PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063322

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063322

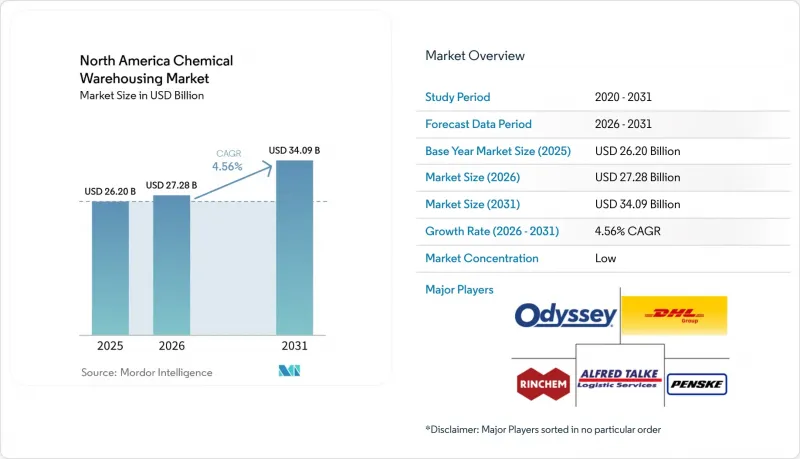

North America Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america chemical warehousing market size is projected to expand from USD 26.2 billion in 2025 and USD 27.28 billion in 2026 to USD 34.09 billion by 2031, registering a 4.56% CAGR between 2026 and 2031.

Rising demand for sustainability-certified storage, growth in battery-grade lithium compounds, and ongoing nearshoring into Northern Mexico are reshaping service requirements and facility locations across the North America chemical warehousing market. This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, HAZMAT Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Country (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Chemical Warehousing Market Trends and Insights

Surge in Carbon-Neutral Pledges Driving Demand for LEED and ISO 14001-Certified Chemical Warehouses

Corporate sustainability targets now include Scope 3 logistics emissions, prompting shippers to insist that third-party facilities meet LEED and ISO 14001 benchmarks. Operators adopting solar roofs, high-efficiency HVAC and on-site water recycling qualify for green loans and command premium rent in the North America chemical warehousing market. Energy costs averaging 6.6 cents /kWh along the Gulf Coast further improve payback periods for renewable retrofits. These certifications create tangible barriers to entry that channel volume toward well-capitalized incumbents. As state regulators align building codes with climate policy, sustainability credentials are expected to become a baseline requirement rather than a differentiator across the North America chemical warehousing market.

Rapid Expansion of Battery-Grade and Energy-Storage Chemicals Requiring Segregated Temperature-Controlled Storage

Electrolyte solvents and lithium hydroxide are hypersensitive to moisture and trace metals, forcing warehouses to add dew-point monitoring, inert gas blanketing, and isolated rooms. Rinchem's 123,000 ft2 Arizona site illustrates the upgraded ventilation and sensor arrays now standard for this trade. Precision helps reduce batch-failure risk, enabling multi-year contracts that lock in utilization. With automotive OEMs announcing 15 new battery plants by 2027, demand for such dedicated capacity is set to rise more quickly than overall activity in the North America chemical warehousing market.

Cyclical Downturn Risk in Key End-Markets Causing Volatile Warehouse Utilization

Paints, plastics and construction additives cycle with housing starts and auto output, shrinking inventories during recessions. New Jersey's warehouse vacancy climbed to 9% in 2024 after 40 million ft2 of speculative builds came online without committed tenants. Similar swings in the North America chemical warehousing market squeeze margin on fixed-cost assets, compelling operators to court counter-cyclical sectors such as pharmaceuticals to balance portfolio risk.

Other drivers and restraints analyzed in the detailed report include:

- United States-Canada Inland-Port Build-Outs Integrating Rail, Barge and Pipeline Links with Dedicated Hazmat Terminals

- AI-Powered Safety Analytics Lowering Incident Rates and Insurance Prerequisites

- Emerging PFAS Bans Adding Uncertainty to Long-Tail Inventories and Liability Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The North America chemical warehousing market is witnessing notable growth, with Temperature-Controlled Chemical Warehouses projected to expand at a CAGR of 5.59% through 2031, surpassing the market's overall growth rate. This highlights the increasing demand for specialized storage solutions. Specialty Chemical Warehouses, holding a 34.25% market share in 2025, reflect the industry's emphasis on quality and compliance. Customers are demonstrating a willingness to invest in certifications, documentation, and validated monitoring systems to ensure safety and regulatory adherence. These factors collectively drive the evolution of the chemical warehousing market in the region.

Demand for dew-point control, inert gas purging, and backup power makes capital intensity high, yet also locks in multi-year contracts from electronics and life-science firms. Hansen Storage doubled freezer capacity to 600,000 ft2 to meet stricter climate-sensitivity standards. General Warehousing faces commoditization as shippers shift premium products into purpose-built zones across the North America chemical warehousing market, forcing non-specialists to compete on price or exit.

List of Companies Covered in this Report:

- DHL Group

- Rinchem Company, Inc.

- Odyssey Logistics and Technology

- ALFRED TALKE

- Penske Logistics

- Quantix Quantix Supply Chain Solutions (Formerly AandR Logistics)

- Porter Logistics

- Weber Logistics

- North American Warehousing Co.

- Metrix Logistics Group

- Buske Logistics

- Evans Distribution Systems

- FW Warehousing

- Rhenus Logistics

- ADLI Logistics

- GXO Logistics

- XPO, Inc.

- C.H. Robinson

- DSV A/S

- Kuehne+Nagel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Carbon-Neutral Pledges Driving Demand for LEED- and ISO 14001-Certified Chemical Warehouses

- 4.2.2 Rapid Expansion of Battery-Grade and Energy-Storage Chemicals Requiring Segregated Temperature-Controlled Storage

- 4.2.3 US-Canada Inland-Port Build-Outs Integrating Rail, Barge and Pipeline Links with Dedicated Hazmat Terminals

- 4.2.4 AI-Powered Safety Analytics Lowering Incident Rates and Insurance Prerequisites, Accelerating Facility Approvals

- 4.2.5 Growth of Bio-Based and Fermentation-Derived Chemicals Creating Allergen-Free, Contamination-Controlled Warehousing Niches

- 4.2.6 Post-CUSMA Near-Shoring Boom Shifting Specialty-Chemical Inventory South to Northern Mexico Logistics Corridors

- 4.3 Market Restraints

- 4.3.1 Cyclical Downturn Risk in Key End-Markets (Construction, Plastics) Causing Volatile Warehouse Utilization

- 4.3.2 Emerging PFAs Bans Adding Uncertainty to Long-Tail Chemical Inventories and Liability Management

- 4.3.3 Scarcity of Rail-Connected Hazmat-Zoned Land Parcels within Tier-1 Chemical Clusters

- 4.3.4 Rising Cyber-Security Threats to IoT-Integrated Hazmat Facilities Increasing Compliance and Mitigation Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Rinchem Company, Inc.

- 6.4.3 Odyssey Logistics and Technology

- 6.4.4 ALFRED TALKE

- 6.4.5 Penske Logistics

- 6.4.6 Quantix Quantix Supply Chain Solutions (Formerly AandR Logistics)

- 6.4.7 Porter Logistics

- 6.4.8 Weber Logistics

- 6.4.9 North American Warehousing Co.

- 6.4.10 Metrix Logistics Group

- 6.4.11 Buske Logistics

- 6.4.12 Evans Distribution Systems

- 6.4.13 FW Warehousing

- 6.4.14 Rhenus Logistics

- 6.4.15 ADLI Logistics

- 6.4.16 GXO Logistics

- 6.4.17 XPO, Inc.

- 6.4.18 C.H. Robinson

- 6.4.19 DSV A/S

- 6.4.20 Kuehne+Nagel

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment