PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064346

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064346

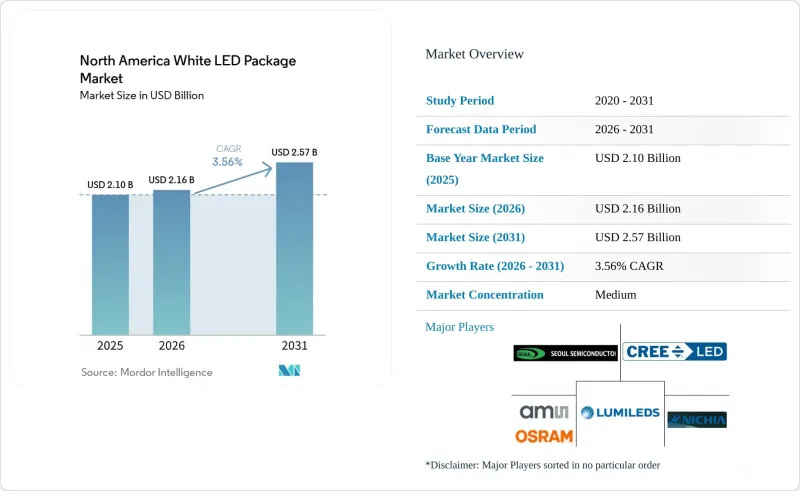

North America White LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america white LED package market size is projected to expand from USD 2.10 billion in 2025 and USD 2.16 billion in 2026 to USD 2.57 billion by 2031, registering a CAGR of 3.56% between 2026 and 2031.

This report is Segmented by Package Architecture (SMD, COB, CSP, and Flip-Chip LED Packages), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America White LED Package Market Trends and Insights

Federal And State Efficiency Mandates Accelerating LED Retrofits

New general-service-lamp rules finalized in 2024 require omnidirectional lamps to reach about 125 lm W-1 at 810 lm output, triggering redesigns of phosphor blends and driver circuits to meet LM-80 and TM-21 lifetime protocols. Parallel mercury-lamp bans across nine states eliminate fluorescent ballast demand, and the Federal Aviation Administration now specifies off-the-shelf LED lamps for runway alignment systems, bringing more than 20 airports into early adoption. Together these actions are shrinking retrofit cycles from seven to four years, lifting volumes of mid-power and high-power packages that satisfy strict lumen-maintenance criteria.

Declining Cost-Per-Lumen And Efficacy Gains

Classic phosphor-converted packages saw manufacturing cost drop 95.5% between 2003 and 2020 as wafer diameters quadrupled and yields tripled. Warm-white device efficiency climbed from 5.8% to 38.8% over the same horizon, leaving spectral efficiency and red-phosphor conversion as the next frontiers. Retail luminaire prices fell 27.3% annually from 2008 to 2020, cutting simple payback to under twelve months for many commercial retrofits, while packaging now dominates per-chip cost, favoring suppliers that integrate precision optics and low-thermal-resistance substrates at scale.

Tariff Volatility And Substrate Supply-Chain Disruptions

Section 301 duties on imported LED chips create unpredictable landed costs, forcing municipal bidders to hold quotes for shorter windows and eroding margins for fixture makers that sell under long-term price agreements. Sapphire wafer supply remains Asia-centric, and any logistics shock quickly ripples into North American packaging lines, lengthening lead times during peak retrofit seasons.

Other drivers and restraints analyzed in the detailed report include:

- Smart-City Infrastructure Investments Boosting High-Power Packages

- Automotive OEM Shift To LED Headlamps And DRLs

- High Capex For Advanced Packaging Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale technology is set to widen its share as automotive forward-lighting designers prioritize low thermal resistance and thinner optics. Surface-mount devices still anchor cost-sensitive general lighting because existing pick-and-place lines handle them without retooling. Flip-chip variants eliminate wire bonds, dropping junction-to-board resistance below 2 °C W-1 and enabling higher drive currents. Chip-on-board remains preferred for track and high-bay luminaires that benefit from high lumen density despite extra assembly steps.

High cross-licensing fees limit new entrants in flip-chip, preserving margins for incumbents. Yet Build America thresholds are nudging suppliers to open U.S. die-attach lines, which may gradually lower unit costs and speed CSP adoption. The North America white LED package market size for chip-scale devices is on course to capture incremental revenue as Tier-1 automotive contracts shift away from wire-bonded arrays. Sustained SMD dominance in retrofit lamps keeps overall architecture diversity balanced.

List of Companies Covered in this Report:

- Cree LED, Inc.

- Lumileds Holding B.V.

- Nichia Corporation

- ams-OSRAM GmbH

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Samsung Electronics Co., Ltd. (LED Division)

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Stanley Electric Co., Ltd.

- Epistar Corporation

- Bridgelux, Inc.

- Luminus Devices, Inc.

- Stanley Electric Co., Ltd.

- Citizen Electronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Market Drivers

- 4.6.1 Federal And State Efficiency Mandates Accelerating LED Retrofits

- 4.6.2 Declining Cost-Per-Lumen And Efficacy Gains

- 4.6.3 Smart-City Infrastructure Investments Boosting High-Power Packages

- 4.6.4 Automotive OEM Shift To LED Headlamps And DRLs

- 4.6.5 Build America, Buy America Sourcing Rules Reshaping Supply Chain

- 4.6.6 Vertical Farming Demand For High-CRI Tunable White Packages

- 4.7 Market Restraints

- 4.7.1 Tariff Volatility And Substrate Supply-Chain Disruptions

- 4.7.2 High Capex For Advanced Packaging Lines

- 4.7.3 Dark-Sky Compliance Ordinances Curbing Outdoor Lumens

- 4.7.4 Patent Cross-Licensing Barriers For Flip-Chip Architectures

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 COB (Chip-on-Board)

- 5.1.3 CSP (Chip Scale Package)

- 5.1.4 Flip-Chip LED Packages

- 5.2 By Power Class

- 5.2.1 Low Power (Less Than 0.5 W)

- 5.2.2 Mid Power (0.5 - 1 W)

- 5.2.3 High Power (Greater Than 1 W)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display And Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cree LED, Inc.

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Nichia Corporation

- 6.4.4 ams-OSRAM GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Samsung Electronics Co., Ltd. (LED Division)

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Citizen Electronics Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Luminus Devices, Inc.

- 6.4.15 Stanley Electric Co., Ltd.

- 6.4.16 Citizen Electronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment