PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063853

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063853

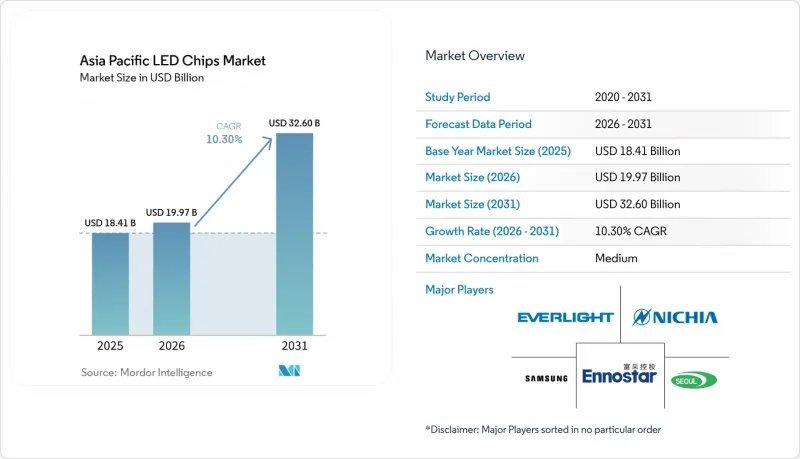

Asia Pacific LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia pacific lED chips market size is expected to grow from USD 18.41 billion in 2025 to USD 19.97 billion in 2026 and is forecast to reach USD 32.60 billion by 2031 at 10.3% CAGR over 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, Micro-LED), Semiconductor Material (GaN/InGaN, Algainp, Other Semiconductor Materials), Application (General Lighting, Automotive, and More), and Geography (China, Japan, India, South Korea, Southeast Asia, Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific LED Chips Market Trends and Insights

Government-Led "Make In India" Incentives For LED Chip Fabrication

India's Production Linked Incentive scheme grants 4-6% rewards on incremental sales of qualified LED components, spurring brownfield expansions and new fabs that target a steep jump in domestic value addition from below 20% toward 80%. Approved applicants have already pledged more than USD 1 billion, unlocking a pathway for global chip producers to diversify sourcing and cut reliance on any single country.Success depends on parallel investment in GaN epitaxy reactors, trained talent, and supportive infrastructure, areas now moving up the policy priority list.

Electrification Of Two-Wheeler Mobility In Southeast Asia

Electric scooters and motorcycles dominate urban transport in Vietnam, Thailand, and Indonesia, creating a surge in demand for power-efficient LED headlamps, taillights, and instrument clusters. Adaptive beams and daytime running lights raise the chip content per vehicle, while the tropical climate sets strict thermal performance requirements. Vehicle makers favor modular LED assemblies that lower assembly complexity and warranty costs, positioning chip vendors with robust thermal engineering capabilities for outsized gains.

Supply-Demand Mismatch Of 6-Inch GaN Epitaxial Wafers

LED, power, and RF device makers are competing for finite 6-inch GaN wafer capacity, a tension aggravated by the slow migration to 8-inch lines. Price volatility and allocation risk squeeze margins for chip producers lacking captive epitaxy or strategic supply agreements. The dynamic fuels vertical integration moves across China, Taiwan, and South Korea, but raises entry barriers for fabless design houses that depend on merchant wafer supply.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Targets Accelerating Industrial LED Retrofits

- Expanding Mini-LED Backlighting Adoption In High-End TVs

- Persistent Yield Challenges In Micro-LED Mass Transfer

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The conventional LED segment retained 80.36% share in 2025, anchoring the Asia Pacific LED chips market size with dependable cost-per-lumen economics at sub-USD 0.10 per chip. Mini-LED arrays have carved out a premium middle ground, supporting thousands of local dimming zones in televisions and monitors while avoiding the full mass-transfer burden of micro-LEDs. Premium TV makers are scaling screen sizes from 43-inch to 100-inch, raising chip counts per panel and creating fertile ground for value-added binning and thermal management services. Micro-LED chips, although still below 5% volume, are advancing at a 14.34% CAGR on the back of direct-emissive display pilots for ultra-large TVs and augmented-reality wearables. Suppliers that master six-sigma transfer yields and parallel laser tools stand to translate early technical wins into outsized revenue as micro-LED throughput improves.

Price pressure in commodity conventional LEDs continues to compress gross margins, prompting large fabs to automate wafer handling and adopt larger-format reactors to dilute fixed costs. Mini-LED's sweet spot in television backlighting is widening as blue-chip brands pair quantum dots with denser LED matrices to deliver OLED-like contrast, extending the segment's runway beyond the forecast horizon. Micro-LED architectures command pricing power that is two to three times higher than mini-LEDs on a per-lumen basis, but the Asia Pacific LED chips market still values predictable delivery schedules over bleeding-edge claims, explaining the cautious but steady pace of micro-LED capacity additions. Technology roadmaps across China, South Korea, and Taiwan now sequence incremental yield milestones, aiming for 99.9999% transfer performance by 2028, which will be a decisive inflection for volume adoption.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, an SGH Company

- Epistar Corporation

- EVERLIGHT Electronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lumileds Holding B.V.

- NationStar Optoelectronics Co., Ltd.

- Lite-On Technology Corporation

- TYNTEK Corporation

- Lextar Electronics Corporation

- Bridgelux, Inc.

- Ams-OSRAM AG

- Rohinni, LLC

- PlayNitride Inc.

- HC SemiTek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Mini-LED Backlighting Adoption in High-End TVs

- 4.2.2 Government-Led "Make in India" Incentives for LED Chip Fabrication

- 4.2.3 Growing Demand for UV-C LED Chips in Sterilization Systems

- 4.2.4 Electrification of Two-Wheeler Mobility in Southeast Asia

- 4.2.5 Phosphor-Free Micro-LED Architectures Reducing Cost per Lumen

- 4.2.6 Corporate Net-Zero Targets Accelerating Industrial LED Retrofits

- 4.3 Market Restraints

- 4.3.1 Persistent Yield Challenges in Micro-LED Mass Transfer

- 4.3.2 Supply-Demand Mismatch of 6-Inch GaN Epitaxial Wafers

- 4.3.3 Intellectual-Property Cross-Licensing Barriers for Start-Ups

- 4.3.4 Volatile Rare-Earth Phosphor Prices Affecting Chip Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Southeast Asia

- 5.4.6 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Cree LED, an SGH Company

- 6.4.5 Epistar Corporation

- 6.4.6 EVERLIGHT Electronics Co., Ltd.

- 6.4.7 San'an Optoelectronics Co., Ltd.

- 6.4.8 OSRAM Opto Semiconductors GmbH

- 6.4.9 LG Innotek Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Lumileds Holding B.V.

- 6.4.12 NationStar Optoelectronics Co., Ltd.

- 6.4.13 Lite-On Technology Corporation

- 6.4.14 TYNTEK Corporation

- 6.4.15 Lextar Electronics Corporation

- 6.4.16 Bridgelux, Inc.

- 6.4.17 Ams-OSRAM AG

- 6.4.18 Rohinni, LLC

- 6.4.19 PlayNitride Inc.

- 6.4.20 HC SemiTek Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment