PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066595

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066595

Thailand Folding Carton Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

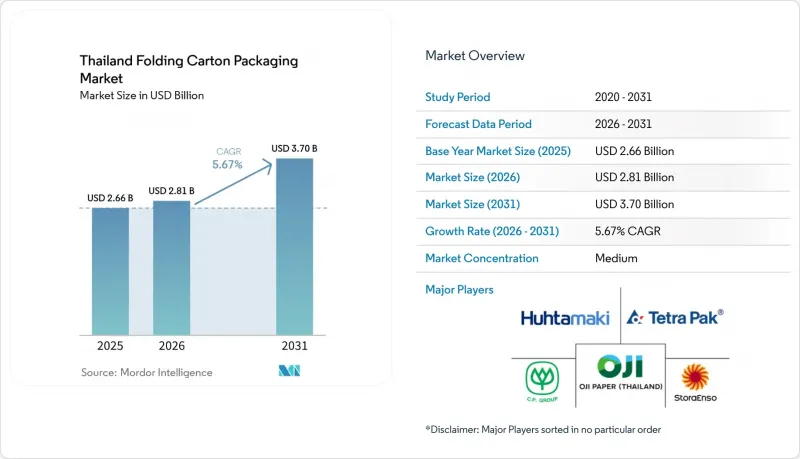

According to Mordor Intelligence, the thailand folding carton packaging market was valued at USD 2.66 billion in 2025 and estimated to grow from USD 2.81 billion in 2026 to reach USD 3.7 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031).

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, E-Commerce and Retail-Ready Packaging, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

Thailand Folding Carton Packaging Market Trends and Insights

Robust E-Commerce Volume Growth and Sustainability Commitments

Thai online retail sales reached USD 26.5 billion in 2023 and are projected to reach USD 32 billion by 2025, driving demand for protective yet brand-forward folding cartons. Large platforms increasingly mandate recycled content to align with corporate ESG goals, compelling converters to secure stable recycled fiber supplies despite volatile import flows. Retailers expanding their omnichannel operations require standardized die lines that can move seamlessly from warehouse to doorstep, pushing multipurpose carton designs. Sustainability pledges are driving the adoption of water-based coatings as PFAS-free alternatives, despite the persistence of cost premiums of USD 0.02-0.05 per m2. Together, rising parcel counts and green-packaging targets underpin consistent mid-single-digit volume growth for the Thailand folding carton packaging market.

FMCG Brand Shift Toward Premium Printed Cartons

Thailand's middle-income households and tourist influx encourage brand owners to upgrade shelf presence with embossed, matte-varnish, and holographic carton finishes. Shorter product lifecycles and seasonal collections require nimble changeovers, a sweet spot for digital presses capable of 15-minute makereadies. R&D spending by technology vendors such as Tetra Pak, about EUR 100 million (USD 118 million) per year, is channeling barrier coatings that enable the reduction of plant energy use by 40% while supporting premium graphics. Premiumization is most visible in personal-care, cosmetics, and specialty confectionery, where packaging is a primary purchase trigger.

Recycled Paperboard Price Volatility Linked to China's Import Policy

China's 2018 ban on mixed-paper imports cascaded into Southeast Asia, flooding Thai mills with inconsistent feedstock and sending mixed-paper prices from above USD 60 per ton in 2017 to near zero before rebounding. Converters struggle to hedge cost swings because domestic collection rates lag developed-market norms. Recent capacity additions in regional recycling plants are narrowing quality gaps, yet policy pivots, such as potential quota reductions in Indonesia, keep price risk elevated. Larger Thai players stock three-month fiber inventories, but SMEs operating on thin working capital cannot absorb sudden spikes, compressing margins and occasionally prompting production halts.

Other drivers and restraints analyzed in the detailed report include:

- Government EPR Draft Law Catalyzing Recycled-Content Demand

- Commercial Rollout of Digital Short-Run Carton Presses

- Soaring Industrial Electricity Tariffs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White-lined chipboard accounted for 45.15% of the Thailand folding carton packaging market in 2025, due to its printability and cost advantage. Brands favor its smooth surface for high-resolution imagery, but folding boxboard is growing at a 6.51% CAGR as retailers pledge to reach 30% recycled content by 2030. Folding boxboard's stiffness-to-weight ratio enables down-gauging, which reduces freight costs by 8-10% for cross-border shipments to the CLMV (Cambodia, Laos, Myanmar, Vietnam). Solid bleached board maintains a niche use in cosmetics, where brightness metrics serve shelf-impact goals; however, its higher cost limits mass adoption. Coated unbleached kraftboard appeals to electronics exporters who value puncture resistance for heavy components.

Barrier-coated grades integrating vapor-deposited aluminum oxide (AlOx) raise the functional ceiling for folding boxboard, enabling migration-safe packaging for nuts, chocolate, and powdered drinks. SRF Limited's third BOBST metallizer installation, scheduled for September 2025 in Rayong, will increase the regional output of high-barrier films that feed laminate structures. These material shifts underscore an emerging hierarchy where chipboard dominates volume but folding boxboard captures reputational mindshare in the Thailand folding carton packaging market.

List of Companies Covered in this Report:

- Siam Toppan Packaging Co., Ltd.

- SCG Packaging Public Company Limited

- Thai Containers Group Co., Ltd.

- Thung Hua Sinn Company Limited

- Continental Packaging (Thailand) Co., Ltd.

- Oji Paper (Thailand) Ltd.

- ASA Group Co., Ltd.

- Sarnti Packing Co., Ltd.

- Thai Card-Board Company Limited

- S&D Industries Company Limited

- J.K. Cartons Group Co., Ltd.

- Huhtamaki (Thailand) Ltd.

- Tetra Pak (Thailand) Ltd.

- Ratchapruek Packaging Co., Ltd.

- Print Master Co., Ltd.

- SC Packaging Asia Co., Ltd.

- Stora Enso (Thailand) Co., Ltd.

- Charoen Pokphand Packaging Co., Ltd.

- Great Wall Enterprise (Thailand) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust E-Commerce Volume Growth and Sustainability Commitments

- 4.2.2 FMCG Brand Shift Toward Premium Printed Cartons

- 4.2.3 Government EPR Draft Law Catalyzing Recycled-Content Demand

- 4.2.4 Commercial Rollout of Digital Short-Run Carton Presses

- 4.2.5 High-Speed Offset Capacity Relocations from China to Thailand

- 4.2.6 Meal-Kit and Ready-Meal Subscriptions Surge

- 4.3 Market Restraints

- 4.3.1 Recycled Paperboard Price Volatility Linked to China's Import Policy

- 4.3.2 Soaring Industrial Electricity Tariffs

- 4.3.3 Fragmented SME Converting Base Limiting Quality Control

- 4.3.4 PFAS-Free Coating Compliance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Siam Toppan Packaging Co., Ltd.

- 6.4.2 SCG Packaging Public Company Limited

- 6.4.3 Thai Containers Group Co., Ltd.

- 6.4.4 Thung Hua Sinn Company Limited

- 6.4.5 Continental Packaging (Thailand) Co., Ltd.

- 6.4.6 Oji Paper (Thailand) Ltd.

- 6.4.7 ASA Group Co., Ltd.

- 6.4.8 Sarnti Packing Co., Ltd.

- 6.4.9 Thai Card-Board Company Limited

- 6.4.10 S&D Industries Company Limited

- 6.4.11 J.K. Cartons Group Co., Ltd.

- 6.4.12 Huhtamaki (Thailand) Ltd.

- 6.4.13 Tetra Pak (Thailand) Ltd.

- 6.4.14 Ratchapruek Packaging Co., Ltd.

- 6.4.15 Print Master Co., Ltd.

- 6.4.16 SC Packaging Asia Co., Ltd.

- 6.4.17 Stora Enso (Thailand) Co., Ltd.

- 6.4.18 Charoen Pokphand Packaging Co., Ltd.

- 6.4.19 Great Wall Enterprise (Thailand) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment