PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063335

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063335

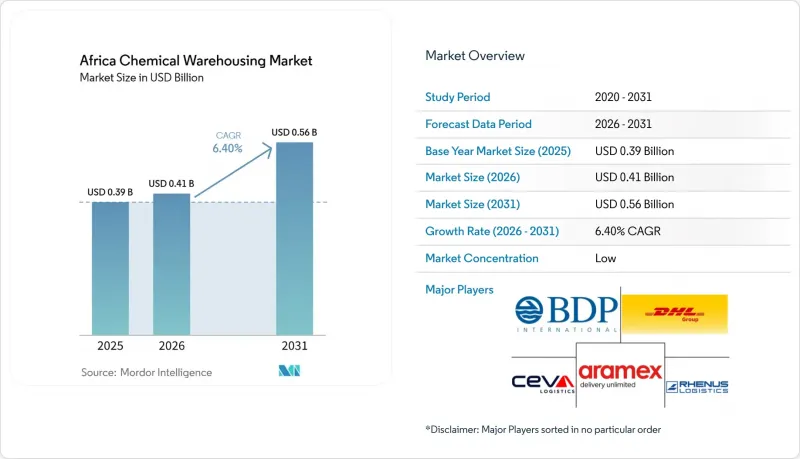

Africa Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the africa chemical warehousing market size was valued at USD 0.39 billion in 2025 and is estimated to grow from USD 0.41 billion in 2026 to reach USD 0.56 billion by 2031, at a CAGR of 6.40% during the forecast period (2026-2031).

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Geography (Nigeria, Morocco, Kenya, and More). The Market Forecasts are Provided in Terms of Value (USD).

Africa Chemical Warehousing Market Trends and Insights

Mining Sector Chemical Demand Growth

The African Union's Green Minerals Strategy shows that mines consume significant quantities of explosives, reagents, cyanide, and related chemical inputs after fuel, lubricants, and power, reinforcing the need for specialized storage at mine-adjacent and port-proximate depots. In South Africa, basic chemical input costs rose in 2025 alongside double-digit increases in electricity and water tariffs, which encouraged mining operators to maintain buffer stocks of sulfuric acid, hydrochloric acid, sodium hydroxide, and chlorine to avoid disruptions. These cost and reliability dynamics increase the role of compliant warehouses capable of segregating corrosives and toxics while supporting steady outbound flows to concentrators and smelters. South Africa's heavy-haul rail supports long-distance movement of bulk liquids and hazardous cargoes tied to mining value chains, aligning with storage networks around Gauteng and KwaZulu-Natal. As mines process lower-grade ores, their reagent intensity increases, which sustains demand for capacity with robust ventilation, secondary containment, and incident response standards in the Africa chemical warehousing market. This supports a steady pipeline of upgrades to warehousing layouts and monitoring systems to manage higher turnover and maintain SHEQ compliance across corridors.

Agricultural Input Market Expansion

Large-scale investments in nitrogen and ammonia-urea capacity in West Africa are expanding the regional supply base for fertilizer inputs and driving demand for compliant storage of urea, ammonia, and methanol, including segregation and inventory controls suited to oxidizers and toxics. As AfCFTA eliminates tariffs on most goods, cross-border flows of agrochemicals are expected to rise, which shifts warehousing footprints toward integrated, corridor-based nodes linked to major ports and inland gateways. Port-side liquid bulk capacity that can flex between edible oils and chemical cargoes supports agribusinesses that need both ambient and hazardous storage with strict hygiene and spill-control protocols. In Kenya, new special economic zones near Mombasa and in geothermal-powered Olkaria are designed to attract agro-processing, which raises the requirement for temperature-controlled and humidity-managed facilities for crop protection products. These trends favor operators that can pair cold-chain capabilities with regulatory documentation for dangerous goods to serve seasonal surges and port-to-inland distribution in the Africa chemical warehousing market. Compliance architectures that integrate labeling, monitoring, and emergency response help align agricultural chemical storage with evolving standards in key markets.

Inadequate Infrastructure and Logistics Networks

Infrastructure gaps and climate exposure generate sustained costs and delays, with average annual losses linked to climate-related events that weigh on the financial performance of transport and storage operations. These conditions magnify risks for hazardous cargo, where delays increase safety and compliance burdens in port yards and inland depots that are not designed for prolonged dwell. Multimodal pilots that shift volume toward rail with enhanced container security can reduce exposure on long-haul routes, but these networks remain nascent outside select corridors. High import reliance on fuel and feedstocks in major hubs sustains the need for tank farms and specialized storage capacity, while also increasing sensitivity to exchange rate swings that affect inventory financing. These systemic hurdles slow the diffusion of advanced warehousing technologies and limit redundancy in secondary cities that the Africa chemical warehousing market will need as regional trade grows.

Other drivers and restraints analyzed in the detailed report include:

- Oil and Gas Sector Development

- Manufacturing Sector Diversification

- Regulatory Fragmentation and Weak Enforcement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty Chemical Warehouses accounted for 37.41% in 2025, reflecting a clear shift toward compliance-intensive storage that supports higher value products across formulations, additives, and polymers in the Africa chemical warehousing market. Temperature-Controlled Chemical Warehouses are projected to grow at 6.74% during 2026-2031 as pharma localization and agrochemical handling standards push demand for validated cold rooms and humidity control, and the Africa chemical warehousing market size for this segment is expected to expand at a 6.74% CAGR through 2031. Hazardous Materials facilities remain essential for flammables, oxidizers, and toxics, particularly where national standards reference classification, packaging, and emergency response codes aligned with international benchmarks. SQAS-AFRICA certification is being used by leading shippers to screen providers that can maintain safe operations for dangerous goods across handling, storage, and incident response. In parallel, general warehousing continues to serve ambient commodities, though margins face pressure as clients require segregation, fire suppression, and access control that exceed legacy footprints in secondary cities. The Africa chemical warehousing industry is therefore favoring facilities that combine automation with audit-ready processes to win long-term contracts from multinationals.

Over 2026-2031, the mix is expected to tilt toward specialty and temperature-controlled sites as AfCFTA supports intra-regional distribution of APIs, excipients, and high-spec agrochemicals that rely on certified chains of custody. New SEZs in Kenya, alongside rail-linked terminals in South Africa, illustrate how policy and infrastructure combine to attract chemical-intensive manufacturing that requires compliant storage models near ports and rail. Port-adjacent liquid bulk terminals, such as Durban's 100,000 cubic meters of capacity, also reinforce a broader hub-and-spoke approach to inventory positioning for both edible oils and chemical cargoes. Operators that standardize labeling, monitoring, and air sampling per hazard-class rules are better positioned to meet audit requirements of global buyers in the Africa chemical warehousing market. This structure narrows the compliance gap and shifts procurement toward certified providers that integrate safety with visibility and data capture for sensitive cargo.

List of Companies Covered in this Report:

- DHL Group

- BDP International

- CEVA Logistics

- Aramex

- Rhenus Logistics

- Transnet Freight and Warehousing

- Hellmann Worldwide Logistics

- DSV

- Worldwide Logistics Group

- Unitrans Africa

- Robeck International Freight

- Value Chemical Logistics

- Impro Logistics

- Xeon

- SAS Logistics Ltd

- DACHSER

- Noatum Logistics

- Toll Group

- Fracht and Fracht Group

- DP World (Imperial Logistics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mining Sector Chemical Demand Growth

- 4.2.2 Agricultural Input Market Expansion

- 4.2.3 Oil and Gas Sector Development

- 4.2.4 Manufacturing Sector Diversification

- 4.2.5 Port Infrastructure Modernization

- 4.2.6 Pharmaceutical Manufacturing Localization

- 4.3 Market Restraints

- 4.3.1 Inadequate Infrastructure and Logistics Networks

- 4.3.2 Regulatory Fragmentation and Weak Enforcement

- 4.3.3 Shortage of Specialized Warehousing Facilities

- 4.3.4 High Import Dependency and Forex Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 Nigeria

- 5.4.2 Morocco

- 5.4.3 Kenya

- 5.4.4 South Africa

- 5.4.5 Ethiopia

- 5.4.6 Algeria

- 5.4.7 Rest of Africa

- 5.5 Impact of Geopolitical Events on the Market

- 5.6 Circular Economy Chemical Recycling

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 BDP International

- 6.4.3 CEVA Logistics

- 6.4.4 Aramex

- 6.4.5 Rhenus Logistics

- 6.4.6 Transnet Freight and Warehousing

- 6.4.7 Hellmann Worldwide Logistics

- 6.4.8 DSV

- 6.4.9 Worldwide Logistics Group

- 6.4.10 Unitrans Africa

- 6.4.11 Robeck International Freight

- 6.4.12 Value Chemical Logistics

- 6.4.13 Impro Logistics

- 6.4.14 Xeon

- 6.4.15 SAS Logistics Ltd

- 6.4.16 DACHSER

- 6.4.17 Noatum Logistics

- 6.4.18 Toll Group

- 6.4.19 Fracht and Fracht Group

- 6.4.20 DP World (Imperial Logistics)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment