PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065498

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065498

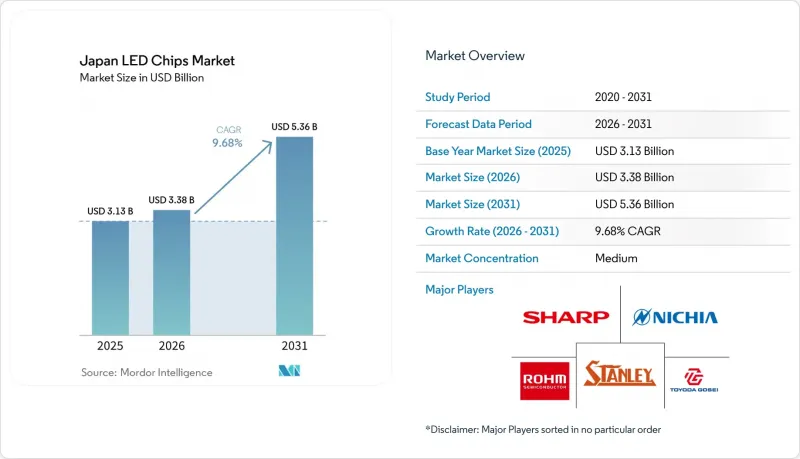

Japan LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan lED chips market size is expected to increase from USD 3.13 billion in 2025 to USD 3.38 billion in 2026 and reach USD 5.36 billion by 2031, growing at a CAGR of 9.68% over 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, Algainp, and Other Semiconductor Materials), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting). The Market Forecasts are Provided in Terms of Value (USD).

Japan LED Chips Market Trends and Insights

Government Incentives for Domestic Semiconductor Production

Japan allocated JPY 1.85 trillion (USD 12.6 billion) in 2023 subsidies for fabs that cover logic, memory, and photonics devices. Support for TSMC's second Kumamoto plant and Rapidus's 2-nanometer pilot line finances clean-room infrastructure now shared by compound-semiconductor projects, including LED epitaxy. Workforce training programs in Kyushu and Hokkaido further reinforce the local talent pool, easing recruitment challenges for LED foundries.

Surge in Electric-Vehicle Headlamp Integration

Koito reported that LEDs already represent 82% of its headlamp output and targets 100% by 2030.Adaptive driving beam modules need as many as 16,000 individually addressed emitters, lifting per-vehicle chip counts by two orders of magnitude versus halogen. Nichia and Infineon unveiled a micro-matrix light engine featuring 16,384 emitters that lowers power draw by about 18% compared with preceding solutions, a critical benefit for battery-electric range preservation.

High Capital Expenditure for Micro-LED Mass Transfer

Tool sets that approach 99.99% placement yield remain expensive. Hamamatsu Photonics invested JPY 37 billion (USD 250 million) in 2025 to bring 8-inch wafer processing online, yet the line can still lose profitability if downstream transfer tools underperform.Smaller firms often opt to license chip architectures rather than bankroll full Micro-LED back-ends.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations Favoring LED Retrofits

- Rising Adoption of Mini-LED Backlit TVs

- Supply Chain Disruptions for Gallium and Indium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs represented about 82.5% of the Japanese LED chips market share in 2025, anchored by depreciated legacy lines that still deliver competitive lumens-per-dollar for municipal retrofits. Mini-LED bridges performance and cost, giving premium TV brands high local-dimming ratios without OLED expense. The Japan LED chips market size tied to Micro-LED is forecast to expand at a near 14% CAGR because automotive adaptive driving beams and emerging augmented-reality displays require pixel densities that legacy chips cannot achieve.

Nichia's DominoPLS modules introduced in 2026 cut matrix-lamp cost by integrating micro-arrays onto a common ceramic substrate, simplifying assembly for compact vehicles. Red emitter efficiency below 3 µm remains difficult, but suppliers collaborate with material labs to boost external quantum efficiency beyond 5%, a threshold needed for full-color wearables.

List of Companies Covered in this Report:

- Nichia Corporation

- Toyoda Gosei Co., Ltd.

- Rohm Co., Ltd.

- Stanley Electric Co., Ltd.

- Sharp Corporation

- Sony Semiconductor Solutions Corporation

- Seoul Semiconductor Co., Ltd.

- Osram Opto Semiconductors GmbH

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lumileds Holding B.V.

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Kingbright Electronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mini-LED Backlit TVs

- 4.2.2 Government Incentives for Domestic Semiconductor Production

- 4.2.3 Surge in Electric Vehicle Headlamp Integration

- 4.2.4 Energy-Efficiency Regulations Favoring LED Retrofits

- 4.2.5 Increasing Demand for Plant-Factory Horticulture Lighting

- 4.2.6 Growth of Smart Lighting in IoT-Enabled Buildings

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions for Gallium and Indium

- 4.3.2 High Capital Expenditure for Micro-LED Mass Transfer

- 4.3.3 Intensifying Price Pressure from Chinese Suppliers

- 4.3.4 Patent Litigation Risks in LED Chip Designs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Toyoda Gosei Co., Ltd.

- 6.4.3 Rohm Co., Ltd.

- 6.4.4 Stanley Electric Co., Ltd.

- 6.4.5 Sharp Corporation

- 6.4.6 Sony Semiconductor Solutions Corporation

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 Osram Opto Semiconductors GmbH

- 6.4.9 Cree LED, Inc.

- 6.4.10 Samsung Electronics Co., Ltd.

- 6.4.11 LG Innotek Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Lumileds Holding B.V.

- 6.4.14 Bridgelux, Inc.

- 6.4.15 Everlight Electronics Co., Ltd.

- 6.4.16 Citizen Electronics Co., Ltd.

- 6.4.17 Kingbright Electronic Co., Ltd.

- 6.4.18 Dominant Opto Technologies Sdn. Bhd.

- 6.4.19 Lextar Electronics Corporation

- 6.4.20 NationStar Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment