PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062234

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062234

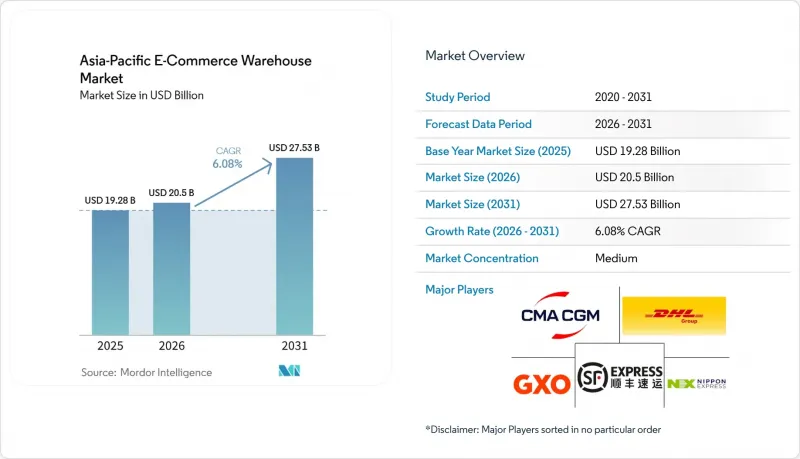

Asia-Pacific E-Commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific e-commerce warehousing market size is expected to grow from USD 19.28 billion in 2025 to USD 20.50 billion in 2026, and is forecast to reach USD 27.53 billion by 2031, growing at a 6.08% CAGR over 2026-2031.

Continued migration from self-run logistics to outsourced 3PL campuses is the principal structural shift, with specialized providers capturing 65% of new leasing in the Asia-Pacific e-commerce warehousing market during 2025. This report is Segmented by Warehouse Type (Fulfilment Centers, Distribution Centers, Cold-Chain, Dark Stores/Micro-Fulfillment, Others), by Service Type (Storage, Picking and Packing, and More), by Automation Level (Manual, Semi-Automated, Automated), by End-User Industry (Apparel, Electronics, Grocery, Pharma, Home Essentials, Others), and by Country. The Market Forecasts in Value (USD).

Asia-Pacific E-Commerce Warehouse Market Trends and Insights

D2C Brand Wave Outsourcing Fulfillment to 3PL Campuses

Direct-to-consumer labels are abandoning owned warehouses in favor of variable-cost 3PL campuses, lifting the Asia-Pacific e-commerce warehousing market as multi-client hubs proliferate. Third-party providers signed two-thirds of all new logistics space in 2025 because shared robotics and labor pools drop per-order costs 25-30% for mid-size brands. The 3PL portion of regional logistics revenue grew at 18% CAGR in 2025, and operators such as GXO and CEVA now run campuses that host 8-15 brands under one roof to maximize automation utilization. DHL added 12 similar sites across Southeast Asia in 2025, each engineered for SKU segregation and data-rich SLAs. Increased density raises complexity, so campuses rely on advanced warehouse management systems that segregate inventory and certify data security compliance.

Government Automation-Subsidy Programs Accelerating Robot Uptake

Fiscal incentives are shortening robot ROI cycles across the Asia-Pacific e-commerce warehousing market. Singapore reimburses up to 50% of automation capex, disbursing SGD 180 million (USD 133 million) in 2025. Japan and South Korea unveiled similar grants totaling USD 1 billion that cut payback to 2-3 years for goods-to-person systems. India's 2025 policy offers a 25% subsidy for Grade A sites, though complex paperwork slowed utilization to one-third of allocated funds. Subsidies pulled 2026-2027 installations forward, pushing regional AMR deployments to 47,000 units in 2025, 62% higher than 2024.

Data-Localization and Cybersecurity Mandates Inflating WMS Costs

Country-level data-sovereignty laws obligate in-country hosting, raising architecture costs 25-40% for multi-market 3PLs and undercutting the cloud-efficiency thesis of the Asia-Pacific e-commerce warehousing market. China's Data Security Law, India's Digital Personal Data Protection Act, and Indonesia's GR 71/2019 force separate instances of warehouse software, driving hybrid models with local data stores and regional analytics. Operators report 30-45% higher maintenance outlays relative to unified platforms, a burden absorbed more easily by large 3PLs than by mid-size incumbents.

Other drivers and restraints analyzed in the detailed report include:

- Regional Free-Trade Zones Streamlining Cross-Border E-Commerce Flows

- ASEAN Customs Transit System Enabling Bonded Trans-Shipment Hubs

- Stricter Lithium-Battery Fire-Safety Codes Raising Build-Out Capex

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfillment centers led with 51.25% of the Asia-Pacific e-commerce warehousing market share in 2025, yet dark stores and micro-fulfillment nodes are growing 11.74% CAGR as retailers chase sub-two-hour city deliveries. GXO's multi-tenant campus model yields 25-30% cost savings thanks to shared robots and cross-docking, signaling continued momentum away from single-brand sheds. Cold-chain capacity is rising fastest inside this segment, propelled by meal-kit operators and temperature-sensitive pharma. Bonded warehouses classified in "others" are enlarging to manage cross-border returns and duty-deferral advantages, processing 2.4 billion parcels in China alone.

Distribution centers still anchor bulk import staging, yet brands juggling multiple facility archetypes struggle with visibility; 42% cite inventory blind spots across formats, nudging demand for unified control-tower software. The Asia-Pacific e-commerce warehousing industry, therefore, shows both consolidation at campus scale and fragmentation at last-mile micro-node scale.

Storage controlled 47.47% of the Asia-Pacific e-commerce warehousing market size in 2025, but picking and packing is expanding at 11.21% CAGR through 2031 as brands seek turnkey partners. Automated goods-to-person systems now deliver 99.7% accuracy, superior to 97.5% for manual workflows, strengthening the outsourcing case. DSV captured 34% of new e-commerce contracts in 2025 with single-invoice packages that span storage, fulfillment, and last-mile.

Value-added kitting, labeling, and plastic-free packaging drive higher labor complexity and 15-20% higher operating costs but also command pricing premiums. Sustainability-aligned services such as carbon-neutral shipping have moved from niche to mainstream, requested by 67% of brands in 2025. Competitive edge now lies in software that orchestrates multi-tier services without eroding margin, a priority echoed by Kerry Logistics' Fulfillment Plus program that grew revenue 28% last year.

List of Companies Covered in this Report:

- DHL Group

- DSV A/S

- CMA CGM Group (Including CEVA Logistics)

- NYK Line (Including Yusen Logistics)

- Nippon Express Holdings

- SF Express (KEX-SF)

- JD Logistics Holdings

- Cainiao Network

- CJ Logistics

- Lineage, Inc.

- Linfox Pty Ltd.

- J&T Express

- Flash Express

- Locad

- Kuehne+Nagel

- GEODIS

- GXO Logistics

- Allcargo Logistics

- Kintetsu Worldwide Express

- Aramex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 D2C Brand Wave Outsourcing Fulfilment to 3PL Campuses

- 4.2.2 Government Automation-Subsidy Programs Accelerating Robot Uptake

- 4.2.3 Regional Free-Trade Zones Streamlining Cross-Border E-Commerce Flows

- 4.2.4 ASEAN Customs Transit System Enabling Bonded Trans-Shipment Hubs

- 4.2.5 Rooftop Solar + Battery Retrofits Cutting Warehouse Opex

- 4.2.6 Meal-Kit and Fresh-Subscription Boom Driving Multi-Temperature Facilities

- 4.3 Market Restraints

- 4.3.1 Data-Localization and Cybersecurity Mandates Inflating WMS Costs

- 4.3.2 Stricter Lithium-Battery Fire-Safety Codes Raising Build-Out Capex

- 4.3.3 Urban Night-Time Truck-Movement Curfews Compress Docking Windows

- 4.3.4 Flood-Risk Insurance Premiums Spiking for Coastal Mega-Sheds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centers

- 5.1.2 Distribution Centers (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking and Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Indonesia

- 5.5.6 Thailand

- 5.5.7 Vietnam

- 5.5.8 Australia

- 5.5.9 Singapore

- 5.5.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 DSV A/S

- 6.4.3 CMA CGM Group (Including CEVA Logistics)

- 6.4.4 NYK Line (Including Yusen Logistics)

- 6.4.5 Nippon Express Holdings

- 6.4.6 SF Express (KEX-SF)

- 6.4.7 JD Logistics Holdings

- 6.4.8 Cainiao Network

- 6.4.9 CJ Logistics

- 6.4.10 Lineage, Inc.

- 6.4.11 Linfox Pty Ltd.

- 6.4.12 J&T Express

- 6.4.13 Flash Express

- 6.4.14 Locad

- 6.4.15 Kuehne+Nagel

- 6.4.16 GEODIS

- 6.4.17 GXO Logistics

- 6.4.18 Allcargo Logistics

- 6.4.19 Kintetsu Worldwide Express

- 6.4.20 Aramex

7 Market Opportunities and Future Outlook