PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065501

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065501

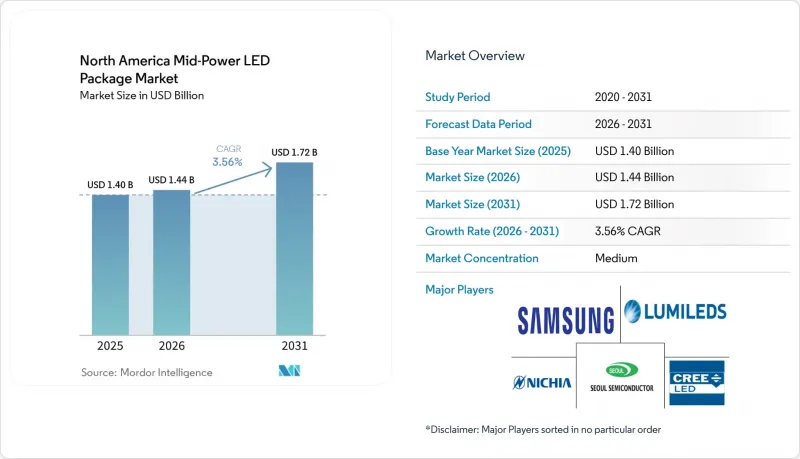

North America Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america mid-power LED package market size is projected to expand from USD 1.40 billion in 2025 and USD 1.44 billion in 2026 to USD 1.72 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Mid-Power LED Package Market Trends and Insights

Standardization of Automotive LED Requirements

Transport Canada TSD 108 Revision 8 became mandatory in October 2025, aligning the photometric and durability rules with U.S. FMVSS 108. Tier-1 suppliers now engineer a single module platform for the continent, and that platform predominantly specifies arrays of 0.5 W to 0.8 W mid-power packages, which spread heat more evenly than sparse high-power clusters. NHTSA's refusal in 2024 to relax adaptive-beam glare thresholds reinforces the need for high-density arrays that maintain uniform luminance across complex optics. SAE J1889 added accelerated thermal-cycling tests in April 2025, favoring lower-junction-temperature mid-power packages. Mexico's February 2026 automotive strategy signals future approvals for matrix and sequential functions, further increasing device count per vehicle. Together, the harmonized requirements expand demand for mid-power LEDs in signal, DRL, and adaptive systems.

Surge In Energy-Efficient Building Codes

California Title 24-2025 lowered lighting power densities by up to 15%, effective January 2026, while IECC 2024 calls for continuous dimming to 10% and broader occupancy sensing in cities that adopted the code in 2026. Oregon's 2026 Residential Specialty Code and New York City's 2025 Energy Conservation Code add similar controls, shortening retrofit paybacks to as little as 12-18 months in high-use spaces. Because mid-power packages integrate seamlessly with legacy constant-current drivers, contractors can reuse wiring and minimize downtime, thereby accelerating project approvals. Utilities in the Midwest and Southeast continue to offer rebates of USD 30-80 per DLC-qualified luminaire, and most of those fixtures use 2835 or 3030 mid-power LEDs. Collectively, stricter codes and rebate economics sustain high retrofit volumes despite plateauing first-wave conversions.

Supply Chain Vulnerability for Phosphor Materials

China's rare-earth export curbs in April and October 2025 placed europium, terbium, and yttrium under license, driving multi-fold price spikes in non-Chinese spot markets. U.S. yttrium imports collapsed from 333 t to 17 t within eight months, and stopgap stockpiles can cover only one to two quarters of LED phosphor demand. A negotiated one-year suspension defers full enforcement to November 2026, yet the episode spotlighted single-source risk, prompting OEMs to request dual-supply certification or non-rare-earth phosphor roadmaps.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost of Mid-Power LED Chips

- Rapid Expansion of Horticulture Lighting in Vertical Farms

- Slow Retrofit Cycle in Commercial Real Estate Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial retrofits and automotive signal lamps together propelled the 0.5 W-to-Less Than 1 W class to a 61.88% share in 2025, the highest in the North America mid-power LED package market. That weight reflects steady gains in efficacy that let designers hit lumen targets with fewer diodes, reducing pick-and-place steps and driver channel counts. Moving to the next forecast period, the same class is forecast to grow at a 3.96% CAGR, outperforming both lower-wattage and near-1 W classes as OEMs converge on this sweet spot for thermal reliability.

Fixture makers migrated from 0.2 W to 0.5 W devices toward the mid-range as Title 24 and IECC constraints tightened, as higher-wattage packages allow slimmer boards and simpler controls. Automotive Tier-1 suppliers enlarged DRL and matrix arrays with 0.6 W-to-0.8 W emitters after SAE revised thermal-cycling tests, confirming reliability under vibration.

List of Companies Covered in this Report:

- Nichia Corporation

- Lumileds Holding B.V.

- Cree LED Inc.

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- OSRAM Opto Semiconductors GmbH

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Lite-On Technology Corporation

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

- Epistar Corporation

- Bridgelux, Inc.

- MLS Co., Ltd.

- Bridgelux, Inc.

- Dominant Opto Technologies Sdn. Bhd.

- Toyoda Gosei Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Standardization of Automotive LED Requirements

- 4.2.2 Surge in Energy-Efficient Building Codes

- 4.2.3 Declining Cost of Mid-Power LED Chips

- 4.2.4 Rapid Expansion of Horticulture Lighting in Vertical Farms

- 4.2.5 Integration of Tunable White LEDs in Human-Centric Lighting

- 4.2.6 Expansion of Utility Rebate Programs Targeting Mid-power LED Fixtures

- 4.3 Market Restraints

- 4.3.1 Price Pressure From Low-Cost Asian Imports

- 4.3.2 Thermal Management Challenges Above 1 W Ceiling

- 4.3.3 Supply Chain Vulnerability For Phosphor Materials

- 4.3.4 Slow Retrofit Cycle in Commercial Real Estate Segment

- 4.4 Industry Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Cree LED Inc.

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 OSRAM Opto Semiconductors GmbH

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Lite-On Technology Corporation

- 6.4.10 Lextar Electronics Corporation

- 6.4.11 NationStar Optoelectronics Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Bridgelux, Inc.

- 6.4.14 MLS Co., Ltd.

- 6.4.15 Bridgelux, Inc.

- 6.4.16 Dominant Opto Technologies Sdn. Bhd.

- 6.4.17 Toyoda Gosei Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment