PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062380

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062380

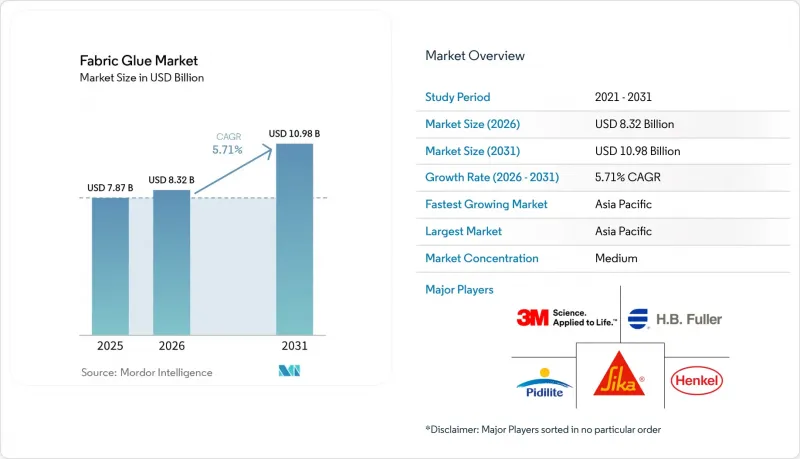

Fabric Glue - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the fabric glue market size is expected to grow from USD 7.87 billion in 2025 to USD 8.32 billion in 2026 and is forecast to reach USD 10.98 billion by 2031 at 5.71% CAGR over 2026-2031.

This report is Segmented by Product Type (Temporary Fabric Glue and Permanent Fabric Glue), Base Chemistry (Water-Based (PVA, EVA) and More), Distribution Channel (Online Marketplaces, and More), End-User Industry (Clothing and Apparel and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Fabric Glue Market Trends and Insights

Rapid On-Demand Fashion Cycles

Fast-fashion platforms introduce thousands of new stock-keeping units (SKUs) daily, prompting factories to replace traditional sequential sewing with automated spray or roller adhesive lines, reducing labor requirements by 30-40%. Polyester and nylon blends bonded with thermoplastic hot-melts achieve peel strengths exceeding 15 N/25 mm, sufficient for garments designed to endure 10-20 wash cycles. Instant tack and minimal cure times make reactive polyurethane and ethylene-vinyl-acetate copolymers favorable choices. Suppliers are optimizing rheology to ensure formulations operate efficiently on high-speed conveyor systems without stringing. Chinese converters have adopted dual-head robots capable of dispensing adhesives in variable patterns, reducing overspray and cutting material usage by 8-10%. Brands incentivize such technological advancements with extended contracts, ensuring consistent demand for higher-margin specialty chemistries.

Surge in Technical-Textile Bonding (PPE, E-Textiles)

Protective garments for healthcare, firefighting, and hazardous-material handling now require multi-layer laminates, replacing stitched seams that previously served as weak points. Adhesive interlayers provide liquid-tight yet breathable barriers, while conductive grades ensure circuit integrity for wearable sensors. Henkel AG & Co. KGaA's silver-flake-filled polyurethane, introduced in 2025, maintains resistivity below 10 Ω/sq even after 50 wash cycles. Military tenders in Japan demand wash-durable bonds capable of withstanding 250,000-cycle flex testing, driving research and development (R&D) into hybrid polymer networks. Suppliers are also targeting medical diagnostics, where flexible electrodes must endure autoclave sterilization at 134°C, a challenge that standard ethylene-vinyl acetate (EVA) cannot meet.

Volatile Vinyl-Acetate and Isopropanol Feedstock Prices

Vinyl-acetate monomer prices ranged between USD 950 and USD 1,150 per ton during 2024-2025, influenced by Middle-East supply disruptions and freight challenges affecting Asian buyers. Isopropanol prices followed crude oil volatility and were impacted by Chinese export restrictions, leading to contract values increasing by 12-18% compared to 2023 levels. Small South-Asian formulators experienced gross margin reductions of 200-300 basis points as buyers resisted mid-contract price adjustments. Without hedging mechanisms, two Bangladeshi producers reported negative margins in Q4 2024, losing market share to larger competitors with long-term supply agreements.

Other drivers and restraints analyzed in the detailed report include:

- Bio-Based Polymer Breakthroughs Enabling Sewing Replacement

- Adoption of Low-Energy Cold-Bonding Processes

- Microplastic-Shedding Regulations on Synthetic Glues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Temporary formulations are expected to grow at a compound annual growth rate (CAGR) of 6.10%, gaining adoption in design studios where repositionability is prioritized over durability. Permanent grades accounted for 59.11% of 2025 revenue, driven by demand in footwear, upholstery, and home textiles, where adhesives must withstand years of wear and laundering. Semi-permanent chemistries, offering 15-minute open times, enable adjustments before thermal crosslinking. For example, Loctite MS 9650, a moisture-curing silane polymer, achieves a peel strength of 18 N/25 mm after 24 hours while allowing rework during assembly.

Design studios prefer pin-free prototyping as it preserves fabric surfaces for marketing photography. Online tutorials highlight how temporary sprays facilitate pattern adjustments, boosting demand among hobbyists and small brands. Since both temporary and permanent adhesives must comply with identical volatile organic compound (VOC) and microplastic regulations, differentiation focuses on packaging and viscosity control. Craft-oriented aerosols command a 30-40% price premium, reflecting consumer preference for convenience over resin cost. Industrial buyers, however, continue to favor bulk drums to optimize unit economics, maintaining a tiered pricing structure within the fabric glue market.

Water-based emulsions contributed 48.22% of 2025 revenue due to their near-zero volatile organic compound (VOC) profiles, aligning with Environmental Protection Agency (EPA) Rule 1168. However, bio-based dispersions are projected to grow at a CAGR of 6.51% through 2031. Manufacturers are expanding the fabric glue market by utilizing vegetable-oil polyols, which match the melt viscosity and set speed of ethylene-vinyl acetate (EVA) while reducing carbon footprints by up to 40%. Hot-melt adhesives remain critical for high-speed production lines; for instance, Henkel AG & Co. KGaA's Technomelt PUR 6260 ECO, with 60% renewable content, bonds elastane without thermal yellowing at 180°C.

Solvent-based neoprenes are increasingly confined to niche applications like leather due to rising compliance costs under Occupational Safety and Health Administration (OSHA) and European Union (EU) regulations. However, their instant tack keeps them relevant for athletic footwear bonding. Reactive polyurethane (PUR) adhesives, which crosslink under moisture, dominate technical textile applications requiring wash durability beyond 50 cycles. The growth of bio-based adhesives faces challenges from feedstock volatility, as castor-oil harvests fluctuate with monsoon patterns, causing 20% price swings. Hybrid systems blending bio-based and petrochemical components mitigate this volatility while qualifying for eco-labels, providing large multinationals with integrated supply chains a competitive advantage.

Geography Analysis

Asia-Pacific accounted for 43.45% of the projected 2025 revenue and is expected to achieve a 6.81% compound annual growth rate (CAGR) through 2031, highlighting its role as a production hub and a growth market for finished goods. In China, Huafon Chemical is investing RMB 3.6 billion (USD 500 million) in a 200,000 tons per year spandex production line, which will utilize reactive polyurethane (PUR) adhesives for elastane lamination. Additionally, RAMPF Group inaugurated a EUR 8 million (USD 8.5 million) polyurethane systems plant in Tianjin in July 2026 to localize supply for automotive and sportswear converters. In India, Pidilite, which holds over 70% of the domestic market share, reported an 11% Q3 FY26 revenue growth driven by technical-textile dispersions. Meanwhile, Vietnam, now the second-largest textile exporter with USD 44 billion in shipments in 2024, is absorbing orders rerouted from Bangladesh, boosting adhesive demand for short-run production.

North America and Europe collectively contribute stable but slower growth due to market maturity and stringent regulations. In the European Union, microplastic regulations are prompting reformulations toward bio-based or non-shedding chemistries, extending development cycles by up to a year. In the United States, state-level volatile organic compound (VOC) regulations in Maryland, Virginia, and Pennsylvania limit adhesive emissions to 50-150 grams per liter (g/L), encouraging a shift toward water-based or hot-melt systems. Mexico's nearshoring trend is driving adhesive consumption closer to U.S. brands seeking resilient supply chains. Technical-textile and automotive production lines migrating from Asia are increasing demand for high-performance polyurethane (PUR) and ultraviolet (UV)-curable adhesives with short lead times.

South America and the Middle East-Africa regions represent smaller market shares but offer areas of significant growth. Pidilite's expansion into African markets is achieving 40% annual growth, leveraging distributor partnerships to reach craft and furniture manufacturers. In Brazil, the textile sector is shifting toward export-oriented technical fabrics, necessitating Bluesign-approved adhesives as European buyers enforce sustainability audits. Turkey's customs-union access to the European Union is driving demand for low-VOC, microplastic-compliant adhesives. In South Africa, automotive seat suppliers are transitioning to low-emission hot-melts to comply with European original equipment manufacturer (OEM) cabin air quality standards, a trend expected to extend into local furniture and apparel subsectors.

- 3M

- Arkema

- Beacon Adhesives Inc.

- Buhnen GmbH & Co. KG

- CHEMENCE

- Eclectic Products, LLC

- Gorilla Glue, Inc

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- iLoveToCreate

- Mitreapel

- Permabond

- Permatex Inc.

- Pidilite Industries Ltd.

- Sika AG

- Therm O Web

- Weldbond Adhesives

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid On-Demand Fashion Cycles

- 4.2.2 Surge in Technical-Textile Bonding (PPE, E-Textiles)

- 4.2.3 Bio-Based Polymer Breakthroughs Enabling Sewing Replacement

- 4.2.4 Adoption of Low-Energy Cold-Bonding Processes in Apparel Factories

- 4.2.5 E-commerce Micro-Brands Demanding Flexible Production Adhesives

- 4.3 Market Restraints

- 4.3.1 Volatile Vinyl-Acetate and Isopropanol Feedstock Prices

- 4.3.2 Micro-Plastic-Shedding Regulations on Synthetic Glues

- 4.3.3 Worker-Exposure Limits Tightening on Solvent-Based Adhesives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Temporary Fabric Glue

- 5.1.2 Permanent Fabric Glue

- 5.2 By Base Chemistry

- 5.2.1 Water-Based (PVA, EVA)

- 5.2.2 Solvent-Based (Neoprene, PU)

- 5.2.3 Hot-Melt (EVA, TPU)

- 5.2.4 Reactive PUR

- 5.2.5 Bio-Based Dispersions

- 5.3 By Distribution Channel

- 5.3.1 Online Marketplaces

- 5.3.2 Specialty Craft Stores

- 5.3.3 Supermarkets and Hypermarkets

- 5.3.4 Textile Raw-Material Distributors

- 5.3.5 Direct-to-Factory

- 5.4 By End-User Industry

- 5.4.1 Clothing and Apparel

- 5.4.2 Home Textiles

- 5.4.3 Footwear and Leather Goods

- 5.4.4 Automotive Upholstery and Interiors

- 5.4.5 Furniture and Mattress

- 5.4.6 Crafts, DIY and Hobby

- 5.4.7 Industrial Protective Textiles

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Beacon Adhesives Inc.

- 6.4.4 Buhnen GmbH & Co. KG

- 6.4.5 CHEMENCE

- 6.4.6 Eclectic Products, LLC

- 6.4.7 Gorilla Glue, Inc

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 iLoveToCreate

- 6.4.11 Mitreapel

- 6.4.12 Permabond

- 6.4.13 Permatex Inc.

- 6.4.14 Pidilite Industries Ltd.

- 6.4.15 Sika AG

- 6.4.16 Therm O Web

- 6.4.17 Weldbond Adhesives

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment