PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063671

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063671

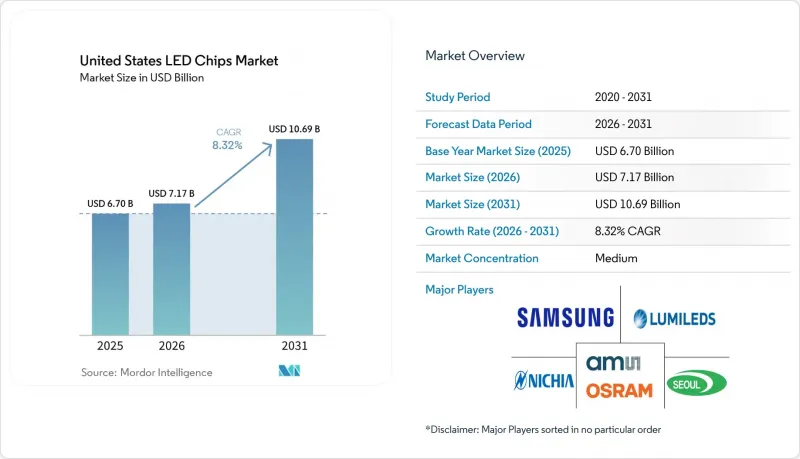

United States LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states lED chips market size was valued at USD 6.70 billion in 2025 and estimated to grow from USD 7.17 billion in 2026 to reach USD 10.69 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and More), Semiconductor Material (GaN/InGaN, Algainp, and More), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States LED Chips Market Trends and Insights

Escalating Adoption of Mini-LED Backlighting in High-End TVs

Sales momentum accelerated after the 2026 Consumer Electronics Show showcased mainstream 55-inch to 130-inch televisions equipped with thousands of red, green, and blue mini-LED emitters rather than white LEDs with color filters. Unit shipments for mini-LED TVs surpassed 20 million in 2026, lifting chip density requirements and pressuring domestic suppliers to tighten binning to sub-2-nanometer wavelength windows. Cost reductions of 20-30% logged during 2025 moved the technology from flagship to mid-tier models, widening the total addressable market for GaN emitters with forward-voltage spreads below 0.1 volts. In the United States LED chip market, the cumulative effect is a multi-year uplift, as television, monitor, and gaming hardware brands require higher volumes of tight-pitch chips. RGB mini-LED configurations eliminate quantum-dot layers in several designs, thereby capturing more of the system's value into the chip bill of materials. Domestic fabs that can guarantee high luminous-flux uniformity across wafer lots are therefore well positioned to win new display contracts.

Federal and State Energy Efficiency Incentives for Solid-State Lighting

Rebate programs covered a significant share of the United States' commercial floor space in 2026, and average prescriptive incentives rose across outdoor categories. Section 179D deductions deliver up to USD 5.36 per square foot, effectively shaving payback periods to below two years for high-efficacy luminaire retrofits in warehouses and cold-storage facilities. Utilities are migrating from flat-per-unit rebates to energy-savings performance models, favoring LED chips that help fixtures exceed 130 lumens per watt and qualify for DesignLights Consortium Premium listings. Oregon's 2025 fluorescent-lamp ban, followed by Hawaii's 2026 ban, further compresses legacy-lamp incentives and channels funding toward LED-to-LED upgrades with networked controls. These measures ensure that the United States LED chip market continues to absorb high volumes for troffer, outdoor, and high-bay fixtures over the next 24 months.

Supply Chain Bottlenecks in Silicon Carbide Substrates

Silicon-carbide crystal growth remains energy intensive, and the move to 200 mm wafers confronts yield losses that erode effective capacity. Competition from power-device makers siphons wafer allocations, as electric-vehicle inverters command higher margins than LED epitaxy. Import restrictions on specialty gases and seed crystals, together with regional industrial-policy frictions, add volatility to lead times for AEC-Q101-qualified parts. U.S. chipmakers hedge risk through multi-year wafer offtake agreements and co-development projects aimed at improving crystalline quality, yet smaller entrants lack negotiating leverage and face allocation rationing. Resulting supply tension trims growth potential for high-reliability automotive and industrial LEDs within the United States LED chips market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Decline in Per-Lumen Cost of High-Power GaN Chips

- Automotive OEM Pivot Toward Exterior LED Pixel Lighting

- High Capital Expenditure for Micro-LED Mass Transfer Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional emitters retained 83.45% of the United States LED chip market share in 2025, reflecting dominance in troffers, streetlights, and retrofit lamps. In parallel, mini-LED and micro-LED architectures expanded at an 11.28% CAGR, unlocking premium price points in television backlighting, adaptive headlights, and near-eye AR microdisplays. Vertical GaN is emerging as a bridge technology, doubling current handling per die, enabling fixture downsizing, and enhancing thermal performance in high-power modules.

The influx of RGB mini-LED backlights, each television integrating up to 30,000 dies, markedly boosts chip dollar-content even as per-lumen prices fall, effectively counterbalancing commoditization in general lighting. For micro-LEDs, mass-transfer hurdles remain, but pilot programs in defense avionics and premium wearables are validating reliability metrics. Domestic suppliers that combine wafer-level binning with proprietary quantum-dot-free color conversion are positioned to capture early design wins. Collectively, the coexistence of high-volume conventional LEDs and fast-growing micro-LED nodes diversifies revenue streams and insulates the United States LED chips market against single-segment cyclicality.

List of Companies Covered in this Report:

- ams-OSRAM AG

- Lumileds Holding B.V.

- Nichia Corporation

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Coherent Corp.

- San'an Optoelectronics Co., Ltd.

- ON Semiconductor Corporation

- Everlight Electronics Co., Ltd.

- Ennostar Inc.

- Brightek Optoelectronic Co., Ltd.

- Genesis Photonics Inc.

- Cree LED, an SGH Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Adoption of Mini-LED Backlighting in High-End TVs

- 4.2.2 Federal and State Energy Efficiency Incentives for Solid-State Lighting

- 4.2.3 Rapid Decline in Per-Lumen Cost of High-Power GaN Chips

- 4.2.4 Automotive OEM Pivot Toward Exterior LED Pixel Lighting

- 4.2.5 Growing Demand for UV-C LED Chips in Disinfection Systems

- 4.2.6 Emergence of Smart Farming Requiring Horticultural LED Arrays

- 4.3 Market Restraints

- 4.3.1 Supply Chain Bottlenecks in Silicon Carbide Substrates

- 4.3.2 High Capital Expenditure for Micro-LED Mass Transfer Equipment

- 4.3.3 Intellectual Property Litigation Risk Among Chipmakers

- 4.3.4 Thermal Management Challenges Limiting Chip Miniaturization

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams-OSRAM AG

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Nichia Corporation

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Epistar Corporation

- 6.4.8 Coherent Corp.

- 6.4.9 San'an Optoelectronics Co., Ltd.

- 6.4.10 ON Semiconductor Corporation

- 6.4.11 Everlight Electronics Co., Ltd.

- 6.4.12 Ennostar Inc.

- 6.4.13 Brightek Optoelectronic Co., Ltd.

- 6.4.14 Genesis Photonics Inc.

- 6.4.15 Cree LED, an SGH Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment