PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061785

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061785

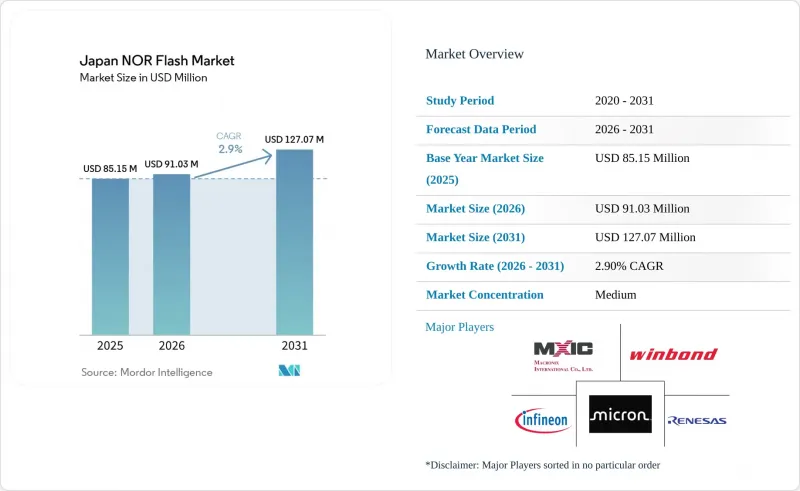

Japan NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan nOR flash market size is expected to increase from USD 91.03 million in 2026 to reach USD 127.07 million by 2031, growing at a CAGR of 2.90% over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3 V Class, 1. 8 V Class and More), End-User Application (Consumer Electronics, and More), Process Technology Node (90 Nm and Older, 55 Nm, and More), Packaging Type (WLCSP/CSP, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Japan NOR Flash Market Trends and Insights

Proliferation of Embedded NOR Flash in Automotive ECUs

Japanese vehicle makers are consolidating multiple control domains into zonal architectures that rely on high-density NOR Flash for sub-second boot times and firmware-over-the-air updates. Infineon's ASIL-D-certified SEMPER family, GigaDevice's GD25/55 line, and Macronix's 400 MB/s Octal part all received automotive safety nods, giving tier-1 suppliers certified building blocks. Growing electric-vehicle output and stricter ADAS mandates enlarge firmware images, so each car now embeds more NOR bits even as ECU counts decline. Subaru's 2026 platform using Infineon AURIX microcontrollers exemplifies this shift, reinforcing the Japan NOR Flash market's link to domestic auto production.

Demand for High-Reliability Memory in Industrial Automation

Society 5.0 is driving factories toward cyber-physical convergence, with METI allocating JPY 29.5 billion (USD 0.19 billion) for edge-AI semiconductors designed to boot instantly and withstand extreme factory conditions. These advancements are critical as controllers operating on private 5G networks require deterministic start-up capabilities. NOR flash memory, with its execute-in-place feature, eliminates the latency associated with NAND shadowing, making it a preferred choice. To meet these demands, suppliers are qualifying products with wider temperature ranges and enhanced error-correction codes. This alignment of product roadmaps with Japanese automation clusters is fostering innovation and supporting the country's push toward advanced manufacturing.

Capital-Intensive Migration to 28 nm and Below Nodes

Moving embedded NOR to advanced nodes reduces cost per bit but demands expensive tooling. SST and UMC's 28 nm SuperFlash proves technical feasibility, yet most domestic lines still run 40-55 nm because Japan's fab costs outpace Taiwan and China. Government funds target logic rather than mature NOR, so suppliers must either absorb lower margins or outsource, dampening the pace at which the Japan NOR Flash market accesses cost-efficient capacity.

Other drivers and restraints analyzed in the detailed report include:

- Transition From LCD to OLED and MicroLED Panels

- Expansion of 5G Base Stations and O-RAN Hardware

- Growing Adoption of SLC NAND as a Substitute

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, serial devices captured a commanding 77.81% share of Japan's NOR Flash market. Their dominance is attributed to their lower pin count and compact footprints, which make them highly suitable for space-constrained applications such as ECUs and IoT boards. These devices benefit from advancements like continued density scaling and the adoption of Octal/xSPI modes, enabling them to achieve throughput levels comparable to parallel NOR without increasing costs. This combination of performance and cost-efficiency has solidified their position as the preferred choice in the market. Furthermore, their ability to meet the evolving demands of modern applications ensures their sustained relevance. Consequently, serial devices are expected to maintain their leadership in Japan's NOR Flash market through 2031.

Meanwhile, parallel NOR continues to serve a loyal customer base in legacy industrial controllers and aerospace systems. These systems rely on microcontrollers specifically designed for 16- or 32-bit buses, making them incompatible with newer technologies without significant modifications. Transitioning these platforms would require extensive PCB redesigns and recertification processes, which are both time-consuming and costly. As a result, users often opt to retain these systems, ensuring the segment's continued presence in the market. Despite its niche status, parallel NOR is projected to achieve a respectable 3.26% growth rate, driven by its critical role in supporting legacy applications. This steady demand underscores its importance in specific industrial and aerospace use cases.

Quad SPI, accounting for 49.12% of revenue, strikes a balance between cost and speed for mainstream designs. Its widespread adoption is driven by its ability to meet the performance requirements of various applications without significantly increasing costs. On the other hand, the Octal/xSPI segment is emerging as the fastest-growing player in Japan's NOR Flash market, boasting a 4.62% CAGR. This growth is attributed to its superior bandwidth capabilities, which exceed 400 MB/s. Such high bandwidth enables multi-core ADAS processors to achieve sub-second ignition readiness, a critical requirement for 2026 vehicle programs. The increasing demand for advanced automotive systems further fuels the adoption of Octal/xSPI interfaces.

Single and Dual SPI cater to price-sensitive wearables and smart-home sensors, which boot infrequently and handle modest data transmissions. These interfaces are particularly suited for applications where cost efficiency is a priority over high performance. Their simplicity and low power consumption make them ideal for devices with limited functionality and intermittent usage. Despite advancements in other interfaces, Single and Dual SPI will continue to thrive in scenarios where controlling the bill of materials takes precedence. Their persistence in the market highlights the ongoing demand for cost-effective solutions in specific use cases. As a result, they remain a vital part of the NOR Flash market ecosystem.

In 2025, devices with 64 Mb memory and below accounted for 26.14% of sales, primarily in body electronics and traditional factory nodes. These devices continue to play a significant role in applications where cost efficiency and basic functionality are prioritized. However, advancements in technology have led to increased memory requirements in certain applications. ADAS domain controllers, OLED timing-controllers, and Open RAN radios now demand dual images for failsafe updates, effectively doubling their memory needs. This shift has driven the adoption of higher memory densities, particularly those exceeding 256 Mb. These higher densities are expanding at a rate of 5.93%, significantly contributing to the growth of Japan's NOR Flash market, especially in premium product segments.

While lower memory ranges, like 2 Mb, still cater to ultra-low-cost tags and basic sensors, their applications are gradually evolving. The proliferation of edge-AI technologies is driving a need for more advanced capabilities even in cost-sensitive designs. As a result, these designs are expected to transition to 4 Mb memory to accommodate inference libraries and support AI-driven functionalities. This shift highlights the growing demand for higher memory capacities across various applications. Although the transition may take time, the trend underscores the increasing importance of memory in enabling smarter and more efficient devices. The evolution of these lower ranges reflects the broader technological advancements shaping the NOR Flash market.

List of Companies Covered in this Report:

- Infineon Technologies AG

- Winbond Electronics Corporation

- Renesas Electronics Corporation

- Macronix International Co., Ltd.

- Micron Technology Inc.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan Xinxin Semiconductor Manufacturing Co. Ltd

- Puya Semiconductor (Shanghai) Co., Ltd.

- Fudan Microelectronics Group

- Cypress Semiconductor Corporation

- Rohm Co., Ltd.

- Dialog Semiconductor Plc

- Etron Technology Inc.

- Tower Semiconductor Ltd.

- SkyHigh Memory Limited

- Longsys Electronics Co., Ltd.

- Spansion LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Embedded NOR Flash in Automotive ECUs Driven by Japan's ADAS and EV Growth

- 4.2.2 Demand for High-Reliability Memory in Industrial Automation Amid Society 5.0 Initiatives

- 4.2.3 Transition from LCD to OLED and MicroLED Panels Requiring Higher-Density NOR for Timing Controllers

- 4.2.4 Expansion of 5G Base Stations and O-RAN Hardware Requiring Fast Boot-Code Storage

- 4.2.5 Localization of Semiconductor Supply Chain Under METI Resilience Programs

- 4.2.6 Emergence of AI Edge Devices Demanding Instant-On Code Storage in Harsh Environments

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive Migration to 28 nm and Below Nodes in Japan's High-Cost Fab Environment

- 4.3.2 Growing Adoption of SLC NAND as a Lower-Cost Substitute in Consumer Electronics

- 4.3.3 Limited Domestic Lithography Capacity Constraining High-Volume NOR Production

- 4.3.4 Yen Volatility Inflating Imported Photoresist and Equipment Costs

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Impact of Macroeconomic Factors on the Market

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By NOR Flash Type (Value)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 4 Megabit and Less (Greater than 2 Mb)

- 5.3.3 8 Megabit and Less (Greater than 4 Mb)

- 5.3.4 16 Megabit and Less (Greater than 8 Mb)

- 5.3.5 32 Megabit and Less (Greater than 16 Mb)

- 5.3.6 64 Megabit and Less (Greater than 32 Mb)

- 5.3.7 128 Megabit and Less (Greater than 64 Mb)

- 5.3.8 256 Megabit and Less (Greater than 128 Mb)

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Sub-1.8 V Class (1.2 V and Similar)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication Infrastructure

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Positioning Analysis

- 6.5 Company Profiles

- 6.5.1 Infineon Technologies AG

- 6.5.2 Winbond Electronics Corporation

- 6.5.3 Renesas Electronics Corporation

- 6.5.4 Macronix International Co., Ltd.

- 6.5.5 Micron Technology Inc.

- 6.5.6 GigaDevice Semiconductor Inc.

- 6.5.7 Integrated Silicon Solution Inc.

- 6.5.8 Microchip Technology Inc.

- 6.5.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.5.10 Wuhan Xinxin Semiconductor Manufacturing Co. Ltd

- 6.5.11 Puya Semiconductor (Shanghai) Co., Ltd.

- 6.5.12 Fudan Microelectronics Group

- 6.5.13 Cypress Semiconductor Corporation

- 6.5.14 Rohm Co., Ltd.

- 6.5.15 Dialog Semiconductor Plc

- 6.5.16 Etron Technology Inc.

- 6.5.17 Tower Semiconductor Ltd.

- 6.5.18 SkyHigh Memory Limited

- 6.5.19 Longsys Electronics Co., Ltd.

- 6.5.20 Spansion LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment