PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066538

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066538

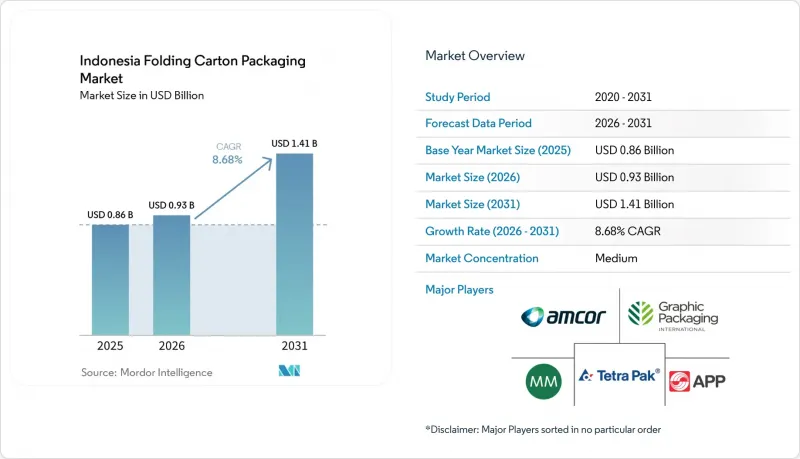

Indonesia Folding Carton Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia folding carton packaging market size was valued at USD 0.86 billion in 2025 and is projected to reach USD 1.41 billion by 2031, growing at a CAGR of 8.68% during 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Personal Care and Cosmetics, Healthcare/Pharmaceuticals, and More). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Folding Carton Packaging Market Trends and Insights

Surging E-Commerce Penetration Driving Demand for Ready-To-Ship Cartons

The Indonesia folding carton packaging market is gaining direct support from the country's large and still-expanding digital commerce base, with Indonesia's digital economy nearing the USD 100 billion mark in 2025 and remaining the largest in Southeast Asia. In 2025, e-commerce GMV reached USD 71 billion, and in 2026, online transaction activity continues to broaden across both major metros and secondary cities. Cartons now serve 2 roles at once: protecting products in transit and serving as a visible brand surface during delivery and unboxing. Live-streaming commerce rose from less than 5% of Indonesia's online GMV in 2022 to around 20% in 2025, making short-run, versioned, and camera-ready packaging far more relevant to brand owners. The daily parcel flow handled by J&T Express, JNE, and SiCepat exceeds 3 million units, so durable outer presentation has become part of the product experience rather than a secondary packaging concern. This is why converters that can deliver fast-turn, digitally printed, retail-ready packs are positioned to capture a larger share of new demand in the Indonesia folding carton packaging market.

Rising Food-Safety Regulations Favoring Paper-Based Packaging

The Indonesia folding carton packaging market is also being shaped by a tighter compliance framework for food-contact substrates. Indonesia's Ministry of Industry issued Permenperin No. 6/2025 on January 24, 2025, which made SNI 8218:2024 mandatory for paper and cardboard used as primary food packaging materials, effective July 24, 2025, with a transition deadline of July 24, 2026, for products manufactured or imported before the effective date. The regulation covers multiple paper and board grades used in primary food packaging, meaning compliance is now tied directly to standard procurement decisions rather than treated as a specialized requirement. In parallel, the Food and Drug Authority conducted a public consultation in October 2025 on a revised food contact materials regulation that sets specific and overall migration limits for packaging materials, including paper and cardboard. This combination favors mills and converters that have already invested in certification, testing, and traceability, as it provides brand owners with a safer route to compliance. Food and beverage companies that shift toward compliant FBB and SBS grades not only meet current requirements but also reduce future enforcement risk. That dynamic gives paper-based formats a more durable place in the Indonesia folding carton packaging market.

Volatility in Recovered Paper Import Policies

The Indonesian folding carton packaging market remains exposed to input risk because domestic secondary fiber collection is still insufficient to meet mill requirements on its own. Total paper imports reached USD 3.4 billion in 2024 and an estimated USD 3.6 billion in 2025, while rising imports from China prompted the Indonesian Pulp and Paper Association to request anti-dumping investigations in duplex and packaging paper categories. This creates pricing pressure from 2 directions: mills face uncertainty in raw material sourcing, while local producers also have to respond to competitive import flows. Integrated players can manage that pressure more effectively because they have a larger procurement scale and stronger control over board supply. Smaller converters are more exposed, since even modest shifts in paper input costs can quickly affect quoted prices and order profitability. Until local recovery systems scale up, this issue will remain a recurring drag on the Indonesian folding carton packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Middle-Class Purchasing Power Stimulating Branded Goods

- Expansion of Quick-Service Restaurants and Takeaway Culture

- Competition From Flexible Plastics in Cost-Sensitive Segments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 37.48% of the Indonesia folding carton packaging market share within the material type in 2025. Its lead position came from uses where stiffness, clean print reproduction, and a smooth surface are important, especially in food, healthcare, and personal care cartons. These categories tend to value both appearance and structural reliability, which keeps FBB relevant across a wide range of branded uses. Domestic supply improved after APRIL Group brought its Kerinci paperboard mill into operation, investing USD 2.3 billion and achieving an annual capacity of 1.2 million metric tons under the BoardOne and SilverPak brands. That capacity addition gives local converters better access to premium board and helps reduce dependence on imported supply for high-specification cartons.

Solid bleached sulfate kept a premium role in healthcare and cosmetics packaging, where whiteness, surface quality, and sharp graphics remain specification-critical. Its growth is steadier than that of more economical grades because many mid-tier brand owners still weigh visual quality against cost. The Indonesia folding carton packaging market size for coated unbleached kraft is projected to expand at 10.12% CAGR from 2026 to 2031, making it the fastest-growing material type. CUK is benefiting from its grease resistance and stronger structure, which make it useful in fast-food service packs, e-commerce transit packs, and other applications that need both durability and acceptable presentation. APP Group's May 2025 launch of Sinar Vanda Hi-Brite C1S, which offered 10-20% higher yield at 92 brightness, shows that mills in Indonesia are still investing in product development for premium paperboard requirements without giving up cost discipline.

List of Companies Covered in this Report:

- PT Graphic Packaging International Indonesia

- Mayr-Melnhof Karton AG

- PT. Indah Kiat Pulp & Paper Tbk

- PT. Pabrik Kertas Tjiwi Kimia Tbk

- PT. Amcor Flexibles Indonesia

- Asia Pulp & Paper (APP) Group

- PT. Primacipta Megah Abadi

- PT. Printec Perkasa

- PT. Kertas Basuki Rachmat Indonesia Tbk

- PT. Sinar Dunia Makmur

- PT. Wiraprint Packaging

- PT. Ultra Prima Abadi

- PT. Sopanusa Tissue and Packaging Saranasukses

- PT Impack Pratama Industri Tbk

- Tetra Pak International S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging E-commerce Penetration Driving Demand for Ready-to-Ship Cartons

- 4.2.2 Rising Food-Safety Regulations Favoring Paper-Based Packaging

- 4.2.3 Growing Middle-Class Purchasing Power Stimulating Branded Goods

- 4.2.4 Expansion of Quick-Service Restaurants and Takeaway Culture

- 4.2.5 Adoption of Digital Printing for Short-Run Personalization

- 4.2.6 Government Incentives for Domestic Paperboard Production

- 4.3 Market Restraints

- 4.3.1 Volatility in Recovered Paper Import Policies

- 4.3.2 Competition from Flexible Plastics in Cost-Sensitive Segments

- 4.3.3 Limited Collection Infrastructure for Post-consumer Cartons

- 4.3.4 Energy-Price Fluctuations Escalating Converting Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 PT Graphic Packaging International Indonesia

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 PT. Indah Kiat Pulp & Paper Tbk

- 6.4.4 PT. Pabrik Kertas Tjiwi Kimia Tbk

- 6.4.5 PT. Amcor Flexibles Indonesia

- 6.4.6 Asia Pulp & Paper (APP) Group

- 6.4.7 PT. Primacipta Megah Abadi

- 6.4.8 PT. Printec Perkasa

- 6.4.9 PT. Kertas Basuki Rachmat Indonesia Tbk

- 6.4.10 PT. Sinar Dunia Makmur

- 6.4.11 PT. Wiraprint Packaging

- 6.4.12 PT. Ultra Prima Abadi

- 6.4.13 PT. Sopanusa Tissue and Packaging Saranasukses

- 6.4.14 PT Impack Pratama Industri Tbk

- 6.4.15 Tetra Pak International S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment