PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061846

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061846

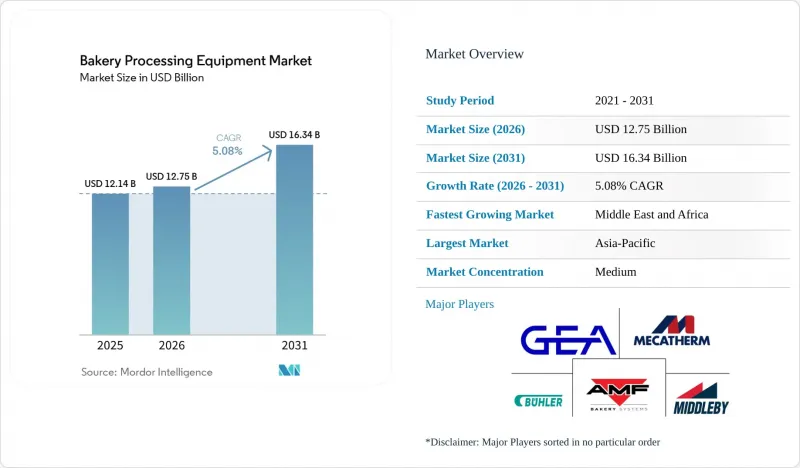

Bakery Processing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the bakery processing equipment market size is expected to increase from USD 12.14 billion in 2025 to USD 12.75 billion in 2026 and reach USD 16.34 billion by 2031, growing at a 5.08% CAGR over 2026-2031.

This report is Segmented by Equipment Type (Mixers and Blenders, Dividers and Rounders, Molders and Sheeters, Ovens and Proofers, Others), Application (Bread, Cakes and Pastries, Cookies and Biscuits, Pizza Crusts, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Bakery Processing Equipment Market Trends and Insights

Rising global demand for artisanal and specialty bakery products

Independent zone-control deck ovens and gentle-handling molders are now at the forefront of design briefs, allowing for high-hydration, long-fermentation doughs that maintain their gas-cell structure, which is critical for achieving desired texture and flavor profiles in artisanal baking. Moreover, as 6% of consumers shift their preferences towards bakery purchases, whether at home or in-store, the demand for adaptable and efficient processing equipment becomes increasingly evident. Suppliers in the ovens and proofers market are witnessing a surge in demand for flexible lines, capable of transitioning from ciabatta to focaccia without the need for tooling swaps, thereby enhancing operational efficiency and reducing downtime. An IBIE survey from 2025 highlighted that 64% of North American bakers are allocating budgets for specialty lines within the next 24 months, with a particular focus on spelt and einkorn capabilities, driven by consumer interest in ancient grains and their perceived health benefits. While this trend is muted in the cost-sensitive Asia-Pacific region, boutique chains in Shanghai and Mumbai are already aligning with Western demand patterns, albeit with a five-year delay, as they gradually cater to a growing niche of health-conscious and premium-seeking consumers.

Increased automation and hygienic-design standards

Protocols like FSMA, NSF/ANSI 169, and EHEDG mandate sanitary enclosures, tool-free disassembly, and CIP circuits to ensure compliance with stringent hygiene and safety standards in food processing and manufacturing. Vendors, including Middleby and VMI, tout mixers and ovens that slash cleaning time by 40% and digitally log sanitation cycles, lightening the audit load and improving operational efficiency. With embedded sensors and smart HMIs, operators enjoy a 60% reduction in labor costs and a return on investment within 12 to 18 months. This is especially appealing as wage inflation surpasses financing expenses, making automation a cost-effective solution. Meanwhile, smaller operators are turning to leasing structures with seasonal repayments to navigate the capital gap, enabling them to adopt advanced equipment without significant upfront investment.

High capital expenditure for advanced equipment lines

Turnkey bakeries now demand an investment of USD 2-5 million. This challenge is intensified by lead times stretching 9-12 months and financing costs that are 200-300 basis points higher than averages seen before 2024. These higher costs and extended timelines have created significant barriers for new players in the market. With tighter budgets, new entrants are leaning towards refurbished European machinery, snagging them at discounts of up to 70%. This approach allows them to reduce initial capital expenditure but often comes at the expense of operational efficiency. Additionally, the reliance on refurbished equipment limits the scalability of operations, making it harder for these players to compete with established market leaders. This choice has led to a postponement in fully adopting automation, a trend particularly evident in Latin America and Southeast Asia. The delayed automation adoption further impacts productivity and the ability to meet growing consumer demand in these regions.

Other drivers and restraints analyzed in the detailed report include:

- Energy-efficient equipment adoption amid sustainability mandates

- Expansion of industrial-scale bakeries in emerging asia-pacific markets

- Skilled-labor shortage and steep learning curve

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ovens and proofers are set to command a dominant 32.56% share of the thermal-processing equipment market's total revenue. Their supremacy is bolstered by a diverse product lineup, featuring deck, rack, tunnel, spiral, and hybrid fuel systems, each tailored for distinct throughput and formulation needs. These systems are indispensable in bakery production, underscoring the segment's robust demand. Furthermore, innovations like hybrid-fuel tunnels, heat-recovery modules, and rapid belt-change systems not only boost operational efficiency but also curtail costs, perpetuating a cycle of equipment upgrades. While Chinese OEMs exert pricing pressures, discerning premium buyers remain steadfast, emphasizing lifecycle costs, reliability, and after-sales service.

Molders and sheeters are on a rapid ascent, eyeing a 14% market share by 2031. This surge is fueled by the rising industrial-scale production of laminated delicacies like croissants and pastries. Anticipating a CAGR of 5.08% until 2031, the segment's growth is a testament to its adoption in high-volume bakery operations. The push for automation and uniformity in dough handling, especially in large-scale and export-focused facilities, drives this expansion. Moreover, advancements in precision forming and seamless integration with continuous production lines are hastening the adoption. As bakery producers broaden their laminated offerings, the momentum for investing in cutting-edge molding and sheeting equipment is poised to escalate.

Geography Analysis

In 2025, the Asia-Pacific region is projected to hold a leading 39.53% revenue share, driven by the development of greenfield capacities in China, India, and various ASEAN nations. Domestic OEMs offer price advantages that enable local bakers to achieve faster returns on investment, although premium imports remain preferred in scenarios where recipe precision and uptime are critical. The rise in urbanization and increasing demand for packaged bakery products are driving equipment investments in tier-2 and tier-3 cities. Additionally, government incentives supporting food processing infrastructure are accelerating the adoption of advanced baking technologies. Regional players are also increasingly adopting automation to enhance consistency and reduce reliance on skilled labor.

The Middle East and Africa are expected to record a strong 7.02% CAGR. In Saudi Arabia, sovereign wealth investments are focused on localizing staple bread production, while Egyptian producers are increasing output fivefold to meet the needs of North African supermarkets. Expanding retail chains and modern trade formats are boosting demand for standardized, high-volume baking solutions. Investments in food security programs across Gulf nations are further strengthening local production capabilities. Partnerships with European equipment suppliers are also enabling regional manufacturers to upgrade their technological capabilities. Population growth and evolving urban consumption patterns continue to support long-term market growth.

Europe and North America, which together account for a significant market share, are shifting their focus from capacity expansion to replacement spending. This shift is primarily driven by stringent hygiene and energy regulations. Manufacturers are prioritizing equipment upgrades to meet strict emissions and food safety standards. The adoption of digitalization, including IoT-enabled monitoring systems, is becoming a key factor in equipment procurement decisions. Retrofitting existing production lines with energy-efficient components is helping bakeries manage operational costs. Furthermore, labor shortages are accelerating the adoption of automation and remote diagnostics.

- GEA Group Aktiengesellschaft

- Buhler Holding AG

- John Bean Technologies Corporation

- The Middleby Corporation (Baker Perkins)

- Ali Group S.r.l. (Rondo)

- AMF Bakery Systems (a Markel Food Group Company)

- Mecatherm S.A.

- Rademaker B.V.

- WP Bakery Group GmbH

- Koenig Maschinen GmbH

- European Pastry & Bakery Machinery (EBAK)

- Reading Bakery Systems (a Markel Food Group Company)

- Revent International AB

- Shaffer Mixing

- Zeppelin Systems GmbH

- Oshikiri Machinery Ltd.

- VMI SA (VMI Group)

- Sigma S.r.l.

- Rheon Automatic Machinery Co., Ltd.

- Gemini Bakery Equipment Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global demand for artisanal and specialty bakery products

- 4.2.2 Increased automation and hygienic-design standards

- 4.2.3 Energy-efficient equipment adoption amid sustainability mandates

- 4.2.4 Expansion of industrial-scale bakeries in emerging Asia-Pacific markets

- 4.2.5 IoT-enabled predictive maintenance reducing unplanned downtime

- 4.2.6 Specialized equipment for gluten-free and alt-grain formulations

- 4.3 Market Restraints

- 4.3.1 High capital expenditure for advanced equipment lines

- 4.3.2 Skilled-labor shortage and steep learning curve

- 4.3.3 Electronic-component supply-chain fragility

- 4.3.4 Prospective carbon-border taxes inflating lifecycle costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Mixers and Blenders

- 5.1.2 Dividers and Rounder

- 5.1.3 Molders and Sheeters

- 5.1.4 Ovens and Proofers

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Bread

- 5.2.2 Cakes and Pastries

- 5.2.3 Cookies and Biscuits

- 5.2.4 Pizza Crusts

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Netherlands

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 GEA Group Aktiengesellschaft

- 6.4.2 Buhler Holding AG

- 6.4.3 John Bean Technologies Corporation

- 6.4.4 The Middleby Corporation (Baker Perkins)

- 6.4.5 Ali Group S.r.l. (Rondo)

- 6.4.6 AMF Bakery Systems (a Markel Food Group Company)

- 6.4.7 Mecatherm S.A.

- 6.4.8 Rademaker B.V.

- 6.4.9 WP Bakery Group GmbH

- 6.4.10 Koenig Maschinen GmbH

- 6.4.11 European Pastry & Bakery Machinery (EBAK)

- 6.4.12 Reading Bakery Systems (a Markel Food Group Company)

- 6.4.13 Revent International AB

- 6.4.14 Shaffer Mixing

- 6.4.15 Zeppelin Systems GmbH

- 6.4.16 Oshikiri Machinery Ltd.

- 6.4.17 VMI SA (VMI Group)

- 6.4.18 Sigma S.r.l.

- 6.4.19 Rheon Automatic Machinery Co., Ltd.

- 6.4.20 Gemini Bakery Equipment Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK