PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063899

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063899

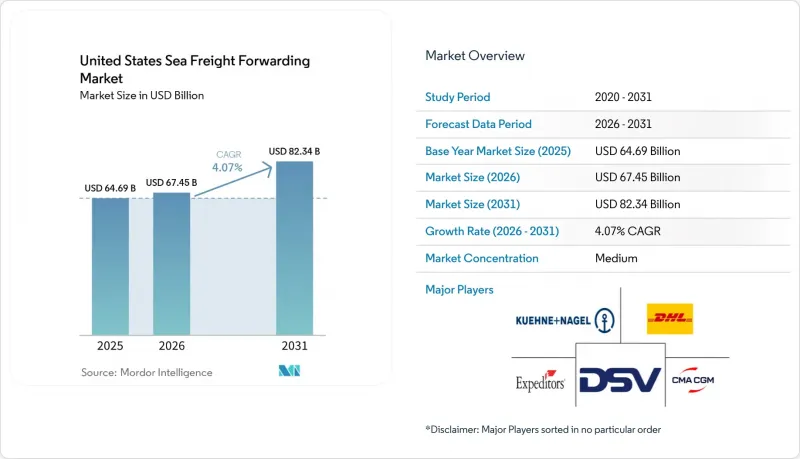

United States Sea Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states sea freight forwarding market size is projected to expand from USD 64.69 billion in 2025 and USD 67.45 billion in 2026 to USD 82.34 billion by 2031, registering a CAGR of 4.07% between 2026 and 2031.

Persistent demand for Asia-origin imports, gradual port automation, and a growing preference for flexible shipping options underpin the expansion. This report is Segmented by Service (Full-Container-Load, Less-Than-Container-Load), by Cargo Type (Dry/General, Reefer), by End-User Industry (Electronics and Semiconductors, Chemicals and Petrochemicals, Food and Beverage, Pharmaceuticals and Healthcare, and More), and by Geography (Northeast, Southeast, Midwest, Southwest, West). Market Forecasts are Provided in Terms of Value (USD).

United States Sea Freight Forwarding Market Trends and Insights

Expansion of US Import Volumes from Asia

Containerized imports from Asia keep the revenue engine running for the United States sea freight forwarding market. Cargo now skews toward semiconductors, medical devices, and electric-vehicle parts that tolerate premium rates for schedule reliability. Forwarders that diversify beyond the traditional Los Angeles-Long Beach complex to Savannah, Houston, and New York relieve congestion risk for customers. A multi-gateway strategy secures market share when labor or weather disrupts any single coast.

Improvements in Port Infrastructure and Automation Projects

Automated cranes and 24-hour gate operations reduce dwell times and lift terminal throughput. The Port of Savannah's Garden City upgrade and Pier 400's robotic handling in Los Angeles give forwarders with preferred slot access measurable velocity gains. The Infrastructure Investment and Jobs Act earmarks USD 17 billion to modernize waterways, but early movers reap benefits sooner, while competitors reliant on legacy facilities face longer truck turn times.

Port Congestion and Labor Disruptions

The 2024 strikes and the subsequent 61.5% wage increase embedded higher costs into every container that moves through East and Gulf Coast docks. Average truck dwell times at Los Angeles and Long Beach stabilized at under three days in late 2025, helping forwarders manage per-diem bills. Diversifying port calls helps mitigate future risk but adds complexity and reduces economies of scale. Shippers watch congestion metrics closely, rewarding partners that reroute quickly when bottlenecks emerge.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Digital Freight Platforms

- E-Commerce Demand for Bulky-Goods Logistics

- Volatile Bunker-Fuel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-container-load services accounted for 73.11% of revenue in the United States sea freight forwarding market in 2025. FCL dominates where predictable demand lets shippers fill a 40-foot box with electronics, machinery, or auto parts. Less-than-Container-Load services, while smaller, are climbing at a 6.79% CAGR, reflecting retail's pivot to frequent, smaller replenishment cycles.

Forwarders that master LCL consolidation blend multiple shipper orders, lowering per-unit costs while capturing premium handling fees. Warehouse management systems link with transportation management systems to automate load planning and reduce errors. Successful providers also integrate customs brokerage and domestic trucking, offering a seamless door-to-door proposition for e-commerce sellers. Digital booking portals lower administrative workload, allowing staff to focus on exception management. The result is steady LCL margin expansion even as cargo pieces proliferate.

List of Companies Covered in this Report:

- Kuehne + Nagel

- DHL Global Forwarding

- DSV (incl. DB Schenker)

- CMA CGM Group (Including CEVA Logistics)

- Expeditors International

- C.H. Robinson

- Nippon Express

- GEODIS

- A.P. Moller - Maersk

- Hellmann Worldwide Logistics

- Kintetsu World Express

- BDP International (now part of PSA International)

- Savino Del Bene

- Fracht Group

- Crane Worldwide Logistics

- SEKO Logistics

- Flexport

- AIT Worldwide Logistics

- OEC Group

- Dimerco Express Group

- Mallory Alexander International Logistics

- Radiant Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.1.1 Expansion of US Import Volumes from Asia

- 4.1.2 Improvements in Port Infrastructure and Automation Projects

- 4.1.3 Rising Adoption of Digital Freight Platforms

- 4.1.4 E-Commerce Demand for Bulky Goods Logistics

- 4.1.5 Offshore-Wind Project-Cargo Opportunities (East Coast)

- 4.1.6 Shipper Preference for ESG-Certified Forwarders

- 4.2 Market Restraints

- 4.2.1 Port Congestion and Labor Disruptions

- 4.2.2 Volatile Bunker-Fuel Prices

- 4.2.3 Stricter IMO Environmental Regulations

- 4.2.4 Limited US Marine-Insurance Capacity for High-Risk Cargo

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Technology Innovations Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Rivalry Among Competitors

- 4.7 Freight-Rate and Surcharges Trend Analysis

- 4.8 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service

- 5.1.1 Full-Container-Load (FCL)

- 5.1.2 Less-than-Container-Load (LCL)

- 5.2 By Cargo Type

- 5.2.1 Dry/General

- 5.2.2 Reefer

- 5.3 By End User Industry

- 5.3.1 Electronics and Semiconductors

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Food and Beverage

- 5.3.4 Pharmaceuticals and Healthcare

- 5.3.5 Retail and E-commerce

- 5.3.6 Others

- 5.4 By Region

- 5.4.1 Northeast

- 5.4.2 Southeast

- 5.4.3 Midwest

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Kuehne + Nagel

- 6.4.2 DHL Global Forwarding

- 6.4.3 DSV (incl. DB Schenker)

- 6.4.4 CMA CGM Group (Including CEVA Logistics)

- 6.4.5 Expeditors International

- 6.4.6 C.H. Robinson

- 6.4.7 Nippon Express

- 6.4.8 GEODIS

- 6.4.9 A.P. Moller - Maersk

- 6.4.10 Hellmann Worldwide Logistics

- 6.4.11 Kintetsu World Express

- 6.4.12 BDP International (now part of PSA International)

- 6.4.13 Savino Del Bene

- 6.4.14 Fracht Group

- 6.4.15 Crane Worldwide Logistics

- 6.4.16 SEKO Logistics

- 6.4.17 Flexport

- 6.4.18 AIT Worldwide Logistics

- 6.4.19 OEC Group

- 6.4.20 Dimerco Express Group

- 6.4.21 Mallory Alexander International Logistics

- 6.4.22 Radiant Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment