PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064022

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064022

France Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

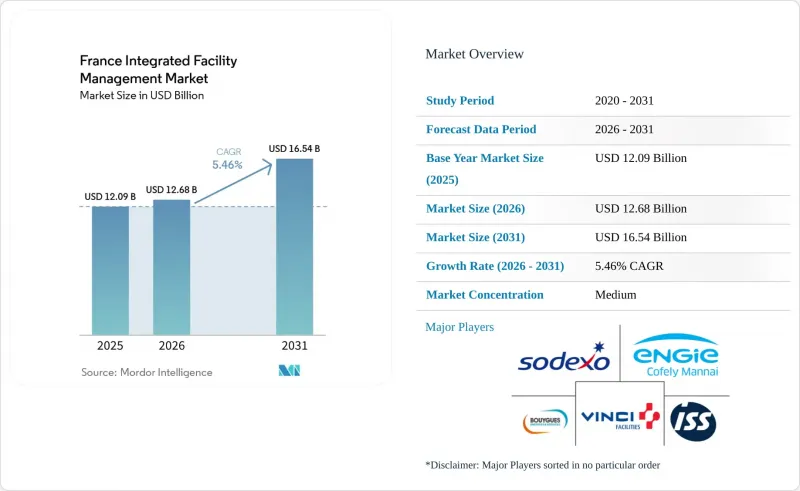

According to Mordor Intelligence, the france integrated facility management market size is expected to increase from USD 12.09 billion in 2025 to USD 12.68 billion in 2026 and reach USD 16.54 billion by 2031, growing at a CAGR of 5.46% over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Integrated Facility Management Market Trends and Insights

Rising Demand for Outsourced Integrated Services in Public Infrastructure

France's public sector owns 90 million m2 of government real estate and manages thousands of municipal and institutional sites that still depend heavily on in-house teams or fragmented contracts. The Tertiary Decree requires 40% energy consumption cuts by 2030 and 50% by 2040 for tertiary buildings above 1,000 m2, with annual OPERAT reporting and penalties that can reach EUR 7,500 (USD 8,475), per legal entity for non-compliance. Those obligations are difficult to manage without centralized monitoring and reporting tools, which is pushing more public buyers toward bundled contracts in the France integrated facility management market. The December 2026 verification milestone against 2030 targets is turning a regulatory requirement into active procurement rather than a long-range planning exercise. Municipal leaders also face public visibility risk when non-compliant buildings appear on official registers, so outsourcing decisions are being shaped by political exposure as well as operating cost pressure in the France integrated facility management (IFM) market.

Accelerating Shift to Performance-Based Contracts in Healthcare Facilities

French hospitals are moving away from legacy P1-P2-P3 maintenance structures and toward Marche Public Global de Performance contracts that combine technical services with energy guarantees. A 2025 tender at CHU de Nice, Hopital Pasteur covered HVAC, electrical, and fire systems under a EUR 30 million contract (USD 33.9 million), with energy and environmental performance carrying 15% of award criteria. In January 2026, Centre Hospitalier de Martigues awarded a 108-month energy performance contract worth EUR 7,464,341 (USD 8.4 million), to Equans Services Batiments and Infrastructures. The CPOM framework continues to reinforce budget discipline across EHPADs and other healthcare settings, which supports longer and more integrated service models in the France integrated facility management market. Providers that can contractually guarantee savings instead of offering only best-effort maintenance are likely to secure longer tenures and better retention in the France IFM market.

Structural HVAC And MEP Skills Shortage Constraining Hard FM Delivery

The France integrated facility management market faces a structural mismatch in technical labor because the sector needs 15,000 new CVC technicians each year while training programs produce only 8,000 graduates. That leaves a yearly deficit of 7,000 profiles before accounting for retirements, and nearly 30% of active CVC technicians are already older than 55 years. The problem is becoming more acute because BACS compliance and low-GWP refrigerant rules now require digital controls knowledge, protocol familiarity, and updated F-Gaz certification. Hard FM providers are therefore being asked to guarantee energy and uptime outcomes while facing higher hiring costs and tighter staffing availability in the France IFM market. Early investment in remote diagnostics and AI-assisted monitoring is becoming a practical response because it reduces technician intensity per site and helps providers protect contract delivery capacity.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Smart Buildings Enabling Predictive FM Via IoT Sensors

- Heightened Regulatory Pressure on Energy Efficiency Targets

- Escalating Public Sector Payroll Costs From CNRACL Employer Contribution Increases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management held 64.61% of the France integrated facility management market share in 2025, which reflects the scale of cleaning, catering, security, reception, and office support demand across institutional, healthcare, and corporate sites. The France IFM market has continued to favor Soft FM because post-pandemic hygiene protocols remain embedded in-service specifications across many client categories. Flexible workspace expansion also widened the addressable base for bundled soft services, with more than 1.4 million m2 of flex office space in France in 2026 and 850,000 m2 located in Ile-de-France. Operated office models are also changing service content because a single provider may now deliver reception, cleaning, catering, and workplace coordination under an all-inclusive operating model. Security and pest control remain smaller lines within Soft FM, but they are gaining scope as clients with longer operating hours ask for constant monitoring and higher service continuity.

Hard facility management is projected to expand at 6.22% CAGR, representing the fastest France integrated facility management (IFM) market size growth by service type through 2031. The France integrated facility management industry is seeing this acceleration because the BACS Decree, the Tertiary Decree, and the 2026 RE2020 expansion all require deeper technical delivery than a soft-only model can provide. The 2024 OPERAT assessment showed that many obligated companies were still behind the path needed for the 2030 target, which keeps retrofit urgency high and shortens conversion timelines for multi-technical contracts. Providers with in-house MEP engineering, sensor deployment capability, and reporting competence are better placed to win this work because clients increasingly want one provider to install, maintain, measure, and report. The result is that complexity-weighted demand is rising faster than volume-led demand, which is gradually changing service mix across the France IFM market.

List of Companies Covered in this Report:

- VINCI Facilities

- ENGIE Cofely

- Sodexo S.A.

- ISS A/S

- Bouygues Energies & Services

- Atalian Global Services

- Derichebourg Multiservices

- Elior Group

- Samsic Facility

- Apleona GmbH

- Dalkia Groupe EDF

- CBRE Group Inc.

- Compass Group plc

- Serco Group plc

- JLL Integrated Facilities Management

- Cushman & Wakefield plc

- BNP Paribas Real Estate Property Management

- GSF Groupe

- Groupe Penelope

- SPIE Facilities

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Outsourced Integrated Services in Public Infrastructure

- 4.2.2 Accelerating Shift to Performance-Based Contracts in Healthcare Facilities

- 4.2.3 Growth of Smart Buildings Enabling Predictive FM via IoT Sensors

- 4.2.4 Heightened Regulatory Pressure on Energy Efficiency Targets

- 4.2.5 Rapid Expansion of Data Centers Requiring Specialized FM

- 4.2.6 Emerging "Hotelization" Trend in Office Spaces Driving Soft FM Bundling

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled HVAC and MEP Technicians

- 4.3.2 Margin Squeeze from Rising Labor Costs Post 2025 Pension Reforms

- 4.3.3 Cybersecurity Risks in Connected Building Management Systems

- 4.3.4 Fragmented Procurement Practices in Municipal Bodies

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 VINCI Facilities

- 6.4.2 ENGIE Cofely

- 6.4.3 Sodexo S.A.

- 6.4.4 ISS A/S

- 6.4.5 Bouygues Energies & Services

- 6.4.6 Atalian Global Services

- 6.4.7 Derichebourg Multiservices

- 6.4.8 Elior Group

- 6.4.9 Samsic Facility

- 6.4.10 Apleona GmbH

- 6.4.11 Dalkia Groupe EDF

- 6.4.12 CBRE Group Inc.

- 6.4.13 Compass Group plc

- 6.4.14 Serco Group plc

- 6.4.15 JLL Integrated Facilities Management

- 6.4.16 Cushman & Wakefield plc

- 6.4.17 BNP Paribas Real Estate Property Management

- 6.4.18 GSF Groupe

- 6.4.19 Groupe Penelope

- 6.4.20 SPIE Facilities

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment