PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063978

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063978

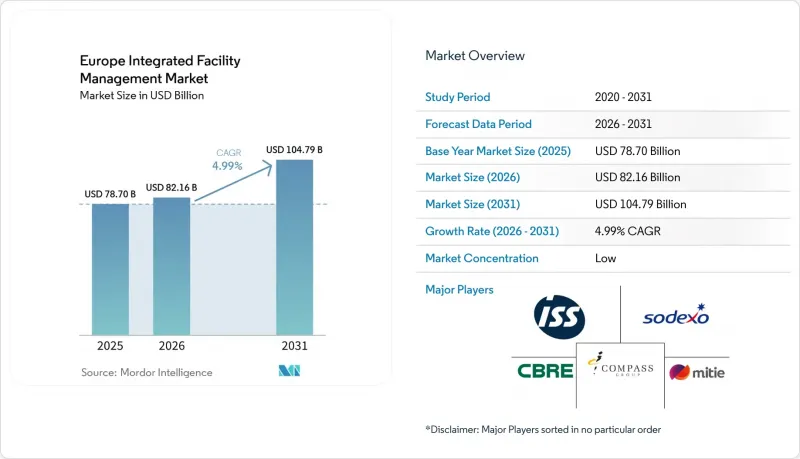

Europe Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe integrated facility management market size is projected to be USD 78.70 billion in 2025, USD 82.16 billion in 2026, and reach USD 104.79 billion by 2031, growing at a CAGR of 4.99% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Healthcare, Hospitality, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Integrated Facility Management Market Trends and Insights

Tightening EU Energy-Efficiency and Decarbonization Mandates

The Europe integrated facility management market is being pulled forward by the recast Energy Performance of Buildings Directive, which entered into force in 2024 and set a firm timetable for national implementation and building upgrades. Non-residential buildings above 290 kW were required to install building automation and control systems by December, 2024, and Member States must transpose the broader directive by May, 2026. The same directive requires the worst-performing 16% of non-residential stock to meet minimum energy performance standards by 2030, and 26% by 2033, which keeps owners focused on staged improvement plans rather than one-time capital work. This matters for integrated operators because compliance now includes monitoring, commissioning, asset documentation, controls management, and coordination of mechanical and electrical upgrades while buildings remain occupied. The public estate is under added pressure because the Energy Efficiency Directive requires annual renovation of a share of public buildings and continued energy reduction efforts across the public sector. As a result, the Europe IFM market is benefiting from a shift toward longer contracts in which one provider is expected to link building performance, day-to-day operations, and compliance reporting under a single framework.

Growing Adoption Of AI-Enabled Predictive Maintenance Platforms

The Europe integrated facility management market is also benefiting from wider use of predictive maintenance tools that turn building telemetry into earlier fault detection and tighter intervention planning. A March 2026 peer-reviewed study in Frontiers in Built Environment validated a hybrid machine-learning framework for HVAC fault detection in non-residential buildings and reported diagnostic accuracy above 99.6% with random forest models trained on air handling unit telemetry. A June 2025 REHVA Journal case from Breda in the Netherlands showed that an AI-driven model predictive control upgrade reduced peak building demand by 28% and lowered peak demand charges by 24% to 30% without major physical intervention. Those results are changing buyer expectations because hard-service contracts are now judged more often on avoided downtime, operating visibility, and energy performance than on the volume of reactive callouts alone. The labor effect is equally important, since connected diagnostics reduce routine inspection workloads while increasing the value of technicians who can interpret data streams and manage connected assets across multiple sites. That shift is widening the capability gap inside the Europe integrated facility management (IFM) market, because larger operators can spread software and analytics costs across national portfolios while smaller firms remain more exposed to manual service models.

Skilled Multi-Trade Technician Shortage and Wage Inflation

The Europe integrated facility management market is facing its most immediate operating constraint in the shortage of technicians who can combine mechanical, electrical, and digital building skills in the same role. The EURES shortage map identified high-severity gaps for air-conditioning and refrigeration mechanics, building electricians, and plumbers across several European labor markets that matter directly to hard-service delivery. DIHK reported for 2025-2026 that 36% of German companies had difficulty filling vacancies and that 63% expected higher labor costs, which points to sustained cost pressure in one of the region's most important operating markets. A September 2025 European Parliament study added that only 1 in 10 heating engineer roles in Germany could be adequately filled through conventional recruitment channels, showing how tight specialist labor has become in building-related trades. Eurostat recorded a 4.7% year-over-year rise in EU construction hourly labor costs in the third quarter of 2025, while the wider business economy rose 3.8%, which illustrates why labor-intensive contracts are becoming harder to price over multiple years. The result is a Europe integrated facility management (IFM) market where providers are accelerating automation, improving workforce planning, and becoming more selective on contracts that combine high technical intensity with weak inflation pass-through.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Outsourcing In Commercial Real Estate Portfolios

- Rise Of Integrated FM In Mission-Critical Data-Center Clusters

- Fragmented EU Regulatory Framework Increasing Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Facility Management (Hard FM) is the faster-growing service category in the Europe integrated facility management market, advancing at a 5.71% CAGR from 2026 to 2031 as compliance work, controls rollout, and aging building systems keep technical demand elevated. The growth is being driven by sustained needs in asset management, MEP services, HVAC, fire systems, and building automation, because regulatory obligations are now tied more closely to operating performance than before. The BACS rollout extends that opportunity further, since the EPBD framework will widen the set of buildings that need more structured technical oversight over the next several years. This is shifting contract value toward lifecycle planning, condition-based maintenance, replacement scheduling, and compliance documentation rather than simple break-fix support. As a result, the Europe integrated facility management industry is leaning more heavily toward technical scopes that can connect energy outcomes, asset uptime, and reporting needs inside one operating model.

Soft Facility Management (Soft FM) remained the largest service segment and held 57.32% of revenue in 2025, which shows how important cleaning, catering, security, and office support still are across every major end-user group. The segment keeps a broad demand base because many occupiers continue to focus on workplace experience, hygiene standards, and day-to-day service continuity even when office footprints are being rationalized. Security-related soft services are also becoming more sensitive as access control, visitor flows, and connected monitoring systems move deeper into digital building environments. That creates a more technical operating layer inside what was once treated mainly as a labor-led service bundle, especially in assets with higher compliance requirements and larger visitor volumes. Even so, the Europe integrated facility management industry still depends on soft services for site coverage and occupant continuity, while pricing remains tighter because many activities are easier for buyers to benchmark and rebid.

List of Companies Covered in this Report:

- ISS A/S

- Sodexo S.A.

- CBRE Group, Inc.

- Compass Group plc

- Mitie Group plc

- Apleona GmbH

- Vinci Facilities

- ENGIE Solutions (Cofely)

- Dussmann Group

- Johnson Controls International plc

- JLL (Jones Lang LaSalle Incorporated)

- Cushman & Wakefield plc

- Allied Universal

- Atlas FM Ltd.

- Aramark Corporation

- SPIE SA

- Serco Group plc

- Bilfinger SE

- Coor Service Management AB

- OKIN Facility, a.s.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening EU Energy-Efficiency and Decarbonization Mandates

- 4.2.2 Growing Adoption of AI-Enabled Predictive Maintenance Platforms

- 4.2.3 Expansion of Outsourcing in Commercial Real Estate Portfolios

- 4.2.4 Digital Twin and IoT Penetration in Aging Building Stock

- 4.2.5 Performance-Linked ESG Financing for Retrofit-Driven Contracts

- 4.2.6 Rise of Integrated FM in Mission-Critical Data-Center Clusters

- 4.3 Market Restraints

- 4.3.1 Skilled Multi-Trade Technician Shortage and Wage Inflation

- 4.3.2 Fragmented EU Regulatory Framework Increasing Compliance Costs

- 4.3.3 Cybersecurity Exposure in Connected Building Systems

- 4.3.4 Margin Pressure from Commoditization of Soft Services

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

- 5.3 By Geographic

- 5.3.1 United Kingdom

- 5.3.2 Germany

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ISS A/S

- 6.4.2 Sodexo S.A.

- 6.4.3 CBRE Group, Inc.

- 6.4.4 Compass Group plc

- 6.4.5 Mitie Group plc

- 6.4.6 Apleona GmbH

- 6.4.7 Vinci Facilities

- 6.4.8 ENGIE Solutions (Cofely)

- 6.4.9 Dussmann Group

- 6.4.10 Johnson Controls International plc

- 6.4.11 JLL (Jones Lang LaSalle Incorporated)

- 6.4.12 Cushman & Wakefield plc

- 6.4.13 Allied Universal

- 6.4.14 Atlas FM Ltd.

- 6.4.15 Aramark Corporation

- 6.4.16 SPIE SA

- 6.4.17 Serco Group plc

- 6.4.18 Bilfinger SE

- 6.4.19 Coor Service Management AB

- 6.4.20 OKIN Facility, a.s.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment