PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072899

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072899

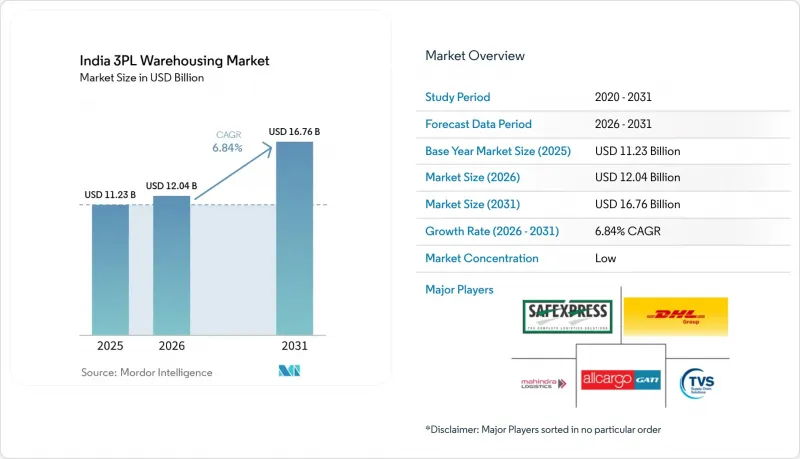

India 3PL Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india 3PL warehousing market size is expected to increase from USD 11.23 billion in 2025 to USD 12.04 billion in 2026 and reach USD 16.76 billion by 2031, growing at a CAGR of 6.84% over 2026-2031.

India's 3PL warehousing market is performing well, driven by rising outsourcing, e-commerce growth, manufacturing expansion, and the shift toward organized supply chains. This report is Segmented by Service Type (Storage, Distribution and More), by Warehouse Type (General Shared, Bonded, and More), by Temperature Control (Non-Temperature, Temperature), by Technology Adoption (Manual, Semi-Automated, and More), by End User Industry (Manufacturing, Consumer Goods, and More), and by Region (North, Central, and More). The Market Forecasts are Provided in Terms of Value (USD).

India 3PL Warehousing Market Trends and Insights

Rapid Growth of E-Commerce Fulfillment

The India 3PL warehousing market is seeing a sharper shift toward fulfillment-led demand rather than simple capacity booking. E-commerce operators are expanding dark-store and replenishment networks because speed now matters as much as inventory depth in major cities. Flipkart Minutes targeted 1,000 dark stores by April 2026, up from more than 500 in late 2025, underscoring how quickly urban replenishment networks are scaling. India had 2,525 operational dark stores as of October 2025, and this base is projected to reach 7,500 by 2030, keeping demand high for intra-city mother hubs, local storage points, and rapid-picking formats. This pattern is forcing 3PL operators to redesign legacy hub-and-spoke models around denser urban layouts, smaller footprints, and faster inventory turns.

Infrastructure Push

The India 3PL warehousing market is also benefiting from transport upgrades that reduce movement time and support larger, more efficient warehouse networks. The Eastern and Western dedicated freight corridors were 96.4% operational by March 2025, covering 2,741 route km and cutting Delhi-Mumbai freight transit time by close to 40%, while wagon turnaround dropped from 15-16 days to 2-3 days. Indian Railways had also commissioned 118 Gati Shakti Multimodal Cargo Terminals across 18 states by October 2025, which widened the map for rail-linked warehousing demand. The opening of the PM GatiShakti portal to private users also improves site planning by enabling operators to assess corridor access, utility links, and land suitability through a common data layer. Better corridor visibility and lower transit variability are making bigger multi-client and factory-linked locations more viable across the India 3PL warehousing market.

Land Acquisition and Zoning Bottlenecks

Land access remains a direct growth constraint for the India 3PL warehousing market, especially where demand is shifting closer to city limits and industrial corridors. The Warehousing Association of India stated in July 2025 that setting up a warehouse still needed close to 60 state and central permissions, which slows development and raises execution risk. Urban zoning rules add another layer because several cities restrict warehouse and cold-storage use in residential zones. At the same time, many states require wider access roads and minimum plot sizes that are hard to secure in dense neighborhoods. These frictions are particularly difficult for quick-commerce and small-format operators because they need sites close to consumers rather than far from the urban core. They also favor well-capitalized operators that can manage approvals, buy better land parcels, and wait longer for project completion.

Other drivers and restraints analyzed in the detailed report include:

- PLI Schemes Triggering Near-Factory Logistics Hubs

- Rise of Dark Stores and Quick-Commerce Micro-Warehousing

- Fragmented Cold-Chain Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage accounted for 59.07% of the India 3PL warehousing market share in 2025, indicating that basic space-and-handle outsourcing still accounts for the largest share of current demand. Distribution and inventory management remained the second-largest service line because e-commerce, consumer goods, and retail clients increasingly need stock rotation, order handling, and returns support within a single operating network. Value-added services are the fastest-growing sub-segment, with a 9.67% CAGR through 2031, confirming that the India 3PL warehousing industry is moving beyond static storage toward integrated fulfillment. This shift is strongest where clients want kitting, labeling, secondary packaging, and documentation support within the warehouse, rather than managing those steps internally. The service mix is changing because clients want fewer handoffs and greater visibility across a single operating platform.

The growth of value-added work also reflects a higher quality threshold in the India 3PL warehousing market. Food and pharma customers need tighter record keeping, batch control, FIFO or FEFO discipline, and stronger process compliance, which makes specialist outsourcing more useful. Operators that invest in better warehouse management systems and traceability tools are better positioned to capture these contracts, as clients prefer connected data and cleaner execution. The result is that service depth is becoming a clearer differentiator than floor space alone, especially in shared facilities serving multiple categories.

General shared/multi-client warehousing held 55% of the India 3PL warehousing market share in 2025, reflecting the continued preference for flexible, asset-light warehousing among shippers. This format works well for seasonal demand, early-stage D2C brands, and mid-sized manufacturers that do not want to commit to long leases or dedicated capacity. Dedicated contract warehousing remains important for anchor clients that need plant-adjacent facilities, custom layouts, and protected throughput. Bonded warehousing is the fastest-growing format, with a 8.85% CAGR through 2031, because export-oriented manufacturing and multi-country sourcing require duty-deferred storage and tighter customs-linked controls. That makes bonded space more strategic than its current scale might suggest.

The strength of this segment comes from a different demand logic inside the India 3PL warehousing market. PLI-linked electronics, semiconductor, and industrial supply chains need inbound component management before production starts, and that supports bonded facilities near ports and industrial corridors. TVS Supply Chain Solutions opened a 40,000 ft2 FTWZ facility near Chennai in March 2026 to support Caterpillar's global supply chains from India, underscoring the growing prominence of bonded warehousing in industrial logistics. Nippon Express also discussed a semiconductor logistics hub in Dholera in January 2026, with plans for specialized bonded warehousing for semiconductor materials. These moves suggest that bonded infrastructure is becoming a long-term enabler of export-linked growth rather than a niche customs service.

Complete Report Scope:

- By Service Type

- Storage

- Distribution and Inventory Management

- Value-Added Services and Others (Kitting, Labelling)

- By Warehouse Type

- General Shared / Multi-client Warehousing

- Dedicated Contract Warehousing

- Bonded Warehousing

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Technology Adoption

- Manual

- Semi-automated

- Fully Automated

- By End User Industry

- Manufacturing

- Consumer Goods

- Food and Beverage

- Retail and E-commerce

- Healthcare and Pharma

- Other End-user Industries

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- DHL Supply Chain

- Mahindra Logistics Ltd.

- TVS Supply Chain Solutions

- Allcargo Supply Chain Pvt. Ltd. (Gati-Allcargo ecosystem)

- Safexpress Pvt. Ltd.

- Delhivery Ltd.

- Blue Dart Express Ltd.

- Transport Corporation of India (TCI Supply Chain Solutions)

- CJ Darcl Logistics Ltd.

- DP World Logistics India

- Yusen Logistics India Pvt. Ltd.

- FedEx Supply Chain India

- Kuehne+Nagel India

- DSV (incl. Schenker integration)

- Nippon Express India

- Prozo Integrated Supply Chain Solutions

- Shiprocket Fulfillment

- Xpressbees Logistics

- Shadowfax Technologies

- Om Logistics Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth of E-Commerce Fulfilment

- 4.2.2 Infrastructure Push (Gati Shakti, Bharatmala)

- 4.2.3 GST-Driven Network Consolidation

- 4.2.4 Organized Retail's Demand for Grade-A Space

- 4.2.5 Rise of Dark Stores and Quick-Commerce Micro-Warehousing

- 4.2.6 PLI Schemes Triggering Near-Factory Logistics Hubs

- 4.3 Market Restraints

- 4.3.1 Land Acquisition and Zoning Bottlenecks

- 4.3.2 Weak First/Last-Mile Multimodal Links

- 4.3.3 Fragmented Cold-Chain Compliance

- 4.3.4 High Power Tariffs Denting Automation ROI

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Evolution of Cold-Chain Warehousing Requirements

- 4.9 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-Added Services and Others (Kitting, Labelling)

- 5.2 By Warehouse Type

- 5.2.1 General Shared / Multi-client Warehousing

- 5.2.2 Dedicated Contract Warehousing

- 5.2.3 Bonded Warehousing

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Technology Adoption

- 5.4.1 Manual

- 5.4.2 Semi-automated

- 5.4.3 Fully Automated

- 5.5 By End User Industry

- 5.5.1 Manufacturing

- 5.5.2 Consumer Goods

- 5.5.3 Food and Beverage

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Pharma

- 5.5.6 Other End-user Industries

- 5.6 By Region

- 5.6.1 North

- 5.6.2 Central

- 5.6.3 West

- 5.6.4 East

- 5.6.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain

- 6.4.2 Mahindra Logistics Ltd.

- 6.4.3 TVS Supply Chain Solutions

- 6.4.4 Allcargo Supply Chain Pvt. Ltd. (Gati-Allcargo ecosystem)

- 6.4.5 Safexpress Pvt. Ltd.

- 6.4.6 Delhivery Ltd.

- 6.4.7 Blue Dart Express Ltd.

- 6.4.8 Transport Corporation of India (TCI Supply Chain Solutions)

- 6.4.9 CJ Darcl Logistics Ltd.

- 6.4.10 DP World Logistics India

- 6.4.11 Yusen Logistics India Pvt. Ltd.

- 6.4.12 FedEx Supply Chain India

- 6.4.13 Kuehne+Nagel India

- 6.4.14 DSV (incl. Schenker integration)

- 6.4.15 Nippon Express India

- 6.4.16 Prozo Integrated Supply Chain Solutions

- 6.4.17 Shiprocket Fulfillment

- 6.4.18 Xpressbees Logistics

- 6.4.19 Shadowfax Technologies

- 6.4.20 Om Logistics Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment