PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063944

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063944

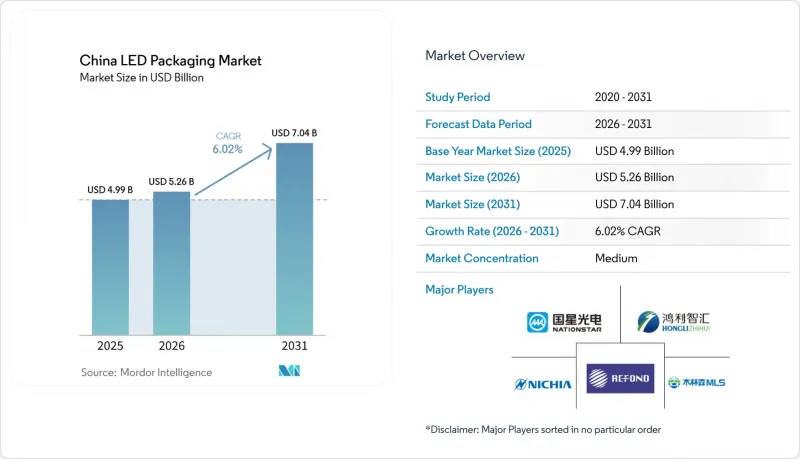

China LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china lED packaging market size is projected to be USD 4.99 billion in 2025, USD 5.26 billion in 2026, and reach USD 7.04 billion by 2031, growing at a CAGR of 6.02% from 2026 to 2031.

This report is Segmented by Packaging Architecture (Chip-On-Board (COB), and More), Power Class (Mid Power (0. 5-1 W), High Power (1-3 W), and More), Emission Type (Visible LED Packages, Infrared (IR) LED Packages, and More), Material Chemistry (Encapsulation, and More), Application (General Lighting, Automotive Lighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China LED Packaging Market Trends and Insights

Government-Backed Smart-City LED Retrofits

Municipal procurement programs are replacing legacy streetlights with networked LED luminaires that integrate dimming, sensors, and remote diagnostics. Projects such as the 79 000-unit retrofit completed in Tianjin's Binhai New Area in 2024 cut energy use by 40%, proving the case for mid- to high-power chip-on-board modules. Tender documents increasingly require compliance with GB 7000.1-2024 safety rules and domestic-content thresholds, directing contract awards to Chinese packagers that can certify interoperability with national IoT standards. Because smart-streetlight controllers collect telemetry, suppliers with robust analytics platforms gain recurring service revenue. This shift toward performance-based contracts strengthens the grip of vertically integrated players that maintain in-house driver electronics and field-failure diagnostics.

Accelerating Mini/Micro-LED Backlighting Adoption

China shipped more than 8 million mini-LED televisions in 2025, and volumes are forecast to top 10 million units in 2026 as retail prices for 100-inch panels fall below CNY 10 000 (USD 1 385). Flagship sets such as Hisense's 116-inch RGB mini-LED achieve 97% BT.2020 coverage and 10 000-nit peaks by tripling die counts per panel, massively expanding demand for chip-scale packages. Placement tolerances tighter than 50 µm and yield targets above 99.9% elevate the barrier to entry, prompting long-term supply tie-ups between BOE, China Star Optoelectronics, and domestic packagers. Korean and Japanese competitors now face a 50% price disadvantage on comparable specifications, spurring them to accelerate their own RGB micro-LED roadmaps.

Price Erosion from Excess Mid-Power Capacity

March 2026 list-price hikes of 3%-25% announced by leading packagers were quickly undercut in Zhejiang, where defect rates in budget lines still hover near 15% and equipment utilization lags the 85% break-even threshold. Combined industry revenue grew 8.9% in 2024, yet profit expansion was confined to firms with automotive or mini-LED focus, highlighting the fragility of commodity pricing. Revenue at MLS and NationStar declined in the first half of 2025, even as niche players Refond and Jufei posted double-digit growth, confirming the structural oversupply in mid-power formats. Until plant closures or demand growth absorb this overhang, margin compression will persist, discouraging fresh investment in SMD lines.

Other drivers and restraints analyzed in the detailed report include:

- Automotive LED Penetration in NEVs

- Export-Oriented EMS Demand for SMD Packages

- Dependence on Imported High-Performance Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale packages are projected to expand at a 6.78% CAGR through 2031 as television makers move from white backlights to RGB mini-LED engines that need higher die density and tighter placement tolerances. Surface-mount device formats still held 42.78% of the China LED packaging market share in 2025, as decades of automation have driven defect rates below 2% and pushed unit pricing to under USD 0.10 for 10 000-piece orders.

High-volume 2835, 3030, and 5050 footprints remain indispensable in residential lamps, yet flip-chip devices without wire bonds now dominate high-current automotive modules that need superior heat dissipation. Glass-substrate mass-transfer lines under construction in Tianmen aim for 99.995% transfer yields, a threshold that could unlock cost-effective micro-LED wearables and automotive displays.

In 2025, mid-power LEDs, rated between 0.5-1 W, accounted for 35.49% of total revenue. However, due to a persistent oversupply, these LEDs are grappling with single-digit gross margins. On the other hand, high-power packages, rated between 1-3 W, are witnessing a growth rate of 6.94% CAGR. This surge is largely attributed to their adoption in adaptive driving-beam headlights and industrial high-bay luminaires, both of which are known to reduce fixture counts and maintenance labor.

Indicator-class emitters with power levels below 0.5 W play a dominant role in the wearables and signage markets. However, the extremely narrow profit margins in these segments significantly constrain opportunities for reinvestment and further development. At the top end, copper-substrate emitters above 3 W now target horticultural grow lights and stadium floodlamps that absorb the 30%-50% price premium in exchange for higher lumen density and long L70 life.

List of Companies Covered in this Report:

- MLS Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- Hongli Zhihui Group Co. Ltd.

- Refond Optoelectronics Co. Ltd.

- Jufei Optoelectronics Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- Nichia Corporation

- ams OSRAM AG

- Samsung Electronics Co. Ltd. (Samsung LED)

- Seoul Semiconductor Co. Ltd.

- Lumileds Holding B.V.

- Everlight Electronics Co. Ltd.

- Bridgelux Inc.

- Citizen Electronics Co. Ltd.

- Cree LED

- Epistar Corporation

- Foshan NationStar Optoelectronics

- Lite-On Technology Corporation

- TongYiFang Optoelectronics

- Ledteen Lighting Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Backed Smart-City LED Retrofits

- 4.2.2 Accelerating Mini / Micro-LED Backlighting Adoption

- 4.2.3 Automotive LED Penetration in NEVs

- 4.2.4 Export-Oriented EMS Demand for SMD Packages

- 4.2.5 Vertical Integration by Chinese LED Champions

- 4.2.6 Mass-Transfer Glass Substrate Packaging Breakthroughs

- 4.3 Market Restraints

- 4.3.1 Price Erosion from Excess Mid-Power Capacity

- 4.3.2 Dependence on Imported High-Performance Phosphors

- 4.3.3 Labor-Cost Inflation in Coastal Clusters

- 4.3.4 Recycling And E-Waste Compliance Costs

- 4.4 Industry Value-Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-line Package (DIP / Through-hole)

- 5.1.6 Other Packaging Architectures (IMD, GOB, Mini-LED Display Packaging)

- 5.2 By Power Class

- 5.2.1 Low Power (Below 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (1-3 W)

- 5.2.4 Ultra-High Power (Above 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared (IR) LED Packages

- 5.3.3 Ultraviolet (UV) LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display And Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share, Products and Services, Recent Developments)

- 6.4.1 MLS Co. Ltd.

- 6.4.2 NationStar Optoelectronics Co. Ltd.

- 6.4.3 Hongli Zhihui Group Co. Ltd.

- 6.4.4 Refond Optoelectronics Co. Ltd.

- 6.4.5 Jufei Optoelectronics Co. Ltd.

- 6.4.6 San'an Optoelectronics Co. Ltd.

- 6.4.7 Nichia Corporation

- 6.4.8 ams OSRAM AG

- 6.4.9 Samsung Electronics Co. Ltd. (Samsung LED)

- 6.4.10 Seoul Semiconductor Co. Ltd.

- 6.4.11 Lumileds Holding B.V.

- 6.4.12 Everlight Electronics Co. Ltd.

- 6.4.13 Bridgelux Inc.

- 6.4.14 Citizen Electronics Co. Ltd.

- 6.4.15 Cree LED

- 6.4.16 Epistar Corporation

- 6.4.17 Foshan NationStar Optoelectronics

- 6.4.18 Lite-On Technology Corporation

- 6.4.19 TongYiFang Optoelectronics

- 6.4.20 Ledteen Lighting Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment