PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063931

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063931

Human Capital Management (HCM) Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

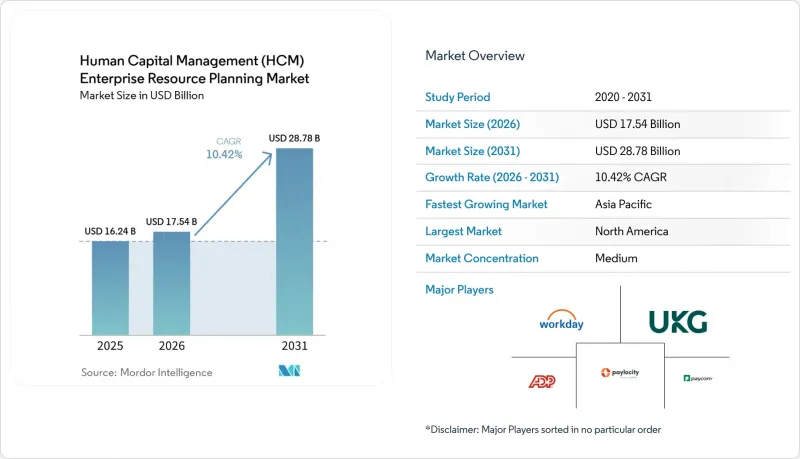

According to Mordor Intelligence, the human capital management (HCM) enterprise resource planning (ERP) market size is projected to expand from USD 17.54 billion in 2026 to USD 28.78 billion by 2031, registering a CAGR of 10.42% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (Manufacturing, BFSI, Healthcare, Retail and E-Commerce, IT and Telecom, Government, and More), Component or Module (Core HR, Talent Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Human Capital Management (HCM) Enterprise Resource Planning Market Trends and Insights

Accelerated Transition to Cloud-Native HR Suites

Organizations are migrating from on-premise ERP add-ons to cloud platforms that cut hardware expense and reduce upgrade pain. Oracle reported double-digit HCM Cloud customer growth in fiscal 2025, citing deployment cycles of 6-9 months compared with 18-24 months on legacy stacks. Workday's 2026R1 embedded AI agents that resolve routine queries, freeing HR staff for strategic planning. Subscription pricing converts capital outlays into variable operating costs, aligning spend with headcount volatility. ADP's Lyric unified data model reduces integration overhead and shortens implementation time. Still, data-cleansing challenges and workflow re-engineering slow heavily customized enterprises.

Demand for Analytics-Driven Workforce Planning

Predictive analytics help employers anticipate skills gaps, optimize labor budgets, and flag attrition risk. Workday users achieved 50% better nurse retention via AI-driven models. The U.S. Bureau of Labor Statistics projects a shortfall of 1.9 million registered nurses by 2031, intensifying demand for retention analytics. Manufacturers deploy skills intelligence to retrain workers on robotics and additive manufacturing, lowering external hiring costs. Oracle's Dynamic Skills surfaces internal candidates, cutting time-to-fill by about 30%. Regulators are watching algorithmic bias, and the EEOC has issued guidance on explainability.

High Switching Costs From Legacy ERP

Data migration can last 6-12 months and require costly consultants, reaching 15-20% of annual subscription fees. Enterprises must write off sunk licenses, pay overlapping subscriptions, and retrain users, deterring near-term moves. Customized union scheduling in manufacturing and healthcare raises re-engineering hurdles, stretching payback periods.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Complexity in Multi-Country Payroll

- Rise of Remote and Hybrid Work Models

- Data Privacy and Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 62.13% of the human capital management ERP market in 2025 and are expected to grow at a 15.12% CAGR through 2031. Pure cloud bookings represented 85% of Workday's new deals, reflecting customer preference for continuous feature delivery. Hybrid strategies persist for governments and defense agencies that keep payroll engines on-premise to satisfy security mandates. However, maintaining dual stacks undercuts savings, and vendors are phasing out legacy versions.

The human capital management ERP market increasingly rewards platforms that align fees with active headcount, allowing firms to flex spend during cycles. Oracle HCM Cloud 25A pushed AI payroll reconciliation to subscribers months ahead of on-premise clients, underscoring the innovation gap. Data-residency rules may slow full-stack adoption in Europe and Asia-Pacific, but most multinationals prefer localized regions over hybrid builds.

Large enterprises contributed 57.23% revenue in 2025 and require audit-ready controls, multi-ledger payroll, and deep integrations that lift average contract values. They also buy adjacent learning and analytics, widening the human capital management ERP market share gap versus smaller firms. Yet small and medium enterprises post the faster 13.72% CAGR as simplified onboarding trims IT overhead.

Gusto, BambooHR, and HiBob offer flat-rate bundles that complete go-lives in under 90 days. Workday launched a mid-market edition in 2024, entering the 500-2,500 employee band. SMEs value mobile apps, embedded payments, and hands-off compliance, though many skip succession and learning at first pass, leaving expansion potential. Vendors court this segment because low churn and upsell headroom lift lifetime value across the human capital management ERP market.

Geography Analysis

North America contributed 34.97% of 2025 revenue, driven by strict multi-state payroll laws and early cloud adoption. The IRS cut the W-2 e-file threshold, accelerating migration among mid-sized employers. Growth is plateauing as most enterprises finish first-wave migrations and now purchase AI add-ons rather than full suites.

Asia-Pacific is projected to be the fastest-growing region, with a compound annual growth rate (CAGR) of 13.94% during the forecast period. The implementation of in-country payroll engines has become crucial as Goods and Services Tax (GST) and social insurance reforms introduce additional layers of complexity into payroll management. Australia and New Zealand demonstrate high levels of cloud adoption, whereas Indonesia and Vietnam are experiencing slower progress due to persistent infrastructure challenges.

Europe's trajectory is compliance-driven, as the GDPR requires local data processing and the Posted Workers Directive requires payroll recalculations. Vendors run regional data centers in Germany, the Netherlands, and Ireland. Eastern Europe benefits as shared-services hubs grow in Poland and Romania. The Middle East is expanding under Saudi Vision 2030 workforce reforms, whereas Africa remains nascent outside South Africa and Egypt.

- Workday Inc.

- Ultimate Kronos Group, Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- Bamboo HR LLC

- Namely Inc.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- PeopleStrategy, Inc.

- Gusto, Inc.

- TriNet Zenefits LLC

- HiBob Ltd.

- The Sage Group plc

- Epicor Software Corporation

- Unit4 N.V.

- Infor (US), Inc.

- Softworks Workforce Management Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Transition to Cloud-Native HR Suites

- 4.2.2 Demand for Analytics-Driven Workforce Planning

- 4.2.3 Compliance Complexity in Multi-Country Payroll

- 4.2.4 Rise of Remote and Hybrid Work Models

- 4.2.5 AI-Powered Talent Acquisition and Retention Tools

- 4.2.6 Integration of HCM with IoT-Enabled Workforce Safety Systems

- 4.3 Market Restraints

- 4.3.1 High Switching Costs from Legacy ERP

- 4.3.2 Data Privacy and Sovereignty Concerns

- 4.3.3 Implementation Skill Shortage Among HR-IT Staff

- 4.3.4 Vendor Lock-In Fear in Mid-Market Enterprises

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 BFSI

- 5.3.3 Healthcare

- 5.3.4 Retail and E-commerce

- 5.3.5 IT and Telecom

- 5.3.6 Government

- 5.3.7 Other Industry Verticals

- 5.4 By Component

- 5.4.1 Core HR

- 5.4.2 Payroll

- 5.4.3 Talent Management

- 5.4.4 Workforce Management

- 5.4.5 Learning and Development

- 5.4.6 Other Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Ultimate Kronos Group, Inc.

- 6.4.3 Ceridian HCM Holding Inc.

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Bamboo HR LLC

- 6.4.9 Namely Inc.

- 6.4.10 Zoho Corporation Pvt. Ltd.

- 6.4.11 Ramco Systems Limited

- 6.4.12 PeopleStrategy, Inc.

- 6.4.13 Gusto, Inc.

- 6.4.14 TriNet Zenefits LLC

- 6.4.15 HiBob Ltd.

- 6.4.16 The Sage Group plc

- 6.4.17 Epicor Software Corporation

- 6.4.18 Unit4 N.V.

- 6.4.19 Infor (US), Inc.

- 6.4.20 Softworks Workforce Management Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment