PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063977

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063977

Asia-Pacific Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

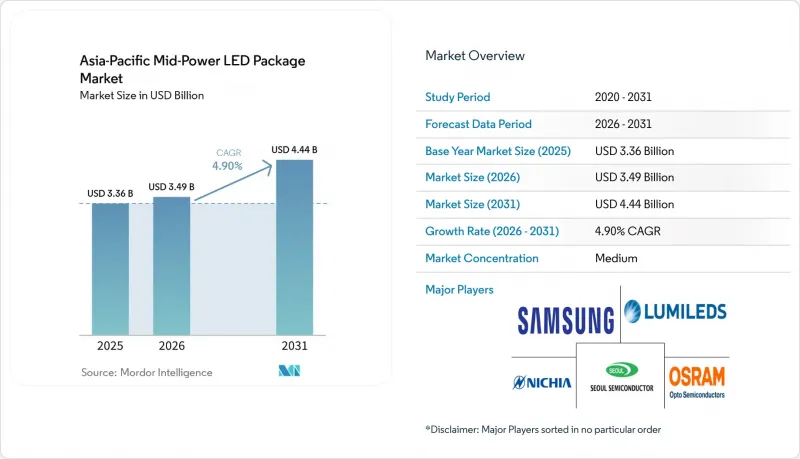

According to Mordor Intelligence, the asia-Pacific mid-power LED package market size is expected to grow from USD 3.36 billion in 2025 to USD 3.49 billion in 2026 and is forecast to reach USD 4.44 billion by 2031 at a 4.9% CAGR over 2026-2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Country (China, Japan, India, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Mid-Power LED Package Market Trends and Insights

Surging Demand for 2835 Mid-Power LEDs in Smart Lighting

Building owners now specify 2835 packages that integrate thermistors and deep-dimming control, eliminating visible flicker and aligning with wellness codes. The 2.8 mm X 3.5 mm footprint allows up to 240 LEDs per meter on flexible strips without breaching thermal limits, creating uniform luminance in retail coves and healthcare wards. Predictive maintenance algorithms tap real-time temperature data to reduce facility operating costs by up to 20%. Adoption accelerates where California Title 24, Singapore's Green Mark, and Japan's WELL certification require low-flicker luminaires. As a result, the Asia-Pacific mid-power LED package market increasingly treats the 2835 as a smart-node platform rather than a low-cost commodity.

Automotive OEM Shift Toward Adaptive Pixel Headlamps

Regulators endorse glare-free high beams, prompting carmakers to embrace 25,000-pixel modules that deliver dynamic beam shaping and road-surface projections. Only suppliers with sub-80 µm pixel pitch and the ability to dissipate 60 watts in a 5 mm X 5 mm envelope qualify, narrowing the vendor pool. Energy savings of 15-20% compared with older matrix lamps translate into extra driving range, an argument that resonates with electric-vehicle buyers across China and Japan. The Asia-Pacific mid-power LED package market thus sees automotive share rising as headlamps evolve from illumination to communication devices.

IP Litigation Risk from Dominant Patent Holders

Patent portfolios have become the chief competitive moat. Recent lawsuits in U.S. and German courts underscore that smaller vendors face a binary choice: accept performance trade-offs to avoid infringement, or risk injunctions that stall automotive qualification cycles lasting 3 years. The overhang forces OEMs to favor suppliers offering indemnification backed by royalty pools, thereby concentrating share within the Asia-Pacific mid-power LED package market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Mini-LED Backlighting Adoption in TV Panels

- Energy-Efficiency Mandates Across Southeast Asia

- Supply Chain Disruptions for Key Phosphor Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Higher-wattage 0.5W- and Less Than 1W packages dominate the Asia-Pacific mid-power LED package market for vehicle headlamps and horticultural rigs. Pixel beams need 0.7-0.9 W chips to sustain 300-meter reach under -40 °C to 125 °C cycles, while vertical farms drive greater than 1,000 µmol m-2 s-1 photon flux with fewer fixtures. Gross margins hover near 30% thanks to stringent binning and AEC-Q-grade reliability. Lower 0.2-0.5 W devices still feed strip lights and mini-LED panels, yet price wars compress margins below 12%, nudging vendors toward premium wattages. The Asia-Pacific mid-power LED package market share in the high-power range thus rises despite smaller unit volumes.

Commodity segments lean on incremental efficacy gains and aggressive cost downs to stay relevant. Retail cove lights pack 0.3 W 2835s at densities of 120-160 LEDs per meter, where lumen per dollar rules procurement. Display backlights adopt similar power envelopes, but panel-maker vertical integration now dictates vendor selection, leaving independents with reduced bargaining power inside the Asia-Pacific mid-power LED package market.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd. (Samsung LED)

- Lumileds Holding B.V.

- ams-OSRAM AG

- Seoul Semiconductor Co., Ltd.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED, an SGH company

- NationStar Optoelectronics Co., Ltd.

- Lite-On Technology Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Toyoda Gosei Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Lextar Electronics Corporation

- Hongli Zhihui Group Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Hubei NationStar Semiconductor

- Shenzhen Jufei Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Regulatory Landscape

- 4.4 Technology Analysis

- 4.5 Market Drivers

- 4.5.1 Surging Demand for 2835 Mid-Power LEDs in Smart Lighting

- 4.5.2 Automotive OEM Shift Toward Adaptive Pixel Headlamps

- 4.5.3 Accelerated Mini-LED Backlighting Adoption in TV Panels

- 4.5.4 Energy-Efficiency Mandates Across Southeast Asia

- 4.5.5 Rapid Expansion of Horticultural Lighting in Controlled-Environment Farms

- 4.5.6 Emerging Micro-Packaging Techniques Reducing Cost per Lumen

- 4.6 Market Restraints

- 4.6.1 IP Litigation Risk From Dominant Patent Holders

- 4.6.2 Supply Chain Disruptions for Key Phosphor Materials

- 4.6.3 Luminance Degradation Under High-Humidity Asian Climates

- 4.6.4 Consolidation of Display Backlight Vendors Dampening ASPs

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Southeast Asia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Samsung LED)

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 ams-OSRAM AG

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Everlight Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Cree LED, an SGH company

- 6.4.9 NationStar Optoelectronics Co., Ltd.

- 6.4.10 Lite-On Technology Corporation

- 6.4.11 Dominant Opto Technologies Sdn. Bhd.

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 San'an Optoelectronics Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 Hongli Zhihui Group Co., Ltd.

- 6.4.16 Refond Optoelectronics Co., Ltd.

- 6.4.17 MLS Co., Ltd. (Forest Lighting)

- 6.4.18 Hubei NationStar Semiconductor

- 6.4.19 Shenzhen Jufei Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment