PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063546

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063546

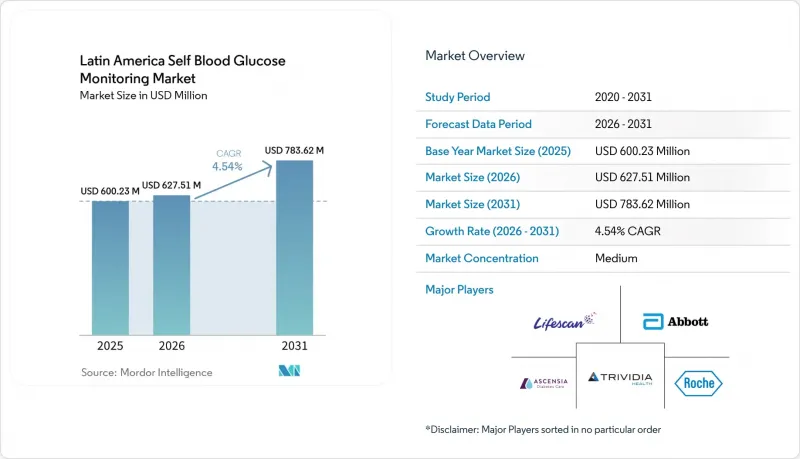

Latin America Self Blood Glucose Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the latin america self blood glucose monitoring market size was valued at USD 600.23 million in 2025 and is estimated to grow from USD 627.51 million in 2026 to reach USD 783.62 million by 2031, at a CAGR of 4.54% during the forecast period (2026-2031).

This report is Segmented by Component (Glucometer Devices and More), Patient Type (Type-1 Diabetes and More), Distribution Channel (B2B and More), End-User (Homecare Settings and More), and Geography (Mexico and More). The Market Forecasts are Provided in Terms of Value (USD).

Latin America Self Blood Glucose Monitoring Market Trends and Insights

Rising Diabetes Prevalence and Undiagnosed Burden in Latin America

The rising burden of diabetes in Latin America increases routine glucose self-testing for newly identified cases and for patients intensifying therapy. Mexico exemplifies the challenge with a high adult prevalence profile, which sustains frequent monitoring across urban corridors with dense pharmacy networks. Health systems are pushing more opportunistic screening through primary care and workplace settings, which channels newly diagnosed patients into the Latin America self blood glucose monitoring market as a first step in self-management. Earlier case detection links meter adoption to behavioral coaching and diet adjustment, which stabilizes baseline strip use before any transition to advanced therapies. Primary care teams emphasize capillary testing for non-insulin patients to support medication titration and to flag complications sooner. These shifts lift recurring strip throughput as more adults formalize daily or weekly testing routines aligned to local clinical guidance.

Public Provision and Reimbursement of SMBG Supplies

Public-sector programs across the region reinforce self-monitoring by bundling meters and strips into chronic disease pathways for prioritized cohorts. City and provincial programs register eligible users and embed SMBG refills within scheduled follow-ups, which reduces missed pickups and keeps adherence steady over time. Social security and retiree plans strengthen access for older patients who require more frequent checks due to multi-morbidity and insulin use. Where public formularies exclude meters or limit strip allotments, retail purchases and employer support fill the gap. This patchwork still benefits the Latin America Self Blood Glucose Monitoring Market because multiple access routes stabilize monthly volumes as patients combine public supplies with retail top-ups. In dense urban areas, this mix of routes maintains predictable flow through pharmacy chains and distribution centers.

Accelerating CGM Adoption Among Insulin Users Reducing Fingerstick Frequency

Continuous and flash glucose sensors gain traction among insulin users in private channels, which reduces routine fingerstick frequency for patients who achieve stable wear and scanning habits. As more endocrinology clinics adopt CGM-first protocols for poor control, the highest-frequency strip users transition to sensors for daily trend visibility. This substitution affects the Latin America Self Blood Glucose Monitoring Market most in affluent metro areas where private coverage or out-of-pocket capacity is stronger. For non-insulin Type 2 cohorts, SMBG remains standard for dose titration and lifestyle management, which sustains a large base of recurring strip demand. Many clinics still recommend periodic capillary checks for CGM users to confirm readings during dose changes or when sensors signal instability, which preserves some strip volume in hybrid workflows. The net effect is a rebalancing of strip consumption away from intensive insulin users toward broader non-insulin populations and onboarding cohorts.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Home-Based Diabetes Self-Management and Digital Enablement

- Expansion of Retail and E-Pharmacy Fulfillment is Improving SMBG Access

- Import Dependence, FX Volatility, and Price Caps Pressure SMBG Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Test strips captured 82.95% of 2025 revenue and are projected to grow at a 5.21% CAGR, reflecting the dominant role of consumables in the Latin America Self Blood Glucose Monitoring Market. Test strips accounted for a large share of the Latin America self blood glucose monitoring market size in 2025, while meter hardware saw thinner unit margins as placement strategies emphasized recurring strip pull-through. Subsidized or low-margin meter placements remain common to accelerate onboarding, while strip repurchases extend over long cycles due to brand and ecosystem lock-in. That lock-in strengthens because many patients prefer compatible meters and strips that match coaching materials and clinic protocols. Features that reduce waste, such as second-chance sampling and guided fill indicators, also help stretch budgets and improve perceived value for public programs and families. As more users track daily or weekly readings at home, predictable strip replacement drives steady cash-register throughput in both retail and e-pharmacy channels.

Lancets retain a smaller revenue role compared with strips but remain high in unit volumes because of single-use hygiene protocols and patient safety rules. Vendors often bundle lancets with new meters or starter kits, which simplifies initial use for newly diagnosed patients. Procurement specifications in public schemes continue to emphasize quality control for consumables, which favors established brands with strong post-market surveillance records. In urban markets where onboarding is frequent, pharmacy teams help align meter choice, lancet gauge, and strip compatibility during counseling. That support reduces returns caused by setup errors and inconsistent sampling techniques and sustains positive user experience. Taken together, strips anchor recurring revenue, hardware sustains brand placement, and lancets complete the routine at-home testing kit in the Latin America self blood glucose monitoring market.

Type 2 diabetes represented 88.35% of the patient mix in 2025, which sets the baseline for meter placements and monthly strip consumption across the Latin America self blood glucose monitoring market. Type 2 diabetes accounted for 88.35% of the Latin America self blood glucose monitoring market share in 2025, and physicians often recommend routine SMBG during dietary changes, oral medication titration, and comorbidity management. That pattern distributes testing intensity across millions of non-insulin patients rather than concentrating volume only in insulin users. As mobile apps and connected meters become more common, many Type 2 users adopt weekly patterns that balance test frequency with coaching feedback. Clinics reinforce SMBG to flag destabilization early, which supports treatment adherence and reduces avoidable acute care. These habits underpin stable strip replacement rates across large urban centers.

Gestational diabetes is projected to grow at a 7.46% CAGR through 2031, making it the fastest-growing patient segment in the Latin America self blood glucose monitoring market. Prenatal care teams are formalizing fasting and postprandial capillary checks to manage maternal and neonatal outcomes, which expands meter and strip allocations for this cohort. Structured prenatal pathways also build SMBG familiarity that can sustain continued monitoring for women at risk of Type 2 progression after delivery. Public clinics and retail pharmacies help with onboarding by demonstrating lancing techniques and meter setup during prenatal visits and purchase encounters. The combination of expanding prenatal guidelines and patient education underpins the segment's strong growth outlook.

List of Companies Covered in this Report:

- Abbott Laboratories

- Acon Laboratories Inc

- AgaMatrix Inc/i-Sens

- ARKRAY, Inc

- Ascensia

- Beurer

- Bionime

- Embecta Corp. (Owen Mumford)

- Roche

- LifeScan IP Holdings, LLC

- Nova Biomedical

- Rossmax

- Taidoc Technology Corp.

- Terumo

- Trividia Health, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diabetes Prevalence and Undiagnosed Burden in Latin America

- 4.2.2 Public Provision and Reimbursement of SMBG Supplies

- 4.2.3 Shift to Home-Based Diabetes Self-Management and Digital Enablement

- 4.2.4 Expansion of Retail and E-Pharmacy Fulfillment is Improving SMBG Access

- 4.2.5 Meter-Strip Brand Lock-In, Sustaining Recurring Strip Volumes

- 4.2.6 Omnichannel Pharmacy Programs Boosting Adherence

- 4.3 Market Restraints

- 4.3.1 Accelerating CGM Adoption Among Insulin Users Reducing Fingerstick Frequency

- 4.3.2 Import Dependence, FX Volatility, and Price Caps Pressure SMBG Margins

- 4.3.3 Regulatory Suspensions/Quality Interdictions Disrupting Public Tenders

- 4.3.4 Counterfeit/Substandard Strips on Informal Channels Erode Trust

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Indicators

- 5.1 Type-1 Diabetes Population

- 5.2 Type-2 Diabetes Population

6 Market Size & Growth Forecasts (Value)

- 6.1 By Component

- 6.1.1 Glucometer Devices

- 6.1.2 Test Strips

- 6.1.3 Lancets

- 6.2 By Patient Type

- 6.2.1 Type-1 Diabetes

- 6.2.2 Type-2 Diabetes

- 6.2.3 Gestational Diabetes & Others

- 6.3 By Distribution Channel

- 6.3.1 B2B

- 6.3.2 Retail Pharmacies

- 6.3.3 Online Pharmacies

- 6.3.4 Other Channels

- 6.4 By End-User

- 6.4.1 Homecare Settings

- 6.4.2 Hospitals

- 6.4.3 Clinics & Diagnostic Centers

- 6.5 By Country

- 6.5.1 Mexico

- 6.5.2 Brazil

- 6.5.3 Argentina

- 6.5.4 Rest of Latin America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Market Share Analysis

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Key Products, and Recent Developments)

- 7.3.1 Abbott Laboratories

- 7.3.2 Acon Laboratories Inc

- 7.3.3 AgaMatrix Inc/i-Sens

- 7.3.4 ARKRAY, Inc

- 7.3.5 Ascensia Diabetes Care

- 7.3.6 Beurer GmbH

- 7.3.7 Bionime Corporation

- 7.3.8 Embecta Corp. (Owen Mumford)

- 7.3.9 F. Hoffmann-La Roche AG

- 7.3.10 LifeScan IP Holdings, LLC

- 7.3.11 Nova Biomedical

- 7.3.12 Rossmax International Ltd

- 7.3.13 Taidoc Technology Corp.

- 7.3.14 Terumo Corporation

- 7.3.15 Trividia Health, Inc.

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment