PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066664

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066664

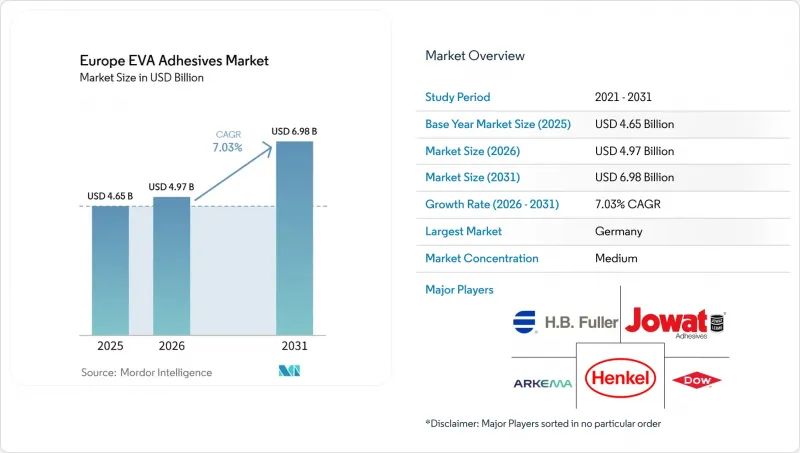

Europe EVA Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the eVA-based adhesives market size is projected to be USD 4.65 billion in 2025, USD 4.97 billion in 2026, and reach USD 6.98 billion by 2031, growing at a CAGR of 7.03% from 2026 to 2031.

This report is Segmented by Technology (Hot Melt, Solvent-Borne, Water-Borne), End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, Other End-User Industries), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

Europe EVA Adhesives Market Trends and Insights

Explosive Growth of E-commerce-driven Packaging Demand

E-commerce shippers face challenges with automated sortation drops of 1.2 m and temperature fluctuations ranging from -15 °C to 35 °C, testing the limits of starch glues. EVA hot melts, offering 8-12 second open times, achieve a green strength of 1.5 N/25 mm in just three seconds. This efficiency allows corrugators to operate at 400 m/min without seal failures. While parcel growth has stabilized, the shift towards mono-material boxes, which are more compatible with recycling, continues to drive up adhesive volumes. New specifications now favor copolymers with less than 5 wt% vinyl acetate, as they successfully meet the RecyClass- Association of Plastic Recyclers (APR) CG-01 protocols. Arkema's acquisition of Dow's flexible-packaging adhesive line in December 2024 highlights the industry's focus on solvent-free formulations, especially those aligning with Nestle's migration limits. Over the next two years, as converters complete trials on low-VA systems, their influence is set to peak, especially with plans to scale these systems across multiple plants.

EU Renovation Wave Boosting Construction Adhesives

By 2030, the Renovation Wave aims to boost Europe's building-renovation rate to 2% annually, directing EUR 72.2 billion towards facade and roof enhancements. EVA-modified dispersions, which bond insulation panels to masonry, sidestep the thermal bridges associated with mechanical anchors and meet the EU Ecolabel VOC standards. Thanks to their national recovery plans, which allocate 35-40% of EU funds for energy retrofits, Italy and Spain are rapidly advancing. Water-borne EVA systems, boasting tack times of 25-30 minutes, twice that of vinyl-acetate homopolymers, are easing labor demands for installers, especially amidst a 15-20% shortage in trade skills.

Rising Competition from POE & TPU in High-Performance Niches

Metallocene polyolefin elastomers, which shave off 40% of application weight, endure 2,000 hours at 150 °C, making them prime candidates for EV battery packs. After curing, thermoplastic-polyurethane reactives achieve a lap-shear strength of 15-18 MPa, allowing footwear brands to eliminate stitching altogether. While these alternatives come with a 20-30% price premium, they offer significant value in weight-sensitive or high-temperature settings. In response, EVA suppliers are introducing grades with 33-40% VA content, but this move escalates raw material costs by 25 to 30%.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Low-VOC/Water-borne Platforms Under REACH

- OEM Push for Lightweight EV Interiors

- End-of-Life Recycling Barriers for EVA-Bonded Laminates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, water-borne dispersions commanded a 45.20% share of the market demand. However, hot melts are on a trajectory to surpass them, boasting a 7.89% CAGR projected through 2031. By eliminating drying ovens, manufacturers can save between 0.8 to 1.2 kWh for every kilogram produced. This also frees up 15 to 20 meters of line space, which is a crucial advantage given the current surge in energy prices. In the automotive segment, tier-1 suppliers are capitalizing on 8 to 12 second open times for robotic assembly, achieving a rate of 50 units per hour. This marks a significant 40% improvement over the dwell times required for water-borne alternatives. In terms of material performance, crosslinkable EVA hot melts are now achieving lap-shear strengths of 12 to 15 MPa at 80 °C. This presents a cost-effective challenge to traditional polyurethane reactives. For solvent-borne systems, a continued decline is expected as workplace VOC ceilings tighten next year. While niche applications in luxury footwear and leather remain, even in these segments, polyurethane reactives are gradually encroaching on market share.

List of Companies Covered in this Report:

- 3M Company

- Arkema

- Avery Dennison Corp.

- BASF SE

- Beardow Adams

- Celanese Corp.

- Dow

- Follmann Chemie GmbH

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman Corp.

- Jowat SE

- Klebchemie M.G. Becker GmbH

- LyondellBasell Industries

- Paramelt B.V.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of e-commerce-driven packaging demand

- 4.2.2 EU Renovation Wave boosting construction adhesives

- 4.2.3 Shift to low-VOC/water-borne platforms under REACH

- 4.2.4 OEM push for light-weight EV interiors

- 4.2.5 High-VA, bio-based EVA grades gaining premium adoption

- 4.3 Market Restraints

- 4.3.1 Feed-stock (ethylene and VAM) price volatility

- 4.3.2 Rising competition from POE and TPU in high-performance niches

- 4.3.3 End-of-life recycling barriers for EVA-bonded laminates

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Hot Melt

- 5.1.2 Solvent-borne

- 5.1.3 Water-borne

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Footwear and Leather

- 5.2.5 Healthcare

- 5.2.6 Packaging

- 5.2.7 Woodworking and Joinery

- 5.2.8 Other End-user Industries

- 5.3 By Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M Company

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corp.

- 6.4.4 BASF SE

- 6.4.5 Beardow Adams

- 6.4.6 Celanese Corp.

- 6.4.7 Dow

- 6.4.8 Follmann Chemie GmbH

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman Corp.

- 6.4.12 Jowat SE

- 6.4.13 Klebchemie M.G. Becker GmbH

- 6.4.14 LyondellBasell Industries

- 6.4.15 Paramelt B.V.

- 6.4.16 Sika AG

- 6.4.17 Soudal Holding N.V.

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment