PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065450

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065450

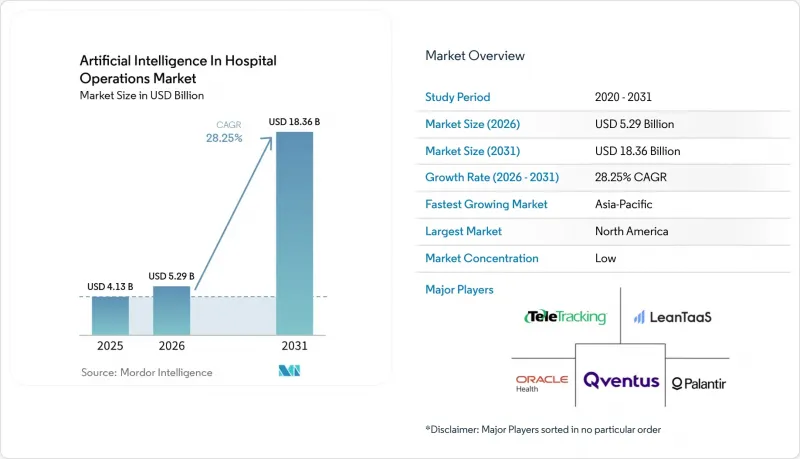

Artificial Intelligence In Hospital Operations - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the artificial intelligence in hospital operations market size is projected to be USD 4.13 billion in 2025, USD 5.29 billion in 2026, and reach USD 18.36 billion by 2031, growing at a CAGR of 28.25% from 2026 to 2031.

This report is Segmented by Offering (Software, Services, Hardware), Use Case (Patient Flow, Workforce Management, Revenue Cycle, Command Center, Perioperative, Asset/Room Ops), Technology (Machine Learning, NLP, Generative AI, Computer Vision, Rules-Based Optimization), Deployment (Cloud, On-Premise, Hybrid), and Geography (North America, Europe, and More). Forecasts in Value (USD).

Global Artificial Intelligence In Hospital Operations Market Trends and Insights

Workforce Shortages and Administrative Burden Push Automation

The Artificial Intelligence in Hospital Operations market is gaining support from chronic workforce strain, which is pushing hospitals to automate staffing, scheduling, and routine administrative work with a clearer return tied to patient safety and labor stability. Duke Health, using GE HealthCare command-center staffing tools, achieved 95% forecasting accuracy for staffing needs up to 14 days in advance and cut temporary labor use by 50%, which created capacity for 500 additional patients each year without adding physical space. This has changed how providers judge operational AI, because tools are now being measured against retention, overtime, and workload balance rather than only against throughput. A 2025 study in Systems found that an AI-enabled rostering system used within a participatory governance model reduced nursing turnover pressure and shift-allocation conflict, which supports the view that deployment quality matters as much as algorithm quality. As a result, hospitals entering the Artificial Intelligence in Hospital Operations market are treating governance readiness, workflow redesign, and staff acceptance as core procurement criteria.

Pressure to Improve Patient Flow, Bed Turnover, and ED Throughput

The Artificial Intelligence in Hospital Operations market is also being lifted by the cost of poor patient flow, because emergency departments, inpatient units, and discharge teams all depend on earlier visibility into bottlenecks. A 2025 study in JMIR Medical Informatics showed that machine learning models could forecast emergency department waiting counts with a mean absolute error as low as 2.45, which gives hospitals more time to adjust staffing and bed allocation before congestion builds. A 2025 digital-twin study presented at the IEOM Society Paris conference reported a 53.7% reduction in total bed requirements and a 63.9% decline in patient waiting times when pooled-resource strategies replaced compartmentalized bed management. These results matter because they show that hospitals are no longer using AI only to improve scheduling at the margin, they are using it to redesign how beds, staff, and patient movement are coordinated across the enterprise. In high-occupancy systems, this is also shifting vendor focus toward tools that shorten length of stay and accelerate discharge decisions, since the next limit is often bed scarcity rather than weak planning.

High Implementation and Maintenance Cost

The Artificial Intelligence in Hospital Operations market still faces a meaningful adoption barrier because hospitals must fund software, integration, data preparation, training, and workflow redesign before benefits appear at scale. A 2025 study in the Journal of Medical Artificial Intelligence found that hospital AI adoption can remain net-value negative for 4 to 5 years before turning net-value positive, which compresses decision making for providers already under financial strain. A 2025 JAMIA study covering 43 health systems found that 47% named financial concerns as one of the top 2 barriers to AI tool development or deployment, second only to tool maturity at 77%. This slows adoption most in community, rural, and safety-net settings, where the margin for multiyear payback is narrower and implementation teams are smaller. It also favors vendors in the Artificial Intelligence in Hospital Operations market that can offer phased rollouts, measurable milestones, and lower-risk deployment pathways.

Other drivers and restraints analyzed in the detailed report include:

- TEAM Bundled-Payment Rollout Raises Demand for Discharge and Episode Orchestration

- Cloud, Interoperability, and Command-Center Digitization Improve Implementation Feasibility

- Cybersecurity, Privacy, and Governance Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 72.31% of the Artificial Intelligence in Hospital Operations market in 2025, while services is projected to expand at a 29.38% CAGR through 2031, which shows that the revenue base is still platform-led even as deployment support gains importance. Subscription software remains the core buying model because hospitals prefer lower upfront capital needs, faster rollout, and pre-built integration with existing EHR and workflow systems. Qventus reported in 2026 that willingness among health systems to wait for an EHR vendor to build a needed feature fell from 52% in 2025 to 22% in 2026, which suggests that independent software vendors still have a meaningful window if they can deliver value faster than the large platforms. That keeps software at the center of the Artificial Intelligence in Hospital Operations market, but it also raises the standard for usability, integration speed, and measurable workflow gains.

Services is growing faster because hospitals have learned that operational AI rarely performs well when the tool is installed without process redesign, training, and change management. This is one area where the Artificial Intelligence in Hospital Operations industry is shifting from simple software procurement toward broader operating model work. Providers increasingly need implementation partners that can redesign staffing workflows, build escalation rules, clean fragmented data, and align local teams around new command-center processes. That need becomes stronger when hospitals want AI to manage patient flow, discharge sequencing, perioperative coordination, or revenue cycle workflows across multiple departments at once. Hardware remains the smallest offering layer in strategic importance, but it should benefit from wider use of edge devices, room sensors, and real-time location infrastructure as virtual nursing and smart-room deployments scale beyond pilot programs.

Revenue Cycle and Administrative Automation held 25.24% of the Artificial Intelligence in Hospital Operations market size in 2025, which reflects the scale of billing complexity, coding volume, denial management, and prior authorization burden inside hospitals. This use case has matured earlier than others because coding and claims workflows generate structured, repetitive tasks that fit natural language processing and rules-driven automation well. Optum's 2025 launch of Integrity One, powered by Clinical Language Intelligence, shows how vendors are building integrated revenue cycle platforms that automate work from point of care through final coding rather than optimizing one narrow task at a time. That is why revenue cycle remains the default entry point for many organizations entering the Artificial Intelligence in Hospital Operations market.

Command Center and Operational Decision Support is the fastest-growing use case, with a 29.52% CAGR projected through 2031, because hospitals increasingly want a single operational layer that can coordinate staffing, bed management, throughput, and discharge activity at the same time. GE HealthCare reported that its command-center platform now operates in nearly 500 hospitals globally and can deliver up to a 12x ROI and USD 40 million in savings by reducing operational inefficiency. Patient Flow and Bed Capacity Management and Workforce Management and Staffing Optimization remain among the largest adjacent use cases because both depend on live operational visibility and rapid intervention. Perioperative and Procedural Operations is also gaining momentum as providers extend AI from operating room block utilization into pre-surgical coordination and clinic scheduling. LeanTaaS supported that shift in 2025 when it launched iQueue for Surgical Clinics to connect upstream clinic workflows with downstream surgical coordination.

Geography Analysis

North America held 43.24% of the Artificial Intelligence in Hospital Operations market share in 2025, which keeps the region as the main revenue base for global vendors. The United States drives this position because it combines large-scale hospital digitization with payment models that reward operational visibility and cost control. The strongest near-term catalyst is the CMS TEAM program, which now places 745 hospitals across 188 selected markets under episode accountability and directly raises demand for discharge, post-acute, and care-transition orchestration. This environment supports earlier scaling of command-center, workforce, and revenue cycle AI than in most other regions. Canada continues to move through cloud-based patient flow and workforce tools, while Mexico remains earlier in the digitization curve because hospital IT capacity is less consistent across providers.

Europe remains the second-largest regional cluster for the Artificial Intelligence in Hospital Operations market, with the United Kingdom and Germany acting as the leading adoption centers. WHO Europe reported in 2026 that EU health systems showed clear momentum in AI readiness, supported by the EU AI Act and national strategies, while also facing large regional disparities and increasing dependence on non-EU suppliers in strategic domains. That combination means European adoption is moving forward, but it is doing so under tighter governance expectations and stronger scrutiny of infrastructure control. For vendors, Europe offers meaningful demand but also requires more discipline around transparency, validation, and data governance than many other regions.

Asia-Pacific is the fastest-growing region in the Artificial Intelligence in Hospital Operations market, with a 29.53% CAGR forecast for 2026-2031, supported by greenfield hospital construction in China and India that allows more AI-native design choices. Australia already shows this command-center expansion, with GE HealthCare launching its ORA Command Center across 3 Melbourne hospitals in March 2026. The region is not growing for one single reason, since some countries are building new hospital infrastructure while others are layering AI onto expanding private health networks and large tertiary systems. In the Middle East and Africa, adoption is earlier overall, but sovereign AI investment in the Gulf is creating faster pockets of uptake, illustrated by the 2025 Oracle, Cleveland Clinic, and G42 partnership to build a global AI-based healthcare delivery platform anchored in the UAE. South America remains the smallest regional base, though Brazil is beginning to show proof points, including Rede Mater Dei de Saude's use of 12 AI agents in revenue cycle workflows on Amazon Bedrock AgentCore.

- ABOUT Healthcare

- Artisight

- Ascom

- care.ai

- Dedalus

- Epic Systems

- GE Healthcare

- HealthCare Logic

- Kontakt.io

- LeanTaaS

- Microsoft

- Oracle Health

- Palantir Technologies

- Koninklijke Philips

- Qventus

- Siemens Healthineers

- symplr

- TeleTracking

- WellStack

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Workforce Shortages and Administrative Burden Push Automation

- 4.2.2 Pressure to Improve Patient Flow, Bed Turnover, and ED Throughput

- 4.2.3 Value-Based Care and Margin Pressure Raise ROI for Predictive Operations AI

- 4.2.4 Cloud, Interoperability, and Command-Center Digitization Improve Implementation Feasibility

- 4.2.5 TEAM Bundled-Payment Rollout Raises Demand for Discharge and Episode Orchestration

- 4.2.6 Tightening Staffing-Governance Pressure Boosts AI Scheduling and Virtual Nursing

- 4.3 Market Restraints

- 4.3.1 High Implementation and Maintenance Cost

- 4.3.2 Cybersecurity, Privacy, and Governance Risk

- 4.3.3 Data Quality and Workflow Fragmentation Weaken Model Trust

- 4.3.4 Frontline Resistance to Centralized Command-Center Workflows

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Use Case

- 5.2.1 Patient Flow and Bed Capacity Management

- 5.2.2 Workforce Management and Staffing Optimization

- 5.2.3 Revenue Cycle and Administrative Automation

- 5.2.4 Command Center and Operational Decision Support

- 5.2.5 Perioperative and Procedural Operations

- 5.2.6 Asset, Room, and Ancillary Operations

- 5.3 By Technology

- 5.3.1 Machine Learning

- 5.3.2 Natural Language Processing

- 5.3.3 Generative AI and Agentic AI

- 5.3.4 Computer Vision and Ambient Intelligence

- 5.3.5 Rules-based Optimization and Simulation

- 5.4 By Deployment Model

- 5.4.1 Cloud

- 5.4.2 On-premise

- 5.4.3 Hybrid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ABOUT Healthcare

- 6.3.2 Artisight

- 6.3.3 Ascom

- 6.3.4 care.ai

- 6.3.5 Dedalus

- 6.3.6 Epic Systems

- 6.3.7 GE HealthCare

- 6.3.8 HealthCare Logic

- 6.3.9 Kontakt.io

- 6.3.10 LeanTaaS

- 6.3.11 Microsoft

- 6.3.12 Oracle Health

- 6.3.13 Palantir Technologies

- 6.3.14 Philips

- 6.3.15 Qventus

- 6.3.16 Siemens Healthineers

- 6.3.17 symplr

- 6.3.18 TeleTracking

- 6.3.19 WellStack

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment