PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072691

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072691

Germany 3PL Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

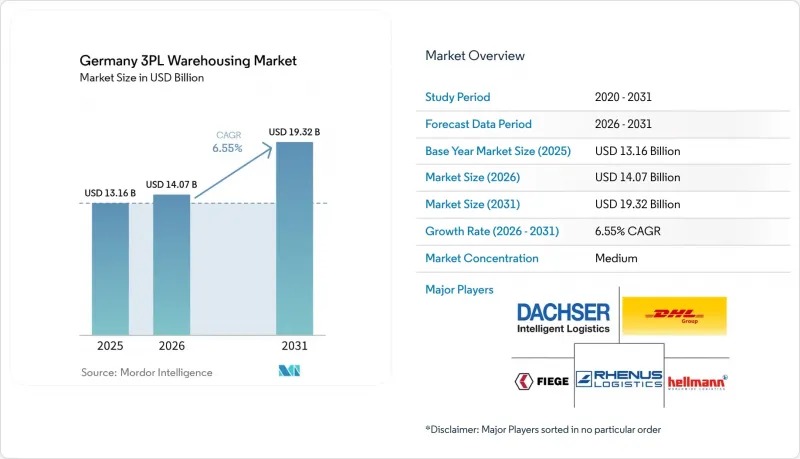

According to Mordor Intelligence, the germany 3PL warehousing market size was valued at USD 13.16 billion in 2025 and is projected to grow from USD 14.07 billion in 2026 to reach USD 19.32 billion by 2031, growing at a CAGR of 6.55% during 2026-2031.

The Germany 3PL warehousing market continues to benefit from the country's role as Europe's manufacturing and transit backbone, with borders to 9 countries and a central position across the Frankfurt, Hamburg, and Rhine-Ruhr logistics triangle, where supply remains tight and prime logistics space commands some of the continent's highest rents. This report is Segmented by Service Type (Storage, Distribution and Inventory Management, and Others), by Warehouse Type (General Shared/Multi-client, Bonded, and More), by Temperature Control (Non-Temperature Controlled, and More), by Technology (Manual, Semi-Automated, Fully Automated), and by End User (Manufacturing, Consumer Goods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany 3PL Warehousing Market Trends and Insights

E-Commerce Same-/Next-Day Fulfillment Pressure

The Germany 3PL warehousing market is seeing stronger fulfillment pressure because online retail demand now depends as much on delivery speed and returns handling as on basic storage. Germany's online retail market generated EUR 80.6 billion (USD 87.0 billion) in 2024 and served 68 million online shoppers, with average annual spend reaching EUR 2,200 (USD 2,376) per shopper. Next-day delivery has become the normal service expectation in categories such as apparel, electronics, and beauty, and same-day service is moving from a premium option to a competitive differentiator in dense urban areas. Returns matter just as much as outbound speed because Germany continues to record very high fashion return rates, which means reverse logistics capacity is now a core warehouse function rather than an optional add-on. This is pushing operators toward sites near major population centers even when rents are high and new land is scarce. As urban greenfield options tighten, large brownfield retrofits and edge-of-city nodes are becoming a more practical route for operators that still need scale and fast cut-off windows.

Pharmaceutical Biologics Cold-Chain Boom

The Germany 3PL warehousing market is getting a strong lift from pharmaceutical logistics because biologics, biosimilars, and specialty therapies need stricter storage control than conventional products. DHL Group opened Florstadt 4 in May 2025 as a 30,000 sqm multi-temperature warehouse, which expanded the Florstadt health logistics campus to 100,000 sqm and more than 140,000 pallet positions. The rise of temperature-sensitive products is changing procurement behavior because GDP and GMP compliance now play a direct role in contract awards and renewals. This shift is also raising the value of digitally auditable, multi-temperature, and certified facilities, since biopharma clients want fewer weak points across storage, handling, and release processes. Vetter Pharma's EUR 150 million (USD 163.5 million) expansion in Ravensburg, which adds 16,000 pallet positions and targets 68,000 positions by 2028, also points to rising demand for outsourced overflow, buffer storage, and support capacity around manufacturer-owned sites. The result is that cold-chain warehousing is no longer a niche within the Germany 3PL warehousing market, but a faster-growing layer that increasingly shapes network planning.

Scarcity and Cost of Prime Industrial Land in Hub Cities

The Germany 3PL warehousing market faces a structural land problem because the tightest logistics corridors are also the ones where demand is strongest. Prime logistics rents in 2025 reached EUR 11.0 per sqm per month (USD 12.0) in Munich, EUR 8.7 (USD 9.5) in Frankfurt, and EUR 8.5 (USD 9.3) in Stuttgart, which confirms that core hubs remain supply-constrained. The long-run space gap is becoming more difficult to close because land-use policy is tightening at both German and EU levels. Brownfield redevelopment offers one route forward, but it brings contamination risk, fragmented ownership, and longer remediation periods, which slow project delivery. This issue is most severe for mid-sized operators that cannot pre-emptively acquire land or finance more complex formats. Over time, land scarcity is likely to keep the Germany 3PL warehousing market tilted toward larger providers with stronger balance sheets and deeper developer relationships.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring of Automotive Tier-1 Suppliers

- Automation ROI Rise Amid Labor Shortages

- Rising Electricity Prices for Temperature-Controlled Sites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage services held 48.11% of the Germany 3PL warehousing market share in 2025, which reflects the continued need for inventory buffering across automotive, retail, and consumer goods supply chains. Distribution and inventory management remain essential because they connect warehouse capacity with pick-pack execution, transport planning, and stock visibility across national networks. Value-added services and others are projected to expand at a 9.38% CAGR through 2031, well above the overall rate and indicating that contract scope is moving beyond basic space provision. This part of the Germany 3PL warehousing market is growing because clients want late-stage customization without taking on their own site, labor, and systems costs. Kitting, labeling, returns processing, and co-packing now sit closer to the center of warehouse economics than they did a few years ago.

That shift is being driven by two pressures at once. E-commerce orders need more unit-level handling, tailored packaging, and faster returns workflows, while healthcare products need tighter documentation and more controlled handling procedures. Germany's packaging and producer responsibility rules also make compliant labeling and preparation services more valuable for customers that want a single outsourced workflow. This is where reputable operators can build better margins, since certified and process-heavy work is harder to replace than standard storage. The Germany 3PL warehousing industry is therefore moving toward contracts where labor content, systems integration, and compliance execution all matter more. Operators with proven capability in consumer electronics and healthcare are better placed to capture this premium layer of demand.

General shared and multi-client warehousing accounted for 54.83% of the German 3PL warehousing market size in 2025, underscoring how strongly shippers still value capital efficiency and national reach. Multi-client buildings remain attractive because they allow 3PL providers to spread fixed costs across multiple customers and varying seasonal demand patterns. This model is especially useful in e-commerce and FMCG, where peak patterns move quickly and overflow flexibility matters. FIEGE's 55,000 sqm Hamminkeln project and 52,000 sqm Hessisch Lichtenau project, both targeted for autumn 2026, show that multi-user capacity is still being added in carefully selected nodes. For many occupiers, shared warehousing remains the most practical route into the Germany 3PL warehousing market.

Dedicated contract warehousing remains the fastest-growing warehouse type, with a 8.55% CAGR through 2031, as some customers cannot operate in shared environments. Pharmaceutical, automotive, sequencing, and hazardous-goods users need stronger process control, contamination separation, or security arrangements than a general multi-client site can provide. That requirement increases the value of purpose-built facilities and longer contract terms. It also raises entry barriers because validation, engineering design, and customer approval become more demanding. Bonded warehousing remains smaller, but it is becoming more relevant for non-EU flows entering Germany's port system as customs documentation and clearance requirements tighten. This leaves the Germany 3PL warehousing market with a dual structure where shared space leads on volume and dedicated space leads on compliance-driven growth.

Complete Report Scope:

- By Service Type

- Storage

- Distribution and Inventory Management

- Value-Added Services and Others (Kitting, Labelling)

- By Warehouse Type

- General Shared / Multi-client Warehousing

- Dedicated Contract Warehousing

- Bonded Warehousing

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Technology Adoption

- Manual

- Semi-automated

- Fully Automated

- By End User Industry

- Manufacturing

- Consumer Goods

- Food and Beverage

- Retail and E-commerce

- Healthcare and Pharma

- Other End-user Industries

List of Companies Covered in this Report:

- DHL Group

- DACHSER

- Rhenus Logistics

- FIEGE Logistics

- Hellmann Worldwide Logistics

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- GEODIS

- CMA CGM Group (Including CEVA Logistics)

- BLG Logistics

- Nagel-Group

- Arvato Supply Chain Solutions

- LGI Logistics Group International

- Nippon Express

- NYK Line (Including Yusen Logistics)

- A.P. Moller - Maersk

- FedEx

- ID Logistics

- Rudolph Logistics Group

- Honold Logistik Gruppe

- Imperial Logistics

- Schnellecke Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Same-/Next-Day Fulfilment Pressure

- 4.2.2 Pharmaceutical Biologics Cold-Chain Boom

- 4.2.3 Near-Shoring of Automotive Tier-1 Suppliers

- 4.2.4 Automation ROI Rise Amid Labor Shortages

- 4.2.5 Rapid Adoption of Carbon-Neutral Warehouse Standards

- 4.2.6 Digital Marketplace Platforms for On-Demand Space

- 4.3 Market Restraints

- 4.3.1 Scarcity and Cost of Prime Industrial Land in Hub Cities

- 4.3.2 Rising Electricity Prices for Temperature-Controlled Sites

- 4.3.3 Strict GDP / GMP Audits Delaying Pharma Warehouse Onboarding

- 4.3.4 Fragmented SME 3PL Base Slowing Uniform Tech Adoption

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Evolution of Cold-Chain Warehousing Requirements

- 4.9 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-Added Services and Others (Kitting, Labelling)

- 5.2 By Warehouse Type

- 5.2.1 General Shared / Multi-client Warehousing

- 5.2.2 Dedicated Contract Warehousing

- 5.2.3 Bonded Warehousing

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Technology Adoption

- 5.4.1 Manual

- 5.4.2 Semi-automated

- 5.4.3 Fully Automated

- 5.5 By End User Industry

- 5.5.1 Manufacturing

- 5.5.2 Consumer Goods

- 5.5.3 Food and Beverage

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Pharma

- 5.5.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 DACHSER

- 6.4.3 Rhenus Logistics

- 6.4.4 FIEGE Logistics

- 6.4.5 Hellmann Worldwide Logistics

- 6.4.6 Kuehne+Nagel

- 6.4.7 DSV A/S (Including DB Schenker)

- 6.4.8 GEODIS

- 6.4.9 CMA CGM Group (Including CEVA Logistics)

- 6.4.10 BLG Logistics

- 6.4.11 Nagel-Group

- 6.4.12 Arvato Supply Chain Solutions

- 6.4.13 LGI Logistics Group International

- 6.4.14 Nippon Express

- 6.4.15 NYK Line (Including Yusen Logistics)

- 6.4.16 A.P. Moller - Maersk

- 6.4.17 FedEx

- 6.4.18 ID Logistics

- 6.4.19 Rudolph Logistics Group

- 6.4.20 Honold Logistik Gruppe

- 6.4.21 Imperial Logistics

- 6.4.22 Schnellecke Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment