PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066434

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066434

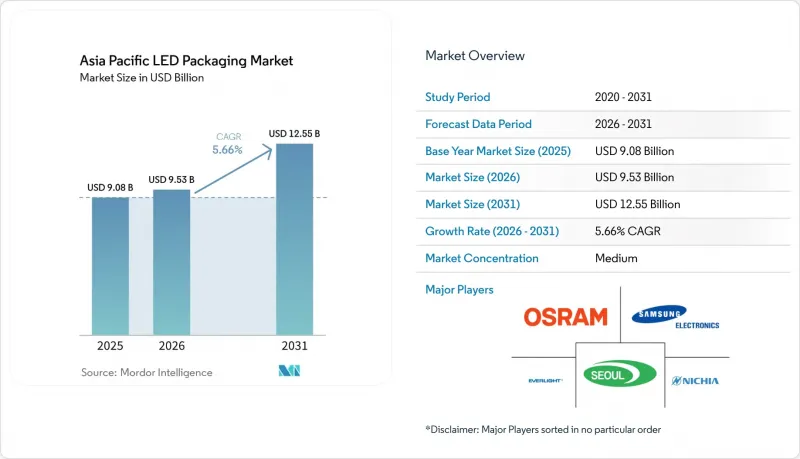

Asia Pacific LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia pacific lED packaging market size is expected to grow from USD 9.08 billion in 2025 to USD 9.53 billion in 2026 and is forecast to reach USD 12.55 billion by 2031 at a 5.66% CAGR over 2026-2031.

This report is Segmented by Packaging Architecture (Surface Mount Device, Chip-On-Board, and More), Power Class (Low Power, and More), Emission Type (Visible LED Packages, and More), Material Chemistry (Substrates, Encapsulation, Bonding and Die-Attach, and More), Application (General Lighting, Automotive Lighting, and More), and Geography. The Market Forecasts are Provided in USD.

Asia Pacific LED Packaging Market Trends and Insights

Rapid Adoption of Mini-LED and Micro-LED Backlighting

Television makers accelerated Mini LED penetration to roughly 10% of regional shipments in 2026, as energy-efficiency subsidies in China reward Level-1-compliant sets. Samsung introduced six Micro RGB TV sizes that eliminate color filters and deliver full BT.2020 gamut certification, reinforcing the move toward chip-level integration. Automakers from Xiaomi to BMW are committed to Mini LED cockpit displays that exceed 4,000 nits, expanding demand for high-brightness packages that manage elevated junction temperatures. The shift favors chip-on-board and glass-substrate modules, prompting panel makers to internalize packaging and forcing independent vendors to specialize in high-yield mass-transfer equipment. Micro LED revenue doubled to USD 105.4 million in 2026, and near-eye AR shipments are projected at 21 million units by 2030, setting the stage for sustained packaging innovation.

Government Energy-Efficiency Mandates Boosting LED Uptake

China's March 2026 standard widened coverage to spotlight, high-bay luminaires, and smart products with a 0.5-watt standby limit, tightening efficacy baselines across commercial construction. Japan mandated 100 % LED road lighting on national highways by 2030 to meet decarbonization goals. India's Production-Linked Incentive scheme unlocked INR 10 478 crore (USD 1.26 billion) for localization, aiming to lift domestic value addition to 75-80%. Divergent testing protocols between Asia and Europe compel exporters to dual-qualify products, spurring demand for chip-on-board packages that surpass 150 lumens-per-watt.

High Initial CapEx for Advanced Packaging Equipment

C Sun invested NT 1.48 billion (USD 46.9 million) in a new Taichung site for AI-driven advanced packaging tools, underlining the steep outlay required for +-1 µm Micro LED placement accuracy. Wuxi NOVO's Thailand branch supports regional customers with Mini LED backlight automation, yet even contract assembly now demands proprietary robotics that many small companies cannot finance. NationStar plans CNY 970.1 million (USD 116.4 million) in six Mini and Micro LED projects, with payback periods of 7 to 8 years, discouraging late entrants. These economics channel new capacity toward large conglomerates or joint ventures that can amortize tooling over multiple product lines.

Other drivers and restraints analyzed in the detailed report include:

- Declining ASP of LED Packages Through Economies of Scale

- Rising Automotive LED Penetration in Headlamps and ADAS

- Thermal Management Challenges in High-Power Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface Mount Device packages accounted for 43.74% of the Asia Pacific LED packaging market size in 2025, sustaining dominance in general illumination fixtures and edge-lit displays. Chip Scale Package revenue is advancing at a 6.28% CAGR through 2031 as flip-chip designs eliminate ceramic submounts, trim the bill of materials, and reduce thermal resistance. Panel makers in China increasingly deploy chip-on-board Mini LED bars in 75-inch-plus televisions, compressing the supply chain and shifting profit pools away from independent packagers. Japanese and Korean automotive suppliers favor flip-chip layouts that simplify automated optical inspection and support per-LED current sensing, a prerequisite for AEC-qualified headlamps.

Continued CSP cost erosion stems from high wafer-level throughput and fewer assembly steps, yet reliability under sulfur exposure and high humidity remains a concern for outdoor signage. SMD producers are responding with epoxy-mold-compound upgrades and secondary optics, but price gaps persist. The Asia Pacific LED packaging industry now observes a dual-track model: commodity SMD lines run at hyperscale in the Pearl River Delta, whereas CSP lines co-located with driver back-end flow in Jiangsu and Taiwan focus on performance-critical segments. Suppliers lacking advanced mass-transfer or flip-chip expertise face shrinking addressable markets as display and automotive verticals internalize packaging.

Mid-power parts ranging from 0.5-1 W captured 39.38% of Asia Pacific LED packaging market share in 2025. High-power components above 1 W are growing faster at 6.21% CAGR as adaptive-beam headlamps demand robust lumen density. Thermal-via optimization allows select mid-power footprints to encroach on indoor high-bay niches; however, automotive specifications still require ceramic or metal-core substrates that withstand -40 °C to 125 °C cycles.

Ultra-high-power arrays above 3 W address sports arenas and horticulture greenhouses where fixture count must be minimized. OEMs weigh single high-power emitters against clustered mid-power assemblies: clusters lower thermal hotspots but increase driver channel count and optical alignment complexity. Suppliers that span the full power spectrum hedge against these architecture choices and lock in volume regardless of OEM design selection.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd. (Samsung LED)

- Osram GmbH (OSRAM Opto Semiconductors)

- Seoul Semiconductor Co., Ltd.

- Everlight Electronics Co., Ltd.

- Cree LED, Inc.

- LG Innotek Co., Ltd.

- Lumileds Holding B.V.

- Guangzhou Nationstar Optoelectronics Co., Ltd.

- Shenzhen Hongli Zhihui Group Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- Lextar Electronics Corp.

- Dominant Opto Technologies Sdn. Bhd.

- Opto Tech Corporation

- Refond Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Advanced Optoelectronic Technology, Inc.

- Bridgelux, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Mini-LED and Micro-LED Backlighting

- 4.2.2 Government Energy-Efficiency Mandates Boosting LED Uptake

- 4.2.3 Declining ASP of LED Packages Through Economies of Scale

- 4.2.4 Rising Automotive LED Penetration in Headlamps and ADAS

- 4.2.5 Localization Incentives for Advanced Packaging Lines in China and India

- 4.2.6 Emergence of Flip-Chip CSP for Horticulture Lighting Customisation

- 4.3 Market Restraints

- 4.3.1 High Initial CapEx for Advanced Packaging Equipment

- 4.3.2 Thermal Management Challenges in High-Power Packages

- 4.3.3 Phosphor Supply Constraints from Rare-Earth Bottlenecks

- 4.3.4 Patent Expiry Cliff Creating Pricing Pressures

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-line Package (DIP / Through-hole)

- 5.1.6 Others, Packaging Architecture

- 5.2 By Power Class

- 5.2.1 Low Power (Less than 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (1-3 W)

- 5.2.4 Ultra-High Power (More than 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared LED Packages

- 5.3.3 Ultraviolet LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display and Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

- 5.6 By Geography

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 Southeast Asia

- 5.6.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Samsung LED)

- 6.4.3 Osram GmbH (OSRAM Opto Semiconductors)

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Everlight Electronics Co., Ltd.

- 6.4.6 Cree LED, Inc.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Lumileds Holding B.V.

- 6.4.9 Guangzhou Nationstar Optoelectronics Co., Ltd.

- 6.4.10 Shenzhen Hongli Zhihui Group Co., Ltd.

- 6.4.11 Sanan Optoelectronics Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 Lextar Electronics Corp.

- 6.4.15 Dominant Opto Technologies Sdn. Bhd.

- 6.4.16 Opto Tech Corporation

- 6.4.17 Refond Optoelectronics Co., Ltd.

- 6.4.18 MLS Co., Ltd. (Forest Lighting)

- 6.4.19 Advanced Optoelectronic Technology, Inc.

- 6.4.20 Bridgelux, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment