PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062321

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062321

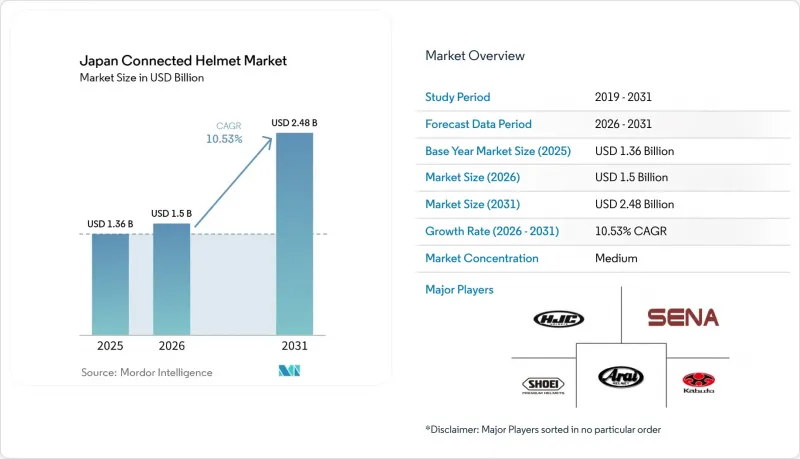

Japan Connected Helmet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan-connected helmet market size is expected to increase from USD 1.36 billion in 2025 to USD 1.50 billion in 2026 and reach USD 2.48 billion by 2031, growing at a CAGR of 10.53% over 2026-2031.

This report is Segmented by Product Type (Full Face, Modular/Flip-up, and More), Connectivity and Feature Level (Bluetooth-Only, Integrated Audio/Comms, and More), End User (Individual Rider and More), Distribution Channel (Offline Retail and More), Price Range (Economy and More), and Geography (Kanto, Kansai, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume in Units.

Japan Connected Helmet Market Trends and Insights

Accelerated Roll-out of 5G/4G LTE-V2X Along Japan's Expressways

The Ministry of Internal Affairs and Communications initiated the installation of roadside units on the Shin-Tomei Expressway. This advancement enables helmets to receive real-time hazard warnings without connecting to a smartphone. With plans to expand to the Tomei, Meishin, and Chugoku corridors, manufacturers will establish a nationwide H2I backbone. This shift is steering competition towards V2X-native chipsets. Delivery fleets stand to gain significantly by receiving lane-closure alerts earlier than GPS navigation, thereby reducing the risk of rear-end collisions. However, a disparity remains: secondary roads, still dependent on a 4G fallback, experience added latency. Consequently, a two-tier market has emerged: metropolitan riders are leaning towards V2X-ready helmets, while their rural counterparts prefer Bluetooth-only models.

OEM-Backed "Smart-helmet-as-a-Service" Bundles

Shoei unveiled the GT-Air 3 Smart, featuring an OLED heads-up display, available for financing alongside motorcycle loans . By shifting from one-time sales to recurring fee bundles, OEMs gain valuable telemetry insights for product design. However, this strategy poses a risk of channel conflict with aftermarket dealers. While older riders lean towards outright ownership, commuters are gravitating towards pay-per-feature tiers, significantly reducing their upfront costs. Early adopters are predominantly found in Kanto and Kansai, regions where dealerships are equipped to manage fittings and firmware updates. Conversely, in rural prefectures, limited dealer networks hinder subscription adoption, presenting a potential avenue for virtual onboarding and mail-in fitting services.

High Replacement Cost of Li-ion Battery Packs in Humid Coastal Regions

In Pacific prefectures, the salty air corrodes charging contacts, significantly reducing battery life. With replacement modules costing more, the total cost of ownership exceeds that of non-connected helmets. While manufacturers haven't introduced swap programs, coastal riders are either delaying upgrades or opting for Bluetooth-only shells with user-replaceable modules. Concerns over safety prevent consumers from using third-party batteries without PSC marks, effectively tying them to expensive OEM parts. This financial burden is hindering the adoption of premium helmets in Okinawa and Shizuoka, even though riding conditions are quite inviting.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Premium Touring and Adventure Bike Sales Among 40-plus Riders

- Mandatory Use of PSC/SG Standards for In-helmet Electronics from 2026

- RF Spectrum Congestion for Bluetooth 5.x in Dense Tokyo Corridors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full face designs held 45.88% of the Japanese connected helmet market share in 2025 because Shoei and Arai dominate premium safety certification. Smart HUD-integrated models, led by Shoei's GT-Air 3 Smart, are forecast at a 12.49% CAGR, reflecting falling micro-display prices and PSC-compliant battery packs.

Modular and flip-up shells attract touring riders who prioritize easy donning, while open-face and half helmets stay below 15% because limited surface area constrains electronics placement. Off-road helmets add action-camera mounts but struggle to fit six-hour batteries without exceeding weight targets. The segment's inflection lies in retrofit kits: CrossHelmet's X1-NKD ships without electronics and lets buyers snap in HUD and sensor pods later, shifting revenue toward upgrade accessories.

Integrated audio/comms accounted for 41.22% of the Japan-connected helmet market in 2025, yet ADAS sensor-suite models grew at a 13.22% CAGR as delivery fleets chase telematics-verified safety bonuses. Uber Eats mandates SG-marked helmets with visual verification, steering couriers toward radar-equipped shells that trigger app unlock only when worn.

HUD/AR helmets remain premium at USD 1,100-1,800, and all-in-one units face reliability issues due to short battery life. Crash-detection and eCall capabilities gain policy support, with Japan's transport ministry studying mandatory eCall by 2028. Manufacturers, therefore, release mid-priced helmets that pair basic Bluetooth intercom with accelerometer-based crash alerts to balance cost and compliance.

List of Companies Covered in this Report:

- Shoei Co., Ltd.

- Arai Helmet Ltd.

- Sena Technologies, Inc.

- OGK Kabuto Co., Ltd.

- HJC Helmets

- Dainese SpA

- Schuberth GmbH

- Bell Helmets

- BMW Motorrad

- Jarvish Inc.

- LS2 Helmets

- Shark Helmets

- Torc Helmets

- LIVALL Tech Co., Ltd.

- Klim (Polaris Inc.)

- VOZZ Helmets

- STUDDS Accessories Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Roll-Out Of 5G/4G LTE-V2X Along Japan's Expressways

- 4.2.2 OEM-Backed "Smart-Helmet as a Service" (Subscription Bundles)

- 4.2.3 Rise In Premium Touring and Adventure Bike Sales Among 40-Plus Riders

- 4.2.4 Mandatory Use Of PSC/SG Standards for In-Helmet Electronics From 2026

- 4.2.5 Ride-Share Insurers Offering 10-15 % Discounts for IoT-Verified Helmets

- 4.2.6 Growing Popularity of Group-Riding Social Networks (LINE And Biker-SNS)

- 4.3 Market Restraints

- 4.3.1 High Replacement Cost of Li-Ion Battery Packs in Humid Coastal Regions

- 4.3.2 RF Spectrum Congestion for Bluetooth 5.X In Dense Tokyo Corridors

- 4.3.3 Fragmented Prefectural Privacy Rules for Accident-Telemetry Storage

- 4.3.4 Limited Consumer Awareness Outside Kanto/Kansai Urban Clusters

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD and Volume in Units)

- 5.1 By Product Type

- 5.1.1 Full Face

- 5.1.2 Modular / Flip-up

- 5.1.3 Open Face

- 5.1.4 Half Helmet

- 5.1.5 Off-road / Motocross

- 5.1.6 Smart HUD-Integrated

- 5.2 By Connectivity and Feature Level

- 5.2.1 Bluetooth-Only

- 5.2.2 Integrated Audio / Comms

- 5.2.3 HUD / AR Display

- 5.2.4 Crash Detection and eCall

- 5.2.5 ADAS Sensor Suite

- 5.2.6 Multi-Feature (All-in-One)

- 5.3 By End User

- 5.3.1 Individual Rider

- 5.3.2 Passenger

- 5.3.3 Fleet / Delivery

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail

- 5.4.2 Online Direct-to-Consumer

- 5.4.3 OEM Accessory Bundles

- 5.5 By Price Range

- 5.5.1 Economy

- 5.5.2 Mid-Range

- 5.5.3 Premium

- 5.6 By Region

- 5.6.1 Kanto

- 5.6.2 Kansai

- 5.6.3 Chubu

- 5.6.4 Kyushu and Okinawa

- 5.6.5 Hokkaido and Tohoku

- 5.6.6 Chugoku

- 5.6.7 Shikoku

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Shoei Co., Ltd.

- 6.4.2 Arai Helmet Ltd.

- 6.4.3 Sena Technologies, Inc.

- 6.4.4 OGK Kabuto Co., Ltd.

- 6.4.5 HJC Helmets

- 6.4.6 Dainese SpA

- 6.4.7 Schuberth GmbH

- 6.4.8 Bell Helmets

- 6.4.9 BMW Motorrad

- 6.4.10 Jarvish Inc.

- 6.4.11 LS2 Helmets

- 6.4.12 Shark Helmets

- 6.4.13 Torc Helmets

- 6.4.14 LIVALL Tech Co., Ltd.

- 6.4.15 Klim (Polaris Inc.)

- 6.4.16 VOZZ Helmets

- 6.4.17 STUDDS Accessories Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment