PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063810

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063810

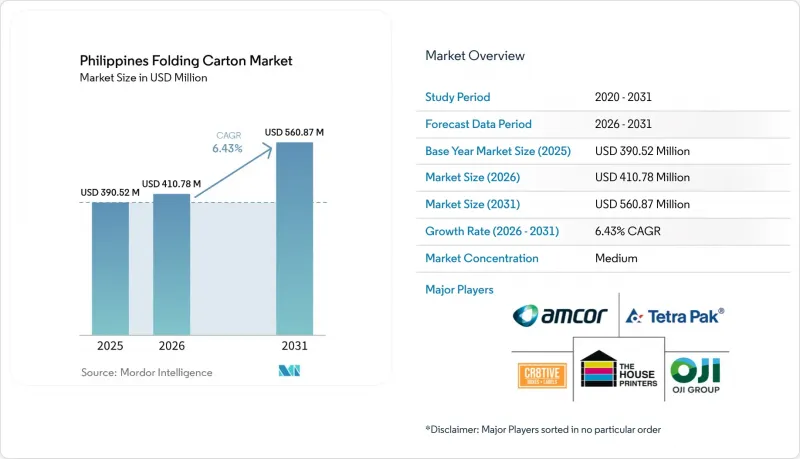

Philippines Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the philippines folding carton market size is projected to expand from USD 410.78 million in 2026 to USD 560.87 million by 2031, registering a 6.43% CAGR over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Gravure Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Folding Carton Market Trends and Insights

Growth of E-commerce Packaging Demand

Online grocery services and direct-to-consumer brands request tamper-evident seals and variable-data printing that personalize unboxing experiences. Cloud-based restaurant chains have secured fresh investment and rely on short-run cartons that can be sourced within days rather than weeks. The Department of Trade and Industry reports that 78% of Filipino consumers value sustainability when shopping online, encouraging fulfillment centers to specify recyclable paperboard in place of plastic pouches. Logistics providers highlight that fiber-based cartons lower dimensional-weight charges and offer 79% curbside recycling access in mature markets, a persuasive argument as domestic fuel costs remain volatile.

Expansion of Food and Beverage Processing Sector

More than PHP 20 billion (USD 352 million) has been deployed between 2024 and 2026 to enlarge domestic capacity for frozen foods, biscuits, coconut products, and seasonings. These projects cluster around cold-chain infrastructure in Luzon, locking in steady volumes of FDA-compliant, coated, unbleached kraft cartons with moisture barriers. Converters that certify substrates for food contact gain preferred-supplier status as processors tighten audit protocols. Adoption of electronic Certificates of Product Registration starting October 2025 increases traceability expectations, benefitting plants equipped with digital lot-coding.

Volatility in Paperboard Prices

Benchmark pulp climbed to USD 740 per ton in February 2026, a 15% jump in six months, tightening converter margins and triggering quarterly price-adjustment clauses. Philippine converters import nearly all virgin fiber, leaving them exposed to freight spikes and foreign-exchange swings. Inventories now run higher, but carrying extra stock strains working capital, especially for small printers whose credit lines are capped. Those conditions complicate converters' ability to offer fixed-price contracts, which many consumer-goods companies prefer. Until regional pulp supply stabilizes, cost pass-through will remain uneven.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Sustainable Packaging Solutions

- Increased Adoption of Digital Printing

- Limited Domestic Pulp Production Increasing Import Dependence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated unbleached kraft captured 32.83% of the Philippines folding carton market share in 2025 on the strength of its recyclability and suitability for food-contact applications. Solid bleached sulfate is forecast to outpace all other materials at a 7.76% CAGR, buoyed by premium cosmetics and pharmaceutical launches that require high-brightness substrates and tamper-evident seals. The Philippines folding carton market size attributed to coated unbleached kraft will rise in parallel with frozen food and quick-service restaurant growth. Pharmaceutical producers sourcing cartons for oral solids already specify child-resistant designs that favor premium bleached board.

Solid bleached sulfate benefits further from rising demand for deluxe finishes such as embossing and metallic accents in skin-care lines distributed through department stores and e-commerce platforms. Folding boxboard provides a cost-effective option for dry groceries and mid-tier household goods, while white-lined chipboard persists in shoe boxes and industrial packs where aesthetics rank below price. Recycled-content grades make incremental headway as EPR compliance drives brand owners to publish recyclability scores on front-of-pack graphics.

List of Companies Covered in this Report:

- Tetra Pak (Philippines), Inc.

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Amcor plc

- Printwell Inc.

- VJ7 Printing and Packaging Inc.

- Papercon Philippines Inc.

- The House Printers Corporation

- Majestic Press Inc.

- Apo International Marketing Corporation

- Grand C Graphics Inc.

- Starkson Packaging Inc.

- Fortune Packaging Corporation

- Megaprint Offset and Packaging Corp.

- Cr8tive Boxes & Labels Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Food and Beverage Processing Sector

- 4.2.2 Growth of E-commerce Packaging Demand

- 4.2.3 Rising Demand for Sustainable Packaging Solutions

- 4.2.4 Increased Adoption of Digital Printing for Short-Run Cartons

- 4.2.5 Government Excise Tax on Plastic Packaging Spurring Shift Toward Paperboard

- 4.2.6 Rapid Growth of Cloud Kitchen and Meal-Kit Start-ups Requiring Small-Batch Cartons

- 4.3 Market Restraints

- 4.3.1 Volatility in Paperboard Prices

- 4.3.2 Competition From Flexible Packaging Alternatives

- 4.3.3 Limited Domestic Pulp Production Increasing Import Dependence

- 4.3.4 Power Supply Interruptions Elevating Production Costs for Converters

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Tetra Pak (Philippines), Inc.

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Stora Enso Oyj

- 6.4.4 Rengo Co., Ltd.

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Amcor plc

- 6.4.7 Printwell Inc.

- 6.4.8 VJ7 Printing and Packaging Inc.

- 6.4.9 Papercon Philippines Inc.

- 6.4.10 The House Printers Corporation

- 6.4.11 Majestic Press Inc.

- 6.4.12 Apo International Marketing Corporation

- 6.4.13 Grand C Graphics Inc.

- 6.4.14 Starkson Packaging Inc.

- 6.4.15 Fortune Packaging Corporation

- 6.4.16 Megaprint Offset and Packaging Corp.

- 6.4.17 Cr8tive Boxes & Labels Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment