PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066663

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066663

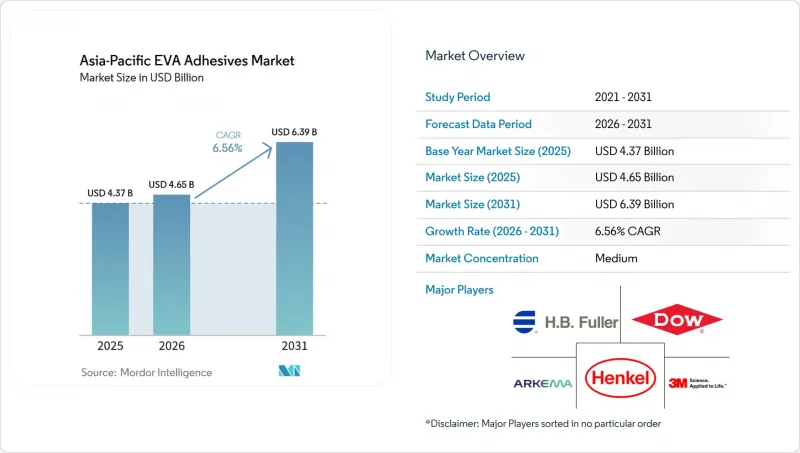

Asia-Pacific EVA Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific eVA-based adhesives market, valued at USD 4.37 billion in 2025, is projected to grow to USD 4.65 billion in 2026 and reach USD 6.39 billion by 2031, marking a CAGR of 6.56% from 2026 to 2031.

This report is Segmented by Technology (Hot-Melt, Solvent-Borne, Water-Borne), End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Other End-User Industries), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, Rest of Asia-Pacific). Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific EVA Adhesives Market Trends and Insights

E-Commerce Boom Driving Hot-Melt Packaging Demand

Cross-border fulfillment centers are increasingly adopting EVA hot-melt systems. These systems eliminate drying steps and reduce line downtime by 30-40%. This trend bolsters the EVA-based adhesives market in the Asia-Pacific region. In China, food-contact migration limits, as per GB 9685-2016, and Japan's Food Sanitation Law, are driving up demand for low-odor grades. Henkel inaugurated its EUR 60 million Shanghai Inspiration Center in 2025. The center can prototype custom hot-melts in just 48 hours, enabling brand owners to expedite their qualification cycles. With rising minimum wages, automation has led to a reduction of two to three operators per packaging line. While these advancements are notable, they come against the backdrop of slowing consumption in China.

Footwear Automation Spurring Low-Temperature EVA Uptake

In 2024, Aica Kogyo, after collaborating with OEMs to develop 15-20 second open-time formulations, achieved hot-melt sales of JPY 74.74 billion in the Asia-Pacific region. Automated shoe plants in Guangdong and Dong Nai, utilizing EVA grades with activation points between 90-110 °C, have successfully minimized heat damage while maintaining a throughput of 1,200 pairs per hour. Additionally, EVA provides a buffer against price fluctuations in natural rubber, thanks to quarterly VAM contracts. While this advantage is primarily seen in Vietnam and Indonesia, it stands to diminish if global footwear sourcing undergoes tariff-induced shifts.

Volatile VAM Feedstock Prices

In Japan, the spot price of Vinyl Acetate Monomer (VAM) jumped from USD 816/ton in Q1 2025 to USD 943/ton by Q4. This price surge has squeezed converters' EBITDA by as much as 5%. Smaller players, unable to hedge, face 30-60 day pricing lags, jeopardizing their relationships. Meanwhile, H.B. Fuller's "Project Quantum Leap" aims to centralize VAM procurement, allowing the company to secure fixed-price collars and target annual savings of USD 150 million. As a result, the divide between integrated multinationals and merchant buyers is widening, pushing the industry towards faster consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Medical-Grade EVA Films in APAC Healthcare

- Solar PV Encapsulation Capacity Additions in China and India

- Tight VOC Limits on Solvent-Borne Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, hot-melt adhesives held a dominant 64.28% share of the Asia-Pacific EVA-based adhesives market. However, water-borne grades are on the rise, boasting a robust CAGR of 7.56%. As converters adapt to meet VOC caps, the Asia-Pacific EVA-based adhesives market is set for growth. While water-borne systems offer benefits like reduced insurance premiums and easier operator training, challenges such as freeze-thaw issues hinder their adoption in cold chains. Highlighting a strategic shift, Henkel's Singapore Electronic Adhesives Technical Centre is moving away from solvent-borne R&D.

Water-borne systems' growth is closely tied to labor and compliance trends. By opting for water-borne systems, facilities sidestep the need for explosion-proof wiring, resulting in significant capital savings. NANPAO has demonstrated the potential for margin enhancement, with over 60% of its revenue mix now water-based, despite the longer drying cycles. Nevertheless, the ultra-fast e-commerce sector continues to lean towards hot-melt adhesives, suggesting a gradual shift in capital investment.

List of Companies Covered in this Report:

- 3M Company

- Aica Kogyo Co., Ltd.

- Arkema

- Avery Dennison Corp.

- Celanese Corporation

- CEMEDINE Co., Ltd.

- Dow

- ExxonMobil Chemical

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- NANPAO Resins Chemical Group

- OKONG Corp.

- Paramelt B.V.

- Pidilite Industries Ltd.

- Selic Corp PCL

- Sika AG

- Tex Year Industries Inc.

- Toyo Polymer Co., Ltd.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 End-User Trends

- 4.3 Market Drivers

- 4.3.1 E-commerce boom driving hot-melt packaging demand

- 4.3.2 Footwear automation spurring low-temperature EVA uptake

- 4.3.3 Shift to medical-grade EVA films in APAC healthcare

- 4.3.4 Solar PV encapsulation capacity additions in China and India

- 4.3.5 Bio-based EVA scale-up in Southeast Asia (under-reported)

- 4.4 Market Restraints

- 4.4.1 Volatile VAM feedstock prices

- 4.4.2 Tight VOC limits on solvent-borne lines

- 4.4.3 Competition from polyolefin pressure-sensitives

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.6.1 Australia

- 4.6.2 China

- 4.6.3 India

- 4.6.4 Indonesia

- 4.6.5 Japan

- 4.6.6 Malaysia

- 4.6.7 Singapore

- 4.6.8 South Korea

- 4.6.9 Thailand

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Technology

- 5.1.1 Hot-Melt

- 5.1.2 Solvent-Borne

- 5.1.3 Water-Borne

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Footwear and Leather

- 5.2.5 Healthcare

- 5.2.6 Packaging

- 5.2.7 Woodworking and Joinery

- 5.2.8 Other End-user Industries

- 5.3 By Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M Company

- 6.4.2 Aica Kogyo Co., Ltd.

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corp.

- 6.4.5 Celanese Corporation

- 6.4.6 CEMEDINE Co., Ltd.

- 6.4.7 Dow

- 6.4.8 ExxonMobil Chemical

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Jowat SE

- 6.4.12 NANPAO Resins Chemical Group

- 6.4.13 OKONG Corp.

- 6.4.14 Paramelt B.V.

- 6.4.15 Pidilite Industries Ltd.

- 6.4.16 Selic Corp PCL

- 6.4.17 Sika AG

- 6.4.18 Tex Year Industries Inc.

- 6.4.19 Toyo Polymer Co., Ltd.

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Key Strategic Questions for Adhesive and Sealant CEOs