PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062311

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062311

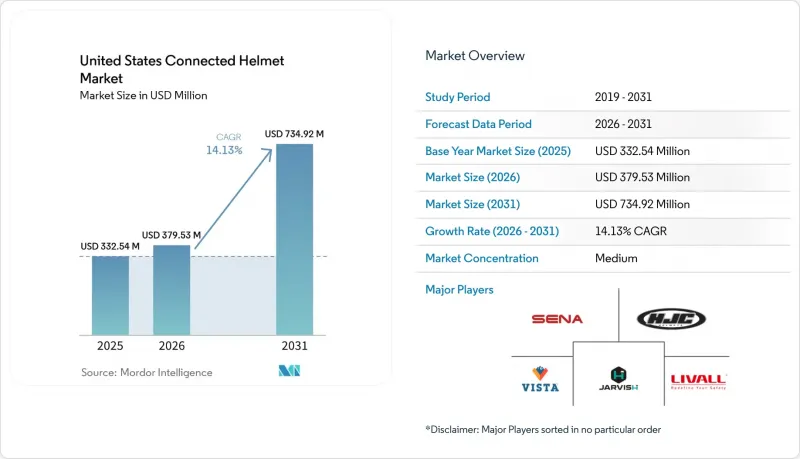

United States Connected Helmet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states connected helmet market size is projected to grow from USD 332.54 million in 2025 to USD 379.53 million in 2026 and is forecast to reach USD 734.92 million by 2031, growing at a CAGR of 14.13% from 2026 to 2031.

This report is Segmented by Product Type (Full Face, Modular/Flip-up, and More), Technology Level (Bluetooth-Only, Integrated Audio/Comms, and More), End User (Individual Rider, Passenger, and Fleet/Delivery), Distribution Channel (Offline Retail and Online Direct-To-Consumer), and Price Range (Economy, Mid-Range, and Premium). The Market Forecasts are Provided in Terms of Value (USD).

United States Connected Helmet Market Trends and Insights

Stringent DOT-Compliant Safety Mandates In U.S. States

Several states have enacted universal motorcycle helmet laws. In response, OEMs are embedding connected verification methods, such as NFC tags, enabling roadside officers to easily verify DOT compliance. The decision to halt liner-thickness screenings eliminated immediate certification hurdles. This change enables brands to integrate sensors without requiring new FMVSS tests . While voluntary Snell standards introduce oblique-impact metrics, premium helmets already tout these as a marketing edge. Enforcement varies: California employs random checkpoints, while other states are more lenient. This discrepancy drives the adoption of geofenced firmware, ensuring proof of compliance is uploaded in stricter areas. As the industry anticipates future biomechanical mandates, R&D teams feel the pressure to balance shell energy dispersion with rising electronic density.

Expansion of Direct-To-Consumer E-Commerce Channels

Online portals are revolutionizing the buying experience by combining detailed listings, real-time stock visibility, and instant firmware downloads, making it hard for physical dealerships to compete. Forcite's configurator, which offers shell sizing and LED previews, has successfully reduced return rates linked to sizing issues. Younger riders are increasingly drawn to unboxing videos, Reddit AMAs, and YouTube reviews featured on product pages, creating a feedback loop that enhances conversion rates. However, these robust digital footprints can serve as evidence in liability lawsuits. To counter this, brands are turning to third-party validations, backing up claims such as "crash notification." Additionally, analytics from payment gateways are being harnessed to forecast demand, streamlining just-in-time production of carbon shells and subsequently reducing working capital needs.

High Upfront Cost Versus Conventional Helmets

Connected helmets, priced between a range for Sena's Phantom and Schuberth's E2 Carbon, command a premium over DOT-approved shells that already meet legal requirements. Shoei's GT-Air 3 Smart is tailored for riders of high-end touring bikes, sidelining budget commuters. Lifecycle costs, including battery replacements and emergency service subscriptions, increase the annual outlay. While insurer discounts can offset the price over time, adoption hinges on riders' willingness to share location data. In states lacking helmet laws, some buyers forgo helmets entirely, exacerbating the price gap.

Other drivers and restraints analyzed in the detailed report include:

- Integration of V2X Chips Enabling Group-Riding Networks

- Insurance-Premium Discounts For Verified Connected-Helmet Use

- Limited Battery Life For Long-Distance Touring

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-face helmets accounted for 37.26% of the United States connected helmet market share in 2025, benefiting riders who emphasize wind noise reduction at highway speeds. The segment evolves as OEMs embed recesses for V2X antennas without adding drag. HUD-equipped models expand at a 14.67% CAGR, supported by Shoei's GT-Air 3 Smart that projects FHD navigation cues three meters ahead of the rider's line of sight, yielding 32% quicker reaction times in simulator trials. Modular flip-ups attract adventure riders who need chin-bar flexibility, while LIVALL pioneers open-face designs with bone-conduction speakers that avoid blocking ear canals.

Touring enthusiasts still favor carbon-fiber shells for weight savings. Still, mid-range fiberglass builds from Sena's Specter show that mesh intercom and Safe Power Mode can coexist with aggressive pricing. Off-road helmets now include LED floods for night trails, broadening use cases beyond paved roads. Regulatory cap-on-projection height forces hidden camera modules inside EPS liners, so brands patent energy-dispersion channels to route impact forces around electronics.

Integrated audio accounted for 33.19% of the United States connected helmet market share in 2025, propelled by rider-to-rider mesh compatibility. Yet ADAS sensor suites, apart from audio, see a 14.34% CAGR as insurers reward eCall functionality. In the coming years, the U.S. market for helmets equipped with ADAS features is poised for rapid expansion. Shoei's HUD, utilizing Sony's OLEDoS micro-display, boasts high brightness - a feature previously exclusive to automotive clusters. Forcite integrates GPS, video, and LED navigation halos into its platform but grapples with battery-drain issues, prompting OEMs to consider swappable cell trays.

As Bluetooth modules become ubiquitous, the emphasis shifts to software innovations that leverage AI to filter out wind noise and seamlessly connect to cloud services. While multi-band antennas address V2X and LTE fallback needs, they introduce additional tuning challenges. With SAE nearing the finalization of cooperative-perception payloads, the importance of firmware roadmaps rivals that of shell materials, underscoring the growing stakes in interoperability.

List of Companies Covered in this Report:

- Sena Technologies Inc.

- Vista Outdoor

- HJC Helmets

- Dainese (AGV)

- Schuberth GmbH

- Shoei Co. Ltd.

- Jarvish Inc.

- CrossHelmet (Borderless Inc.)

- LIVALL Tech Co. Ltd.

- Forcite Helmet Systems

- Quin Design

- Skully Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Dot-Compliant Safety Mandates In U.S. States

- 4.2.2 Expansion Of Direct-To-Consumer E-Commerce Channels

- 4.2.3 Integration Of V2X Chips Enabling Group-Riding Networks

- 4.2.4 Micromobility Fleet Operators Mandating Smart Helmets

- 4.2.5 Insurance-Premium Discounts For Verified Connected-Helmet Use

- 4.2.6 Federal Iija Roadside V2X Pilots Accelerating Ecosystem

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost Versus Conventional Helmets

- 4.3.2 Limited Battery Life For Long-Distance Touring

- 4.3.3 Bluetooth/Wi-Fi Spectrum Congestion In Urban Corridors

- 4.3.4 Data-Privacy Liability Concerns For Fleet Operators

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Full Face

- 5.1.2 Modular / Flip-up

- 5.1.3 Open Face

- 5.1.4 Half Helmet

- 5.1.5 Off-road / Motocross

- 5.1.6 Smart HUD-Integrated

- 5.2 By Technology Level

- 5.2.1 Bluetooth-Only

- 5.2.2 Integrated Audio / Comms

- 5.2.3 HUD / AR Display

- 5.2.4 Crash Detection & eCall

- 5.2.5 ADAS Sensor Suite

- 5.2.6 Multi-Feature (All-in-One)

- 5.3 By End User

- 5.3.1 Individual Rider

- 5.3.2 Passenger

- 5.3.3 Fleet / Delivery

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail

- 5.4.2 Online Direct-to-Consumer

- 5.5 By Price Range

- 5.5.1 Economy

- 5.5.2 Mid-Range

- 5.5.3 Premium

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Sena Technologies Inc.

- 6.4.2 Vista Outdoor

- 6.4.3 HJC Helmets

- 6.4.4 Dainese (AGV)

- 6.4.5 Schuberth GmbH

- 6.4.6 Shoei Co. Ltd.

- 6.4.7 Jarvish Inc.

- 6.4.8 CrossHelmet (Borderless Inc.)

- 6.4.9 LIVALL Tech Co. Ltd.

- 6.4.10 Forcite Helmet Systems

- 6.4.11 Quin Design

- 6.4.12 Skully Technologies Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment