PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063344

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063344

Middle East Third-Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

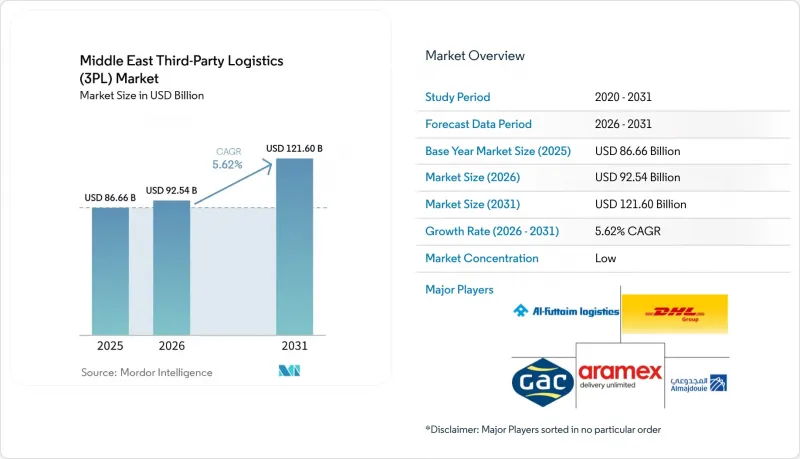

According to Mordor Intelligence, the middle east third-Party logistics market size is expected to increase from USD 86.66 billion in 2025 to USD 92.54 billion in 2026 and reach USD 121.60 billion by 2031, growing at a CAGR of 5.62% over 2026-2031.

Softer oil demand, diversified manufacturing growth, and steady e-commerce adoption underpin the trajectory, while clients now rank regulatory compliance, ESG reporting, and real-time visibility ahead of pure freight-rate considerations. This report is Segmented by Service (Domestic Transportation Management, International Transportation Management, and More), by End-User Industry (Automotive, Energy and Utilities, Life Sciences and Healthcare, and More), by Logistics Model (Asset-Light, and More), and by Country (United Arab Emirates, Saudi Arabia, Turkey, Oman, and More). The Market Forecasts are Provided in Terms of Value (USD).

Middle East Third-Party Logistics (3PL) Market Trends and Insights

Turkey-GCC Cross-Border E-commerce Accords Accelerating Small-Parcel Flows

Bilateral facilitation agreements slashed customs clearance from as high as 72 hours to 12-18 hours in 2024, which triggered a surge in Turkish e-commerce exports valued at USD 4.2 billion. Faster clearance reshaped the cost curve for air freight and automated sortation, letting 3PLs invest in bonded facilities near Turkish free-zone airports. Consolidated pre-cleared shipments now trim logistics costs by up to 30%, redirecting Gulf online retailers toward Turkey as a China-plus-one sourcing base. Dubai and Abu Dhabi serve as transshipment nodes, amplifying parcel densities that feed regional last-mile networks. Providers owning multi-country brokerage APIs are therefore winning contracts ahead of asset-heavy rivals limited to domestic fleets.

Green Sukuk Financing Spurring Roll-out of Solar-Powered, ESG-Certified Warehouses

Islamic green instruments mobilized USD 2.5 billion for logistics assets in 2024, cutting financing costs for developers that commit to measurable carbon metrics. The Public Investment Fund's USD 3 billion tranche earmarked a portion for LEED-rated distribution centers that underpin Vision 2030. Each facility must report energy intensity and renewable-power share, which embeds third-party audits into everyday operations. Larger 3PLs with in-house sustainability teams gain an edge, while smaller operators struggle with verification fees. In the UAE, a planned 500,000 sqm solar-powered park showcases how public-private initiatives reset the minimum ESG standard clients now expect.

Persistent Container-Equipment Imbalance Inflating Repositioning Costs on GCC Lanes

Empty-equipment transfers now cost importers USD 400-600 per TEU as Red Sea detours reduce inbound container pools. Carriers pass part of the burden to 3PLs locked in fixed-price contracts, eroding margins. Gulf import dominance versus lower export flows sustains the deficit, while alternative break-bulk solutions are unviable for FMCG shippers. Providers with repositioning alliances or container-sharing platforms can contain costs, but most mid-tier players face profitability headwinds until fleet geography normalizes.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen Export Mega-Projects Generating Demand for Cryogenic Bulk-Gas Logistics

- Mandatory GS1 Serialization in Saudi Pharma Supply Chains

- Slow GCC VAT-Framework Harmonization Complicating Bonded Cross-Border Movements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Value-added warehousing and distribution is set to grow at a 6.98% CAGR through 2031 as clients prioritize regulatory compliance, serialization tracking, and ESG certification. This shift has moved competition from cost-per-pallet metrics to audit-readiness and technology integration. International transportation management faces challenges like container equipment imbalances and geopolitical uncertainties, but providers with multimodal coordination capabilities can differentiate by optimizing real-time capacity and costs. Domestic transportation management, projected to hold a 49.34% of the Middle East third-party logistics market share in 2025, benefits from e-commerce growth and quick commerce demands, though driver shortages and fuel cost volatility are squeezing margins on fixed-price contracts.

In pharmaceutical logistics, GS1 serialization integration within VAWD operations ensures compliance while improving inventory visibility and stock rotation. GCC ports, positioned as transshipment hubs, support sea freight coordination, but container shortages limit capacity and increase spot-rate volatility. Air freight services, crucial for time-sensitive pharmaceutical and aerospace cargo, face bottlenecks due to regional airport capacity constraints. Road transportation in GCC markets benefits from better highway infrastructure and cross-border facilitation but struggles with rising costs from driver nationalization mandates and licensing restrictions.

List of Companies Covered in this Report:

- Al-Futtaim Logistics

- Almajdouie Logistics

- APL Logistics Ltd.

- Aramex

- BDP International

- CMA CGM Group (Including CEVA Logistics)

- Crane Worldwide Logistics

- DHL Group

- DSV A/S

- Emirates Logistics

- Gulf Agency Company (GAC)

- GWC (Gulf Warehousing Company)

- Kanoo Logistics

- Nippon Express Holdings

- NYK Line (Including Yusen Logistics)

- RAK Logistics

- Saudi Post

- TLM International Freight Services LLC

- Total Freight International

- Tristar Transport LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Turkey-GCC Cross-Border E-Commerce Accords Accelerating Small-Parcel Flows

- 4.2.2 Green Sukuk Financing Spurring Roll-Out of Solar-Powered, ESG-Certified Warehouses

- 4.2.3 Hydrogen Export Mega-Projects (NEOM, Oman) Generating Demand for Cryogenic Bulk-Gas Logistics

- 4.2.4 Mandatory GS1 Serialization in Saudi Pharma Supply Chain Expanding Compliance-Ready 3PL Contracts

- 4.2.5 Dark-Store Instant-Grocery Start-Ups Outsourcing Hyper-Local Fulfilment to 3PL Micro-Hubs

- 4.2.6 UAE Aerospace and Satellite-Assembly Clusters Driving Growth in Project-Cargo 3PL Services

- 4.3 Market Restraints

- 4.3.1 Persistent Container-Equipment Imbalance Inflating Repositioning Costs on GCC Lanes

- 4.3.2 Slow GCC VAT-Framework Harmonization Complicating Bonded Cross-Border Movements

- 4.3.3 Shortfall of Pharmaceutical-Grade Reefer Assets amid Rising Vaccine and Biologics Trade

- 4.3.4 Escalating Ransomware and Cyber-Intrusion Risks Increasing 3PL Insurance Premiums and Downtime

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technology Outlook (IoT, AI, Robotics, Hydrogen Trucks)

- 4.6 Regulatory Landscape and Government Initiatives

- 4.7 Insights into E-commerce Business

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Domestic Transportation Management

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Others

- 5.1.2 International Transportation Management

- 5.1.2.1 Road

- 5.1.2.2 Air

- 5.1.2.3 Sea

- 5.1.2.4 Multimodal / Intermodal

- 5.1.3 Value-Added Warehousing and Distribution (VAWD)

- 5.1.1 Domestic Transportation Management

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Energy and Utilities

- 5.2.3 Manufacturing

- 5.2.4 Life Sciences and Healthcare

- 5.2.5 Technology and Electronics

- 5.2.6 E-commerce

- 5.2.7 Consumer Goods and FMCG

- 5.2.8 Food and Beverages

- 5.2.9 Others

- 5.3 By Logistics Model

- 5.3.1 Asset-Light (Management-Based)

- 5.3.2 Asset-Heavy (Own Fleet and Warehouses)

- 5.3.3 Hybrid

- 5.4 By Country

- 5.4.1 United Arab Emirates

- 5.4.2 Saudi Arabia

- 5.4.3 Turkey

- 5.4.4 Egypt

- 5.4.5 Qatar

- 5.4.6 Bahrain

- 5.4.7 Kuwait

- 5.4.8 Oman

- 5.4.9 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Al-Futtaim Logistics

- 6.4.2 Almajdouie Logistics

- 6.4.3 APL Logistics Ltd.

- 6.4.4 Aramex

- 6.4.5 BDP International

- 6.4.6 CMA CGM Group (Including CEVA Logistics)

- 6.4.7 Crane Worldwide Logistics

- 6.4.8 DHL Group

- 6.4.9 DSV A/S

- 6.4.10 Emirates Logistics

- 6.4.11 Gulf Agency Company (GAC)

- 6.4.12 GWC (Gulf Warehousing Company)

- 6.4.13 Kanoo Logistics

- 6.4.14 Nippon Express Holdings

- 6.4.15 NYK Line (Including Yusen Logistics)

- 6.4.16 RAK Logistics

- 6.4.17 Saudi Post

- 6.4.18 TLM International Freight Services LLC

- 6.4.19 Total Freight International

- 6.4.20 Tristar Transport LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment