/ReRAM Alternatives

- 4.3.3 ASP Compression From Rising Chinese Capacity Pressuring Vendor Margins

- 4.3.4 Foundry Concentration In Taiwan Exposing Consumer-Device Supply Risk

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By NOR Flash Type (Value And Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal And xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65-3.6 V)

- 5.4.4 <=1.2 V Class

- 5.5 By Process Technology Node (Value)

- 5.5.1 90 nm and More

- 5.5.2 65 nm

- 5.5.3 55 nm (Incl. 58 nm)

- 5.5.4 45 nm

- 5.5.5 28 nm and Below

- 5.6 By Packaging Type (Value)

- 5.6.1 WLCSP / CSP

- 5.6.2 QFN / SOIC

- 5.6.3 BGA / FBGA

- 5.6.4 Other Packaging Types

- 5.7 By Geography (Value And Volume)

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest Of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Italy

- 5.7.3.5 Russia

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 Taiwan

- 5.7.4.5 India

- 5.7.4.6 Southeast Asia

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Turkey

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 United Arab Emirates

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Egypt

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products And Services, Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Micron Technology Inc.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Microchip Technology Inc.

- 6.4.7 Integrated Silicon Solution Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Wuhan XMC

- 6.4.11 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.12 Samsung Electronics Co. Ltd.

- 6.4.13 Alliance Memory Inc.

- 6.4.14 Zbit Semiconductor Inc.

- 6.4.15 Xi'an Longsys Co. Ltd.

- 6.4.16 Cypress Semiconductor Corp.

- 6.4.17 AMIC Technology Corp.

- 6.4.18 Fudan Microelectronics Group Co. Ltd.

- 6.4.19 EON Silicon Solution Inc.

- 6.4.20 Unigroup Guoxin Microelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis