PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062309

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062309

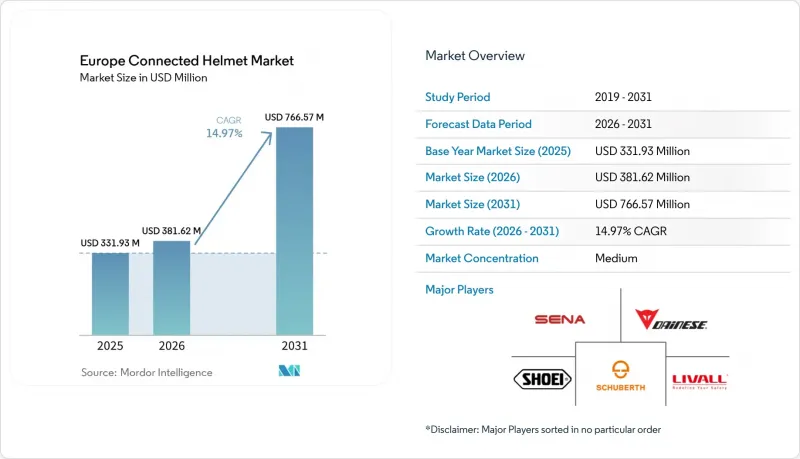

Europe Connected Helmet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe-connected helmet market size is projected to grow from USD 331.93 million in 2025 to USD 381.62 million in 2026, and is forecast to reach USD 766.57 million by 2031, growing at a CAGR of 14.97% from 2026 to 2031.

This report is Segmented by Product Type (Full Face, Modular/Flip-up, and More), Technology Level (Bluetooth-Only, Integrated Audio/Comms, and More), End User (Individual Rider, Passenger, and Fleet/Delivery), Distribution Channel (Offline Retail and Online Direct-To-Consumer), Price Range (Economy, Mid-Range, and Premium), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Connected Helmet Market Trends and Insights

Rising Adoption of Motorcycle ADAS and Hud-Enabled Helmets

Head-up display technology is evolving from a motorsport novelty to a touring essential. Shoei's GT-Air Smart, developed in collaboration with EyeLights and Sony, enhances rider reaction times by projecting navigation cues directly into their line of sight . Schuberth's C5 ANC features active noise cancellation, helping to reduce fatigue on extended Alpine journeys. Meanwhile, TVS's prototype showcased at EICMA offers spatially anchored AR guidance, but its limited battery life highlights energy density as a looming engineering challenge. German riders, accustomed to high-mileage treks across the Alps, appreciate these fatigue-reducing features and are ready to invest in premium HUD units. As HUD modules find their way into mid-priced helmets, the European connected helmet market is poised for broader price-tier penetration, all while maintaining UA certification standards.

EU Regulation 2025/555 Mandating E-Call Integration

The updated eCall regulations will transition emergency signaling to packet-switched networks. While eCall remains optional for motorcycles, helmet manufacturers are proactively adapting to meet the demands of insurers and fleet purchasers. BMW Motorrad has introduced a vehicle-mounted eCall system that significantly reduces response times, yet it does not incorporate a helmet. Quin Design and LIVALL, by integrating crash sensors into the helmet shell, maintain oversight of rider data and ensure their continued relevance in the aftermarket. Thus, the European connected helmet market hinges on determining which platform-be it a vehicle, a helmet, or a wearable-will first gain consumers' trust and insurers' endorsement.

High Upfront Cost Versus Conventional Helmets

Connected helmet models are roughly quadruple that of a plain polycarbonate lid, creating sticker shock in markets where average annual motorcycle spend is under a minimal budget. Southern European cities, where low-capacity scooters dominate, display the steepest price elasticity, stalling volume adoption. Providers attempt to soften the blow via buy-now-pay-later plans, yet interest costs partially offset savings from potential insurance rebates, muting conversion. Until electronics costs align with large-scale automotive supply chains, premium segmentation will continue to polarize the connected helmet market.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Premium Touring Culture Across Central and Northern Europe

- Insurance-Premium Discounts For Verified Connected-Helmet Use

- GDPR-Driven Data-Privacy Hurdles for Crash Telemetry

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-face models secured 43.41% of the Europe-connected helmet market size in 2025, by balancing aerodynamics, quiet interiors, and ECE 22.06 compliance. The Europe-connected helmet market for smart HUD units is set to outgrow every other category at a 15.15% CAGR to 2031, as nano-OLED modules reach sunlight-readable 3,000 nits and sub-50-gram optics. Shoei's GT-Air 3 Smart exemplifies the trend, combining Full HD projection with long-lasting batteries to cater to all-day tourers. While open-face and half helmets remain favored for Mediterranean scooter rides, they now face rising certification costs, narrowing the price gap with entry-level full-face models.

Touring riders who appreciate modular helmets for their ability to lift the chin bar during refueling are now benefiting from Cardo's integration of Mesh technology. This enhancement enables private group communication between multiple riders over long distances, effectively addressing communication challenges in Alpine tunnels. Meanwhile, off-road niches are thriving, as Quin-equipped O'Neal dirt helmets transmit crash data to emergency applications across European nations. Consequently, the European helmet market is divided between premium HUD models and Bluetooth-only full-face variants. Manufacturers adept at bridging both price points are strategically positioned to safeguard both volume and profit margins.

Integrated audio/comms accounted for 37.23% of the Europe-connected helmet market in 2025, as Bluetooth is now table stakes. Cardo and Sena's latest chipsets deliver 1.6 km of range and automatically switch between Mesh and Bluetooth modes, ensuring backward compatibility while future-proofing firmware updates. Yet ADAS-sensor helmets-gyros, accelerometers, eCall, and V2X-are scaling at 15.03% CAGR to 2031 as insurers demand real-time risk scoring. BMW's Com P1 GS seamlessly integrates crash detection into a module, which conveniently attaches to the GS Carbon shell.

While HUD/AR helmets come with a hefty price tag, they still face challenges with energy density. For instance, TVS's prototype reveals that the battery provides only a limited runtime in continuous AR mode. Designers of all-in-one helmets aspire to achieve the trifecta: UA-certified crash detection, HUD, and V2X functionalities within a single shell. However, as of now, only Midland's BT Mini and BTR1 Advanced have successfully passed UA's rotational tests. As the European market for connected helmets evolves, there's a growing trend towards a modular approach-combining helmets with certified clip-ons-potentially overshadowing the all-in-one super-helmets. This shift may persist until advancements in battery chemistry and a reduction in certification costs align.

List of Companies Covered in this Report:

- Dainese SpA

- Sena Technologies, Inc.

- Schuberth GmbH

- Shoei Co., Ltd.

- HJC Helmets

- LS2 Helmets

- Shark Helmets

- LIVALL Tech Co., Ltd.

- Jarvish Inc.

- CrossHelmet (Borderless Inc.)

- Forcite Helmet Systems

- Quin Design

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption Of Motorcycle Adas & Hud-Enabled Helmets

- 4.2.2 EU Regulation 2025/555 Mandating E-Call Integration

- 4.2.3 Growth In Premium Touring Culture Across Central & Northern Europe

- 4.2.4 Insurance-Premium Discounts For Verified Connected-Helmet Use

- 4.2.5 5G-V2X Corridor Build-Out Along Ten-T Routes

- 4.2.6 OEM Bundling Of Subscription-Based Rider-Data Services

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost Versus Conventional Helmets

- 4.3.2 Limited Battery Life & Cold-Weather Performance

- 4.3.3 GDPR-Driven Data-Privacy Hurdles For Crash Telemetry

- 4.3.4 Fragmented Certification Add-Ons Beyond ECE 22.06

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Full Face

- 5.1.2 Modular / Flip-up

- 5.1.3 Open Face

- 5.1.4 Half Helmet

- 5.1.5 Off-road / Motocross

- 5.1.6 Smart HUD-Integrated

- 5.2 By Technology Level

- 5.2.1 Bluetooth-Only

- 5.2.2 Integrated Audio / Comms

- 5.2.3 HUD / AR Display

- 5.2.4 Crash Detection & eCall

- 5.2.5 ADAS Sensor Suite

- 5.2.6 Multi-Feature (All-in-One)

- 5.3 By End User

- 5.3.1 Individual Rider

- 5.3.2 Passenger

- 5.3.3 Fleet / Delivery

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail

- 5.4.2 Online Direct-to-Consumer

- 5.5 By Price Range

- 5.5.1 Economy

- 5.5.2 Mid-Range

- 5.5.3 Premium

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Dainese SpA

- 6.4.2 Sena Technologies, Inc.

- 6.4.3 Schuberth GmbH

- 6.4.4 Shoei Co., Ltd.

- 6.4.5 HJC Helmets

- 6.4.6 LS2 Helmets

- 6.4.7 Shark Helmets

- 6.4.8 LIVALL Tech Co., Ltd.

- 6.4.9 Jarvish Inc.

- 6.4.10 CrossHelmet (Borderless Inc.)

- 6.4.11 Forcite Helmet Systems

- 6.4.12 Quin Design

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment