PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065610

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065610

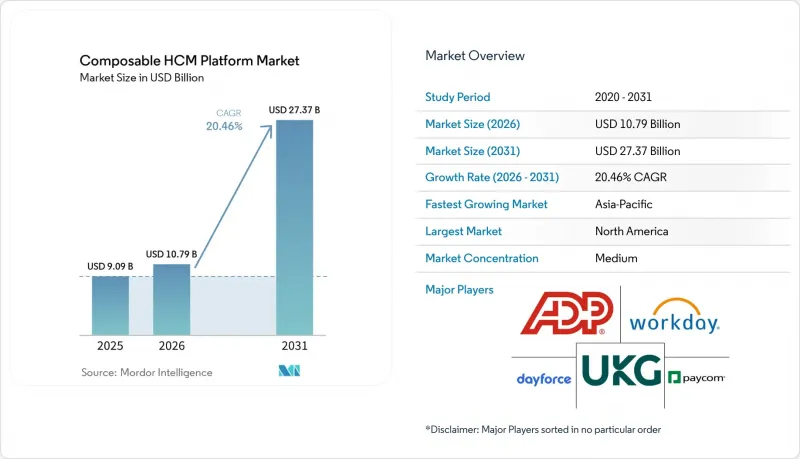

Composable HCM Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the composable HCM platform market size is projected to be USD 9.09 billion in 2025, USD 10.79 billion in 2026, and reach USD 27.37 billion by 2031, growing at a CAGR of 20.46% from 2026 to 2031.

This report is Segmented by Component (Platform Software, and Services), Deployment Model (Cloud-Based, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Functional Module (Core HR & Employee Record Management, and More), End-User Industry Vertical (Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Composable HCM Platform Market Trends and Insights

Shift Toward Cloud-Native Modular HR Architecture

The composable HCM platform market is gaining traction because many enterprises no longer want HR systems that require full platform upgrades whenever one process changes. Older HR stacks often make each policy revision, compliance update, or analytics request more costly because every change touches multiple tightly linked systems. The composable HCM platform market benefits from the spread of microservices, API-first design, cloud-native delivery, and headless application architectures, enabling organizations to replace a single module without disrupting adjacent workflows. Workday moved in this direction in September 2025, when it launched Workday Build, which opened the company's applications, data, and AI infrastructure to customer- and partner-built extensions directly on the platform. SAP SuccessFactors reinforced this direction in its 1H 2026 release by linking AI agents across recruiting, payroll, learning, and workforce administration through a more loosely coupled service model. As more enterprises modernize one module at a time, the cost and disruption of later HR changes tend to decline, strengthening the case for the composable HCM platform market over a longer adoption cycle.

Rising Demand for AI-Driven Workforce Planning And People Analytics

The composable HCM platform market is also being driven by a clear shift from static HR reporting to active workforce decision support. Organizations now want planning tools that can connect labor costs, headcount, skills, and operating outcomes in a single, governed environment rather than across disconnected systems. Workday's general availability launch of Sana in March 2026 showed how leading vendors are building policy-aware AI agents that can complete multi-step HR and finance tasks from a single interface. SAP reported in May 2026 that 62% of C-suite executives were dissatisfied with how people data connects to business performance, indicating a real gap in current enterprise operating models. Demand is rising fastest in scenario planning and labor cost modeling, where companies want to test workforce options before making staffing decisions. Once this planning layer is adopted, the value of unified employee data rises quickly, which keeps the composable HCM platform market closely tied to advances in workforce intelligence.

Data Privacy, AI Governance, and Algorithm Audit Burdens

The composable HCM platform market faces a real constraint due to the governance burden associated with AI-based hiring, performance, and planning tools. Companies now have to document model logic, preserve audit trails, and maintain clear human oversight when automated systems influence employment decisions. This burden is especially strong in Europe, where the EU AI Act classified employment-related AI tools as high-risk applications and set documentation and conformity obligations before market placement. The composable HCM platform market, therefore, moves faster for vendors with mature compliance controls, as they can progress through procurement and legal review with less friction. Newer entrants may still offer strong AI functionality, but many face longer review cycles when buyers test security, governance, and explainability requirements. In regulated industries, governance readiness is becoming an early screening factor, which reduces the number of vendors that reach a detailed functional evaluation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Multi-Country Payroll and Compliance Automation Needs

- Frontline and Distributed Workforce Digitization

- Legacy HR and Payroll Migration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software accounted for 67.42% of revenue in 2025, keeping this part of the composable HCM platform market at the center of buyer spending. Enterprises prioritized the core layer first because API orchestration, low-code configuration, workflow control, and workforce data management determine how well the rest of the system can connect. Spending in this area also reflected a clear preference for integration-capable HR foundations rather than stand-alone point tools that add more interfaces. Within the software layer, core composable HCM platforms and API and integration orchestration platforms remained the most valuable sub-tiers because they set the interoperability ceiling for the full architecture. Marketplace and extensibility platforms also gained more attention as large employers sought pre-built business capabilities that shortened time-to-value across specific HR use cases.

Services remained smaller in 2025, but they are projected to grow at a 20.66% CAGR through 2031, indicating that the composable HCM platform industry is expanding beyond license revenue alone. The composable HCM platform market tends to drive greater service demand as implementations expand into a broader set of workflows and require more configuration support than internal HR teams can sustain. This pattern matters because implementation, advisory, and managed services often continue long after the initial software deployment. Workflow automation and process orchestration are helping expand this need since organizations increasingly want approval chains, compliance actions, and data flows configured without constant developer involvement. Over time, the revenue balance may still favor platform software, but service income should remain an important part of how vendors and partners participate in the composable HCM platform market.

Cloud-based deployment accounted for 72.18% of revenue in 2025, making it the leading model in the composable HCM platform market. Buyers favored subscription-based infrastructure because it reduces capital spending and aligns upgrade cycles with vendor release schedules. Cloud adoption also aligned well with the market's modular design logic, since new components are easier to connect when vendors maintain a more consistent update rhythm. At the same time, on-premises deployment still has relevance in government, defense, and critical infrastructure environments where employee data and payroll processing are tightly controlled. These exceptions kept deployment choice tied to regulatory context rather than to architecture preference alone.

Hybrid deployment is projected to expand at a 21.47% CAGR through 2031, which makes it the fastest-growing model in the composable HCM platform market. Many enterprises prefer a phased approach in which regulated data remains on-premises while analytics, collaboration, and extensibility layers move to the cloud first. This pattern is especially relevant in Europe and the Asia-Pacific region, where country-specific residency rules can slow a full shift to public cloud. The composable HCM platform market is therefore not moving in a straight line from on-premises to the cloud, because hybrid structures offer a practical bridge for organizations dealing with migration risk and compliance constraints. As regional cloud infrastructure deepens, some hybrid users will move further toward cloud-only delivery, but hybrid should remain a durable choice through the forecast period.

Geography Analysis

North America accounted for 39.86% of the composable HCM platform market in 2025, making it the largest regional segment. The United States accounted for most of that demand because enterprises there were early adopters of API-first HR architecture and had a dense vendor ecosystem to support multi-module deployment. Large organizations in technology, financial services, and healthcare continued to connect core HR, payroll, analytics, and talent management within unified data structures, keeping the composable HCM platform market firmly anchored in the region. Canada gained momentum from growing interest in multi-provincial compliance automation, while Mexico saw demand driven by workforce digitization in manufacturing and distribution environments. This regional lead also reflected stronger cloud infrastructure penetration and greater willingness among enterprises to move away from legacy HR cores.

Asia-Pacific is projected to expand at a 24.89% CAGR through 2031, which makes it the fastest-growing geography in the composable HCM platform market. Growth is coming from rapid SME digitization in India and Southeast Asia, multi-country payroll modernization in Japan, South Korea, and Australia, and rising healthcare platform investment across the region. China remains important, but its path is shaped by localization rules that favor architectures with regional cloud deployment options. India is also seeing demand from technology services exporters and global capability centers that manage distributed workforces, while labor-intensive sectors are moving toward more connected HR operations. Tech Mahindra's May 2026 partnership with UKG showed how APAC-based service and technology capabilities are increasingly influencing deployment patterns well beyond the region.

Europe is moving through a more compliance-driven expansion in the composable HCM platform market, with the June 7, 2026, transposition deadline under the EU Pay Transparency Directive pushing employers toward better job architecture and pay data infrastructure. Germany, the United Kingdom, France, the Netherlands, and the Nordic countries remain the main demand centers because they combine enterprise scale with stricter expectations around governed workforce data. South America is still an emerging geography, but Brazil stands out because its large enterprise base and complex payroll obligations create strong demand for compliance-linked payroll automation. The Middle East is also expanding, led by Saudi Arabia and the United Arab Emirates, where workforce nationalization programs are increasing the need for detailed workforce composition reporting. Africa remains at an earlier stage, but South Africa and Nigeria are moving faster as payroll complexity and multi-jurisdiction compliance needs create clearer use cases for modular HR infrastructure.

- Automatic Data Processing, Inc.

- Bamboo HR LLC

- Cegid Group

- Cornerstone OnDemand, Inc.

- Darwinbox Digital Solutions Private Limited

- Dayforce, Inc.

- Deel Inc.

- Sage People

- Lattice

- Hi Bob, Inc.

- isolved, inc.

- Paychex, Inc.

- Paycom Software, Inc.

- Paycor HCM, Inc.

- Paylocity Holding Corporation

- Personio SE and Co. KG

- Remote Technology, Inc.

- Rippling People Center Inc.

- UKG Inc.

- Workday, Inc.

- Zellis UK Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Shift Toward Cloud-Native Modular HR Architecture

- 4.3.2 Rising Demand for AI-Driven Workforce Planning and People Analytics

- 4.3.3 Expansion of Multi-Country Payroll and Compliance Automation Needs

- 4.3.4 Frontline and Distributed Workforce Digitization

- 4.3.5 EU Pay Transparency Readiness and Pay Equity Reporting

- 4.3.6 Low-Code Marketplace Extensions and Packaged HR Capabilities

- 4.4 Market Restraints

- 4.4.1 Data Privacy, AI Governance, and Algorithm Audit Burdens

- 4.4.2 Legacy HR and Payroll Migration Complexity

- 4.4.3 Suite Vendor Marketplace Lock-In Risk

- 4.4.4 Country-Level Payroll and Benefits Rule Fragmentation

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform Software

- 5.1.1.1 Core Composable HCM Platforms

- 5.1.1.2 API and Integration Orchestration Platforms

- 5.1.1.3 Workflow Automation and Process Orchestration Engines

- 5.1.1.4 Low-code/No-code HR Configuration Platforms

- 5.1.1.5 Workforce Data Fabric and Intelligence Platforms

- 5.1.1.6 Marketplace and Extensibility Platforms

- 5.1.2 Services

- 5.1.1 Platform Software

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Functional Module

- 5.4.1 Core HR and Employee Record Management

- 5.4.2 Payroll, Compensation and Benefits

- 5.4.3 Talent Acquisition and Recruiting

- 5.4.4 Talent Management and Internal Mobility

- 5.4.5 Workforce Management and Labor Optimization

- 5.4.6 Learning and Workforce Development

- 5.4.7 Workforce Intelligence, Analytics and Planning

- 5.4.8 Employee Experience, HR Service Delivery and Workflow Automation

- 5.4.9 Integration and Workflow Orchestration

- 5.4.10 Workforce Data Fabric and Employee Identity Management

- 5.5 By End user Industry Vertical

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Bamboo HR LLC

- 6.4.3 Cegid Group

- 6.4.4 Cornerstone OnDemand, Inc.

- 6.4.5 Darwinbox Digital Solutions Private Limited

- 6.4.6 Dayforce, Inc.

- 6.4.7 Deel Inc.

- 6.4.8 Sage People

- 6.4.9 Lattice

- 6.4.10 Hi Bob, Inc.

- 6.4.11 isolved, inc.

- 6.4.12 Paychex, Inc.

- 6.4.13 Paycom Software, Inc.

- 6.4.14 Paycor HCM, Inc.

- 6.4.15 Paylocity Holding Corporation

- 6.4.16 Personio SE and Co. KG

- 6.4.17 Remote Technology, Inc.

- 6.4.18 Rippling People Center Inc.

- 6.4.19 UKG Inc.

- 6.4.20 Workday, Inc.

- 6.4.21 Zellis UK Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment