PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065507

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065507

Philippines Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

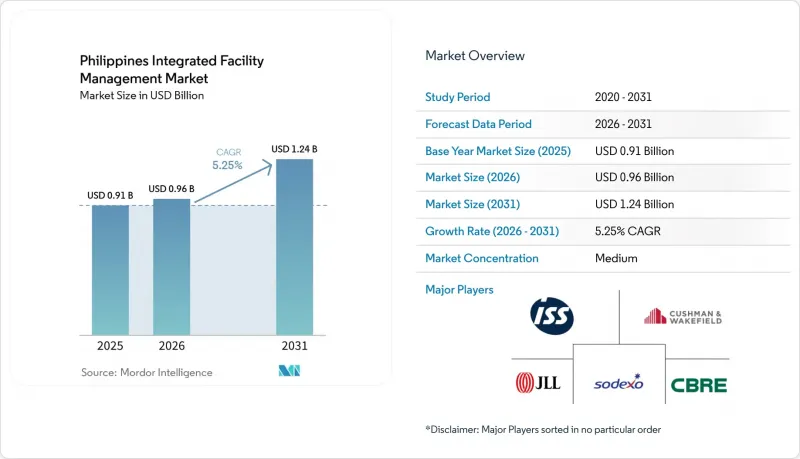

According to Mordor Intelligence, the philippines integrated facility management market size is projected to be USD 0.91 billion in 2025, USD 0.96 billion in 2026, and reach USD 1.24 billion by 2031, growing at a CAGR of 5.25% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Integrated Facility Management Market Trends and Insights

Build Better More Infrastructure Pipeline Expansion

The Philippines integrated facility management market is drawing support from the government's broader infrastructure build-out because new rail, terminal, and utility assets create recurring service demand after construction ends. The PPP pipeline expanded materially by January 2026, and the project base now covers a larger set of assets that move into operating and maintenance phases over time. In May 2026, the administration also unveiled a PHP 3.16 trillion (USD 54.6 billion) project pipeline, across 252 projects, with railway development taking the largest value share in that list. That matters because concessionaires usually focus on transport delivery and asset operation rather than building large in-house FM teams across every location. Providers that can combine technical maintenance, asset management, cleaning, and security are better positioned to win bundled work as these facilities come online. Procurement activity is therefore likely to deepen between 2027 and 2030, when today's construction pipeline converts into a broader installed base of operating public assets.

Outsourcing Trend Among BPO and Commercial Offices

The Philippines integrated facility management market continues to benefit from the outsourcing practices of the office sector, especially where large occupiers prefer predictable service standards across multi-floor or campus-style sites. Metro Manila office transactions reached 847,000 sqm in 2025, and that recovery was supported by IT-BPM demand and faster expansion from Global Capability Centers. Provincial expansion also widened the contract map beyond Cebu and Davao, as operators added capacity in cities such as Bacolod and across other established delivery locations. This matters because BPO requirements are no longer limited to basic occupancy support, since healthcare information management, AI operations, and software development environments require better thermal control, more dependable power support, and cleaner indoor air. Those changes raise the FM specification of both existing and newly leased sites, which strengthens the case for integrated service contracts instead of separate single-service vendors. The demand base still carries some exposure to U.S. policy risk because North America remains the main origin of IT-BPM investment, so providers are increasingly testing revenue plans against slower client expansion scenarios.

Skilled-Labor Shortage and Wage Inflation

The Philippines integrated facility management market still faces a labour bottleneck, and the most acute shortage exists in licensed MEP engineers and senior technical supervisors. The problem is more severe in major business districts, where specialist roles can remain open for extended periods and experienced engineering staff command significant pay premiums over standard market benchmarks. Overseas demand worsens the shortage because Gulf employers continue to offer materially higher pay for comparable engineering and construction management roles. That outflow reduces the pool of experienced professionals available for technically demanding contracts in hospitals, industrial plants, and data centers. It also limits how quickly domestic providers can move beyond soft services into more complex hard FM scopes. At the same time, wage pressure weakens margins on fixed-price contracts, which is why providers are pushing for annual escalation clauses, even though some public-sector buyers remain resistant.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare Facility Build-outs and Modernization

- Smart-Building and IoT-Enabled FM Adoption

- Energy-Cost Volatility in the Grid

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft integrated facility management (FM) held 68.41% of the Philippines integrated facility management (IFM) market share in 2025, while Hard FM is projected to expand at a 6.07% CAGR through 2031. That revenue mix reflected the buyer base of the Philippines IFM industry, where office occupiers, hospitality sites, and retail-led facilities still account for a large share of active contracts. Cleaning, office support, and security remained the core revenue generators because they are required at high frequency and across a wide installed base of commercial premises. These services also offered providers repeat contract volumes and steadier cash flow than highly cyclical project-linked work. Catering remained more concentrated in industrial plants, hospitals, and very large BPO campuses where on-site food provision supports workforce welfare and operating continuity.

Hard FM is growing faster because new asset classes carry higher technical obligations in MEP, HVAC, fire safety, and planned maintenance. Data centers, railway systems, and hospital facilities are increasing the engineering intensity of the Philippines IFM market and pushing buyers toward preventive maintenance and asset management models. Within the hard FM stack, asset management and MEP and HVAC services hold the strongest revenue concentration because downtime in industrial, transport, and healthcare sites has direct operating consequences. Fire and life-safety services remain smaller in revenue terms, but they maintain a reliable demand floor because compliance is mandatory across public and private buildings. Other hard FM scopes, including civil maintenance and facade work, are expanding with the built environment, but they remain less differentiated than technical building systems work. PCAB Quadruple A classification and formal quality, environmental, and safety credentials continue to matter for large utility and government accounts, which keeps the top end of the service category more selective.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- ISS A/S

- Sodexo S.A.

- Atalian Global Services Philippines Inc.

- Servicio Filipino Inc.

- Meralco Industrial Engineering Services Corporation

- SGS Philippines, Inc.

- Santos Knight Frank, Inc.

- Century Properties Management, Inc.

- G4S Secure Solutions (Philippines), Inc.

- KMC Solutions Holdings, Inc.

- Mansion Maintenance Company, Inc.

- Kontrac Facilities Management Services, Inc.

- Hydron Corporation

- WeCare Facility Management Services, Inc.

- Artelia Group

- CPMGI

- Kabraso Multi-Purpose Cooperative

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Build Better More Infrastructure Pipeline Expansion

- 4.2.2 Outsourcing Trend Among BPO and Commercial Offices

- 4.2.3 Healthcare Facility Build-outs and Modernization

- 4.2.4 Smart-Building and IoT-Enabled FM Adoption

- 4.2.5 Mandatory ESG and Green-Building Certifications

- 4.2.6 Hyperscale Data-Center Capacity Growth

- 4.3 Market Restraints

- 4.3.1 Skilled-Labor Shortage and Wage Inflation

- 4.3.2 Energy-Cost Volatility in the Grid

- 4.3.3 Fragmented Supplier Base and Price Competition

- 4.3.4 Compliance Burden from Energy Efficiency and Conservation Act Audits

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 CBRE Group, Inc.

- 6.3.2 Jones Lang LaSalle Incorporated

- 6.3.3 Cushman & Wakefield plc

- 6.3.4 ISS A/S

- 6.3.5 Sodexo S.A.

- 6.3.6 Atalian Global Services Philippines Inc.

- 6.3.7 Servicio Filipino Inc.

- 6.3.8 Meralco Industrial Engineering Services Corporation

- 6.3.9 SGS Philippines, Inc.

- 6.3.10 Santos Knight Frank, Inc.

- 6.3.11 Century Properties Management, Inc.

- 6.3.12 G4S Secure Solutions (Philippines), Inc.

- 6.3.13 KMC Solutions Holdings, Inc.

- 6.3.14 Mansion Maintenance Company, Inc.

- 6.3.15 Kontrac Facilities Management Services, Inc.

- 6.3.16 Hydron Corporation

- 6.3.17 WeCare Facility Management Services, Inc.

- 6.3.18 Artelia Group

- 6.3.19 CPMGI

- 6.3.20 Kabraso Multi-Purpose Cooperative

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment