PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063873

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063873

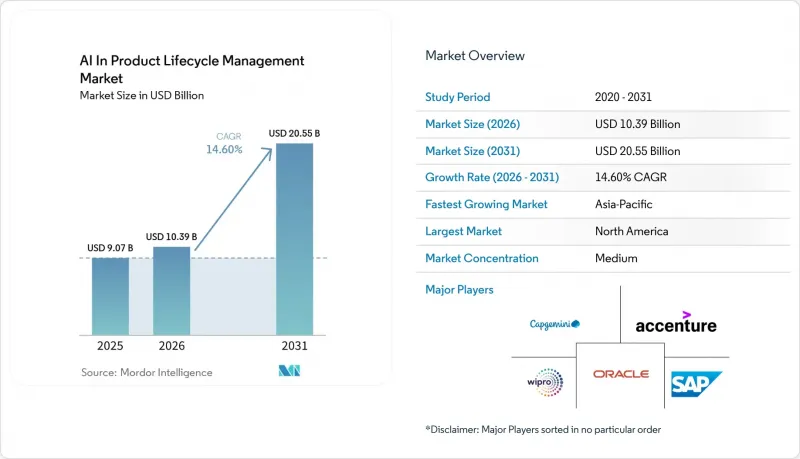

AI In Product Lifecycle Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in product lifecycle management market size is projected to expand from USD 9.07 billion in 2025 and USD 10.39 billion in 2026 to USD 20.55 billion by 2031, registering a CAGR of 14.60% between 2026 to 2031.

This report is Segmented by Component (Software, Services), Deployment Mode (Cloud/SaaS, On-Premises, Hybrid), Application (PDM & BOM, Design Collaboration, Quality & Compliance, Digital Twin, and Others), End User (Automotive, Aerospace & Defense, Healthcare, Industrial Equipment, and Others), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global AI In Product Lifecycle Management Market Trends and Insights

Cloud/SaaS PLM Modernization and Digital Thread Buildout

Cloud-native infrastructure enables compute-intensive tasks, such as large-scale BOM semantic searches and real-time visual similarity checks, which are integral to AI in product lifecycle management. Over half of new Aras Innovator deployments now operate as SaaS, including defense-grade GovCloud instances that meet ITAR and CMMC requirements. This shift reduces entry barriers for mid-sized firms by eliminating significant upfront server investments. It also ensures standardized security updates and performance enhancements, allowing engineering teams uninterrupted access to the latest AI models. Vendors are increasingly introducing usage-based AI micro-services, priced separately from core PLM licenses, driving additional revenue growth beyond traditional user-based metrics.

Compliance, Traceability, and Quality Automation Needs

Regulators now require manufacturers to maintain comprehensive digital audit trails that document every requirement, design decision, and validation artifact. The U.S. FDA's Quality Management System Regulation, effective February 2026, expands oversight to include AI-enabled production software, making AI-native PLM essential for compliance in the med-tech industry. In response, PTC has introduced Codebeamer AI assistants that automatically generate test cases aligned with industry standards, reducing manual traceability efforts by nearly 50%. Similar functionalities are being integrated into the portfolios of other vendors, such as Dassault Systemes and Siemens, as they embed risk-scoring logic into engineering workflows. These advancements streamline validation cycles across life-sciences supply chains and allow quality engineers to focus on higher-value analytical tasks.

Legacy System Integration and Fragmented Data Models

Many large manufacturers, having acquired multiple PLM instances through mergers, face challenges with inconsistent part numbering systems and revision methodologies. Consolidating these disparate systems into a unified semantic layer requires significant investment in mapping processes, which is essential for AI to generate actionable and traceable insights. On average, data-conversion projects at automotive Tier-1 suppliers now take approximately 18 months to complete and account for 4% of annual engineering IT budgets. While graph-based knowledge layers offer a viable solution, most Fortune 500 OEMs anticipate this transition extending into their next planning cycle.

Other drivers and restraints analyzed in the detailed report include:

- Rising Product Complexity and Multi-Domain Engineering

- Need to Shorten Time-to-Market and Change-Cycle Latency

- IP Security, Governance, and Explainability Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software held a 62.15% revenue share in the AI-driven product lifecycle management market. This dominance is primarily due to AI capabilities integrated into major PLM suites, including Siemens' Teamcenter, Dassault Systemes' 3DEXPERIENCE, and PTC's Windchill. Features such as voice-driven BOM navigation, generative design sketches, and automated requirement summarization not only ensure seat renewals but also drive expansion into new accounts.

While service revenue is smaller in absolute terms compared to licenses, it is growing at a faster pace. Systems integration specialists focus on re-platforming historical data, managing cloud migrations, and optimizing large-language-model prompts to align with client-specific taxonomies. These services often extend beyond the initial implementation phase, evolving into managed service subscriptions aligned with the customer's AI model refresh cycles. This trend supports a 15.95% CAGR for services, surpassing overall market growth while reinforcing the dominance of established platforms.

In 2025, cloud and SaaS deployments accounted for 54.15% of total spending, with this share expected to grow as compute-intensive tasks increasingly rely on elastic infrastructures. The market size for AI in product lifecycle management driven by cloud deployments is projected to grow at a 16.15% CAGR through 2031. Multitenant architectures enable vendors to deliver weekly model updates without disrupting customer operations, a capability that is challenging to replicate on self-hosted servers.

Hybrid strategies, commonly adopted by Japanese and German OEMs, combine local control for sensitive files with on-demand GPU resources for tasks such as simulation and generative design. Tesla's use of Dassault Systemes' 3DEXPERIENCE in a containerized on-premises instance highlights how high-volume manufacturers prioritize low latency and consistent throughput. Over time, software vendors are introducing secure edge appliances that synchronize only non-sensitive data to the public cloud, gradually encouraging conservative users to adopt broader SaaS solutions and expanding the market.

Geography Analysis

In 2025, North America commanded a dominant 38.65% share of global revenue, spearheaded by sectors such as aerospace, defense, semiconductors, and electric vehicles, all of which prioritize stringent engineering change controls. Federal procurement policies favoring digital-thread maturity, combined with the FDA's 2026 release of the Computer Software Assurance guidance, establish a foundational compliance standard. This standard ensures project funding continuity and provides a buffer during broader economic slowdowns. Additionally, the region's robust presence of cloud hyperscalers accelerates the realization of value from generative AI pilots, solidifying its lead in the AI-driven product lifecycle management arena.

Europe, while currently holding the second spot in spending, is on a rapid ascent. This surge is largely attributed to the EU's impending Digital Product Passport and Ecodesign regulations, which are seamlessly integrating lifecycle assessments into design processes. The DACH region, already home to some of the densest Product Lifecycle Management (PLM) systems globally, stands to gain significantly. By infusing AI intelligence into these existing systems, they can expect immediate reductions in cycle times. Notably, Dassault Systemes highlighted an 8% year-on-year growth in its European Industrial Innovation software revenue for Q3 2025, a surge directly tied to AI-driven license upgrades.

Asia-Pacific is set to be the powerhouse of the AI-driven product lifecycle management market, boasting a projected CAGR of 16.50%. In China, battery-electric vehicle manufacturers are swiftly adopting AI-centric PLM strategies to expedite model iterations. Japanese OEMs are navigating data residency challenges, opting for a phased cloud strategy. They often choose hybrid models, retaining geometry data onshore while leveraging regional data centers for intensive computational tasks. In India, engineering service firms are developing PLM-AI tools, streamlining migration processes for Western clients. This not only underscores India's significance as a PLM adopter but also as a key exporter of PLM expertise.

- Accenture

- Aras

- Arena Solutions

- Autodesk

- Capgemini

- Centric Software

- CONTACT Software

- Dassault Systemes

- HCLTech

- IBM

- Infor

- Lectra

- OpenBOM

- Oracle

- Propel Software

- PTC

- SAP

- Siemens Healthineer AG

- Tata Technologies

- Wipro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Product Complexity and Multi-Domain Engineering

- 4.2.2 Need to Shorten Time-To-Market and Change-Cycle Latency

- 4.2.3 Cloud/Saas PLM Modernization and Digital Thread Buildout

- 4.2.4 Compliance, Traceability, and Quality Automation Needs

- 4.2.5 AI-Powered Lifecycle Sustainability and LCA Inside PLM

- 4.2.6 AI Conversion of Legacy Engineering Documents into Reusable Product Memory

- 4.3 Market Restraints

- 4.3.1 Legacy System Integration and Fragmented Data Models

- 4.3.2 IP Security, Governance, and Explainability Requirements

- 4.3.3 Copilot-In-A-Silo Problem Across PLM/ERP/MES/ALM Ecosystems

- 4.3.4 Embedding/Vector-Store Governance and Stale Lifecycle Context

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud / SaaS

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Product Data Management & BOM Intelligence

- 5.3.2 Design & Engineering Collaboration

- 5.3.3 Change, Release & Workflow Automation

- 5.3.4 Quality, Compliance & Traceability

- 5.3.5 Digital Twin, Simulation & Lifecycle Analytics

- 5.3.6 Portfolio, Program & Requirements Management

- 5.3.7 Manufacturing Handoff & Closed-loop Feedback

- 5.4 By End User

- 5.4.1 Automotive & Transportation

- 5.4.2 Aerospace & Defense

- 5.4.3 Industrial Equipment & Heavy Machinery

- 5.4.4 Semiconductor & Electronics

- 5.4.5 Healthcare & Medical Devices

- 5.4.6 Consumer Goods, Fashion & Retail

- 5.4.7 Chemicals & Materials

- 5.4.8 Energy, Utilities & Infrastructure

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accenture

- 6.3.2 Aras

- 6.3.3 Arena Solutions

- 6.3.4 Autodesk

- 6.3.5 Capgemini

- 6.3.6 Centric Software

- 6.3.7 CONTACT Software

- 6.3.8 Dassault Systemes

- 6.3.9 HCLTech

- 6.3.10 IBM

- 6.3.11 Infor

- 6.3.12 Lectra

- 6.3.13 OpenBOM

- 6.3.14 Oracle

- 6.3.15 Propel Software

- 6.3.16 PTC

- 6.3.17 SAP

- 6.3.18 Siemens Healthineer AG

- 6.3.19 Tata Technologies

- 6.3.20 Wipro

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment