PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063338

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063338

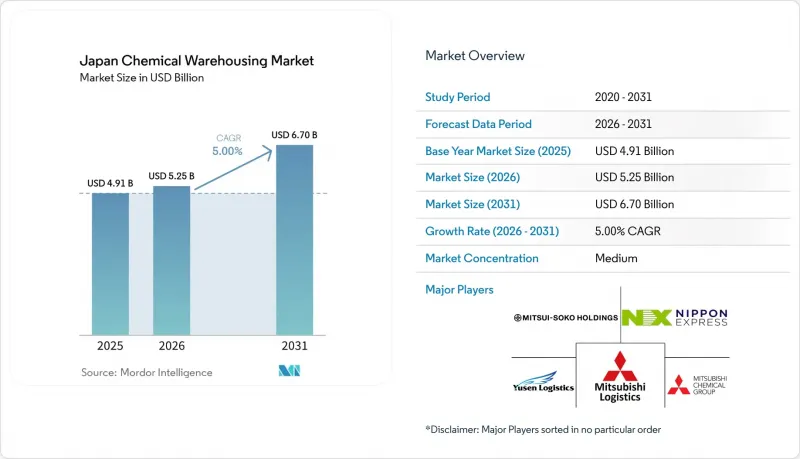

Japan Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan chemical warehousing market size is projected to expand from USD 4.91 billion in 2025 and USD 5.25 billion in 2026 to USD 6.70 billion by 2031, registering a CAGR of 5% between 2026 to 2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, Oxidizers, and More), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Agrochemicals, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

Japan Chemical Warehousing Market Trends and Insights

Advanced Materials Manufacturing Leadership

Japan's tilt toward high-value specialty chemicals and pharma intermediates is changing warehouse design and procedures, with validated environments and robust traceability becoming the constraint rather than bulk capacity. Nippon Shokubai plans to expand nucleic acid API capacity tenfold at its Suita site by 2027, which requires GMP-grade storage close to production and rigorous handling rules that extend into the warehouse. FUJIFILM Wako tripled its output capacity for GMP-compliant raw materials in 2024, strengthening local needs for temperature control, process segregation, and electronic documentation of environmental conditions. Towa Pharmaceutical targets 17.5 billion tablets annually by fiscal 2026, which will increase demand for cleanroom-adjacent warehousing and accurate lot-level custody logs to protect quality and meet release schedules. As production shifts to medium- and high-potency products, storage value density rises, increasing the financial stakes of temperature deviations and handling errors and pushing digital tracking into everyday warehousing practices.

Pharmaceutical and Life Sciences Expansion

An aging population and steady progress in biologics and nucleic acid therapies keep pharma warehousing demand resilient, requiring climate assurance, validated processes, and redundant systems to cut spoilage risk. Nippon Shokubai's program to install a large GMP production line for nucleic acid APIs by 2027 shows how manufacturing scales translate into heightened needs for compliant storage, data integrity, and clean logistics interfaces. Dedicated HAZMAT zones and enhanced ventilation are also relevant, as facilities handle higher-potency compounds alongside solvents and reagents common to pharma manufacturing. Warehouse operating models evolve to include validated temperature monitoring, real-time alerts, and audit-ready electronic records to satisfy documentation and release processes. Regional clusters in Osaka and Ibaraki are adding capacity near plants, supporting just-in-time flows for clinical and commercial timelines without compromising compliance.

Severe Land Scarcity and High Costs

Scarcity of suitable plots near petrochemical clusters and deep-water terminals constrains new warehouse construction and prompts developers to consider inland locations that trade proximity for lower costs. City planning and building rules in industrial belts keep pressure on design choices and timelines, especially for single-story fire-resistant HAZMAT facilities that require impermeable floors and spill containment. Operators respond with vertical storage systems and higher automation density to increase throughput within constrained footprints, improving economics but increasing capital requirements and complexity for future tenant changes. Circular-economy hubs are emerging at industrial ports that host chemical-recycling assets, thereby increasing the value of nearby bonded warehousing and pre-sorting capacity for inbound feedstock. These dynamics lift the strategic value of intermodal nodes and brownfield upgrades that can be brought up to code with validated fire protection and segregation.

Other drivers and restraints analyzed in the detailed report include:

- Logistics Automation and Robotics Adoption

- Regulatory Push for Safety Infrastructure

- Aging Workforce and Labor Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses held 41.24% of the Japan chemical warehousing market share in 2025, underscoring the country's shift toward high-value formulations and strict safety protocols. Specialty chemical storage near production lines supports fast cycle times and strict segregation between lots and product families, both of which are essential for GMP-compliant inputs and advanced materials. General warehousing still supports bulk polymers and commodity inputs, though operators are adding WMS and sensors to align with lean replenishment cycles for automotive and construction customers.HAZMAT sites follow Fire Service Act thresholds for designated quantities and adopt impermeable floors, foam suppression, and lightning protection, as relevant, which push construction costs beyond general warehouse norms. This mix increases switching costs for customers that require validated storage, a documented chain of custody, and audit-ready records covering the warehouse segment of the flow.

In the Japan chemical warehousing market, temperature-controlled chemical warehouses are leading the charge, boasting a robust 5.78% CAGR projected through 2031. These facilities, alongside HAZMAT-certified counterparts, stand out for their unique capabilities. Notably, they emphasize fire-resistant construction, climate redundancy, and meticulous traceability. The operational stack now spans backup generation with automatic failover, continuous temperature and humidity monitoring, alerting protocols, and electronic records that meet audit needs. Multi-tenant campuses add automated fire shutters and segregated bays because mixed stored goods bring overlapping hazard classifications that must be isolated. The Japan chemical warehousing industry is also lifting robotics adoption at docks and high-density aisles, which offsets margin pressure from rising wages and helps recover capacity lost to the 2024 driver overtime rules. Together, these investments are reshaping competitive positioning across warehouse types because validated capabilities command premium rates that support reinvestment and compliance upkeep.

List of Companies Covered in this Report:

- Mitsubishi Logistics Corporation

- Mitsui-Soko Holdings Co., Ltd.

- Nippon Express Holdings

- Yusen Logistics Co., Ltd. (NYK Line)

- Mitsubishi Chemical Logistics Corp. (Subsidiary of Mitsubishi Chemical Corporation)

- LOGISTEED, Ltd

- SENKO Group Holdings Co., Ltd.

- Sanwa Soko Co., Ltd.

- Tatsumi Co., Ltd.

- Sankyu Logistics

- DHL Group

- Chikko Corporation

- Kuehne + Nagel

- Rhenus Logistics

- CEVA Logistics

- DSV

- Yasuda Logistics

- Tosoh Logistics Corporation

- AIT Worldwide Logistics, Inc.

- Odyssey Logistics and Technology (Japan)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced Materials Manufacturing Leadership

- 4.2.2 Pharmaceutical and Life Sciences Expansion

- 4.2.3 Logistics Automation and Robotics Adoption

- 4.2.4 Fine Chemicals and Intermediates Growth

- 4.2.5 Regulatory Push for Safety Infrastructure

- 4.2.6 Chemical Industry Consolidation

- 4.3 Market Restraints

- 4.3.1 Severe Land Scarcity and High Costs

- 4.3.2 Aging Workforce and Labor Shortage

- 4.3.3 Stringent Regulatory Compliance Burden

- 4.3.4 High Energy and Operating Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitical Events on the Market

- 4.9 Circular Economy Chemical Recycling

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Mitsubishi Logistics Corporation

- 6.4.2 Mitsui-Soko Holdings Co., Ltd.

- 6.4.3 Nippon Express Holdings

- 6.4.4 Yusen Logistics Co., Ltd. (NYK Line)

- 6.4.5 Mitsubishi Chemical Logistics Corp. (Subsidiary of Mitsubishi Chemical Corporation)

- 6.4.6 LOGISTEED, Ltd

- 6.4.7 SENKO Group Holdings Co., Ltd.

- 6.4.8 Sanwa Soko Co., Ltd.

- 6.4.9 Tatsumi Co., Ltd.

- 6.4.10 Sankyu Logistics

- 6.4.11 DHL Group

- 6.4.12 Chikko Corporation

- 6.4.13 Kuehne + Nagel

- 6.4.14 Rhenus Logistics

- 6.4.15 CEVA Logistics

- 6.4.16 DSV

- 6.4.17 Yasuda Logistics

- 6.4.18 Tosoh Logistics Corporation

- 6.4.19 AIT Worldwide Logistics, Inc.

- 6.4.20 Odyssey Logistics and Technology (Japan)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment