PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065533

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065533

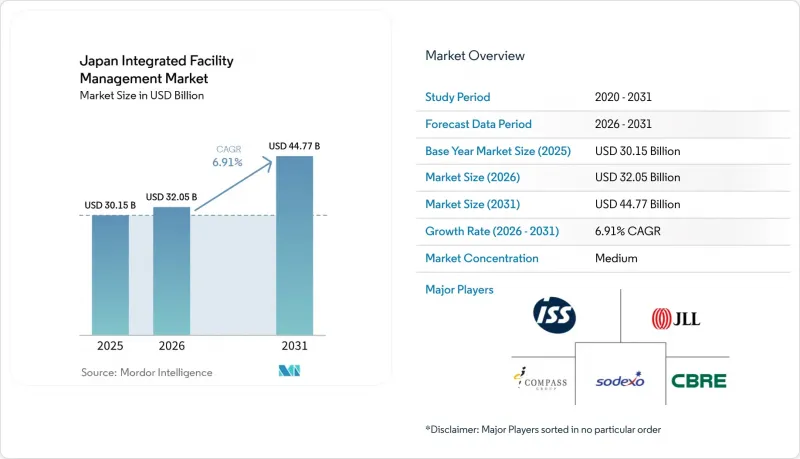

Japan Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan integrated facility management market size is expected to increase from USD 30.15 billion in 2025 to USD 32.05 billion in 2026 and reach USD 44.77 billion by 2031, growing at a CAGR of 6.91% over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

Japan Integrated Facility Management Market Trends and Insights

Rising Aging Infrastructure Driving Outsourcing Demand

Aging commercial buildings are creating a long-duration outsourcing base for the Japan integrated facility management market because older assets need more coordinated upkeep and stricter maintenance planning. Seismic reinforcement, MEP upgrades, fire safety work, and sanitation obligations are harder to manage when handled by disconnected vendors, especially in large, occupied properties that cannot tolerate service disruptions. Asset owners are therefore moving toward integrated providers that can handle multiple technical scopes within a single contract and maintain documentation aligned with statutory requirements. This shift also improves contract stickiness because clients place value on single-point accountability, lifecycle visibility, and fewer operational handoffs across the building portfolio. In practice, the aging stock in Tokyo, Osaka, and Nagoya is supporting a wider role for providers that can combine building engineering oversight with scheduled compliance execution. That keeps the Japan integrated facility management (IFM) market tied not only to routine services but also to recurring upgrade cycles across mature urban assets.

Growing Demand for Predictive Maintenance Accuracy

Predictive maintenance is becoming a practical growth lever in the Japan integrated facility management market because it helps providers shift from scheduled inspections to condition-based intervention. This matters more in Japan because aging building systems, labour scarcity, and the need for technical reliability raise the cost of reactive maintenance failure. NTT Docomo and NTT Facilities began field validation in April 2026 of a conversational AI system that uses Graph RAG and multi-agent processing to let staff query BIM data in natural language across seven NTT Docomo buildings. The model is important because it lowers the training barrier for non-specialist FM personnel while improving access to asset health information in daily operations. NTT Data also reported in 2025 that BIM-FM integration at its Mitaka East facility reduced model data size by 98.8% while preserving full asset visibility, supporting broader multi-site deployment on standard hardware. As these tools move from pilot use to contract expectations, the Japan IFM market will keep moving toward pricing based on uptime, prevented failures, and measurable building outcomes rather than labour input alone.

High Labor Costs Limiting Future Competitiveness

Labor cost inflation remains the clearest near-term restraint on the Japan integrated facility management market because staffing is still essential across cleaning, security, inspections, and building operations. Wage pressure is difficult to offset when many contracts were designed around traditional labour deployment and low pass-through flexibility. The pressure is more visible in public-sector work, where procurement structures often limit how much cost inflation can be reflected in contract pricing. That weakens the economics of advanced service delivery because providers may hesitate to place higher-skilled teams or digital support layers into contracts that do not compensate for rising execution costs. It also accelerates the push toward robotic cleaning, remote monitoring, and AI-assisted security because automation becomes a hedge against structurally tight labour supply rather than a simple efficiency upgrade. As that divide widens, scale operators with funding and technology will be better placed than cost-reactive providers to defend margins in the Japan integrated facility management (IFM) market.

Other drivers and restraints analyzed in the detailed report include:

- Government Energy and Corporate FM Service Needs Are Improving Integrated Services

- Local Technology and Managed Services Are Growing Rapidly

- Stringent Building Codes Increasing Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management (FM) held 54.4% of the Japan integrated facility management market share in 2025, while Hard FM is projected to grow at a 7.7% CAGR through 2031. Hard FM is expanding faster because clients are giving more weight to building integrity, lifecycle planning, and the coordination of engineering-heavy scopes under one accountable provider. Demand is strongest where aging assets, retrofit requirements, and performance-led maintenance need a deeper technical operating model than basic scheduled servicing. NTT Data's work at the Mitaka East facility showed that BIM-FM integration can preserve full asset visibility while cutting model data size by 98.8%, which supports broader hard service deployment across large portfolios without a heavy system burden. NTT Facilities and NTT Docomo are also testing conversational AI for building information access, which can reduce the friction of using BIM data in day-to-day FM work and improve the quality of technician responses.

Soft Facility Management remains the foundational volume layer of the Japan IFM market because cleaning, catering, waste management, front-of-house support, and related recurring services are tied to daily building continuity. Even when occupiers tighten budgets, these functions are difficult to defer for long because they directly affect hygiene, occupant experience, and baseline compliance. The segment also fits integrated contracts well because soft services are often the first bundle clients consolidate before they expand into more technical scopes. That creates a practical entry route for providers that want to deepen account coverage over time and turn recurring site presence into larger managed service relationships. In that sense, Soft FM continues to anchor the Japan integrated facility management industry even as Hard FM becomes the faster-growing part of the service mix.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Compass Group PLC

- ISS A/S

- Sodexo S.A.

- Mitsui Fudosan Facilities Co., Ltd.

- Tokyu Community Corp.

- Mitsubishi Estate Facilities Co., Ltd.

- Sumitomo Mitsui Construction Facilities Co., Ltd.

- NTT Facilities, Inc.

- Secom Co., Ltd.

- Daikin Facilities Co., Ltd.

- Kajima Tatemono Sogo Kanri Co., Ltd.

- Obayashi Facilities Co., Ltd.

- Tokyu Livable, Inc.

- AEON Delight Co., Ltd.

- Hakuyo Facilities Management Co., Ltd.

- Nihon Housing Co., Ltd.

- Meiwa Facilities Co., Ltd.

- Shinryo Corporation

- Daiwa House Group Facilities Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Aging Infrastructure, Citing Outsourcing Demand

- 4.2.2 Accuracy of Demand of the Predictive Maintenance

- 4.2.3 Government Energy/Corporate FM Service Needs for Improving Integrated Services

- 4.2.4 Local Technology/Managed Services Growing Rapidly

- 4.2.5 Expansion of Data Centers Resulting in FM Specialization

- 4.2.6 Rising Healthcare and Institutional Facility Requirements Amid Japan's Aging Demographics

- 4.3 Market Restraints

- 4.3.1 High Labor Costs Limiting Future Competitiveness

- 4.3.2 Stringent Building Codes Increasing Compliance Costs

- 4.3.3 Shortage of FM Talent for Niche Services

- 4.3.4 Outdated Performance Metrics Hindering Administration (CAFM)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group, Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Compass Group PLC

- 6.4.4 ISS A/S

- 6.4.5 Sodexo S.A.

- 6.4.6 Mitsui Fudosan Facilities Co., Ltd.

- 6.4.7 Tokyu Community Corp.

- 6.4.8 Mitsubishi Estate Facilities Co., Ltd.

- 6.4.9 Sumitomo Mitsui Construction Facilities Co., Ltd.

- 6.4.10 NTT Facilities, Inc.

- 6.4.11 Secom Co., Ltd.

- 6.4.12 Daikin Facilities Co., Ltd.

- 6.4.13 Kajima Tatemono Sogo Kanri Co., Ltd.

- 6.4.14 Obayashi Facilities Co., Ltd.

- 6.4.15 Tokyu Livable, Inc.

- 6.4.16 AEON Delight Co., Ltd.

- 6.4.17 Hakuyo Facilities Management Co., Ltd.

- 6.4.18 Nihon Housing Co., Ltd.

- 6.4.19 Meiwa Facilities Co., Ltd.

- 6.4.20 Shinryo Corporation

- 6.4.21 Daiwa House Group Facilities Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment