PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072514

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072514

Singapore Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

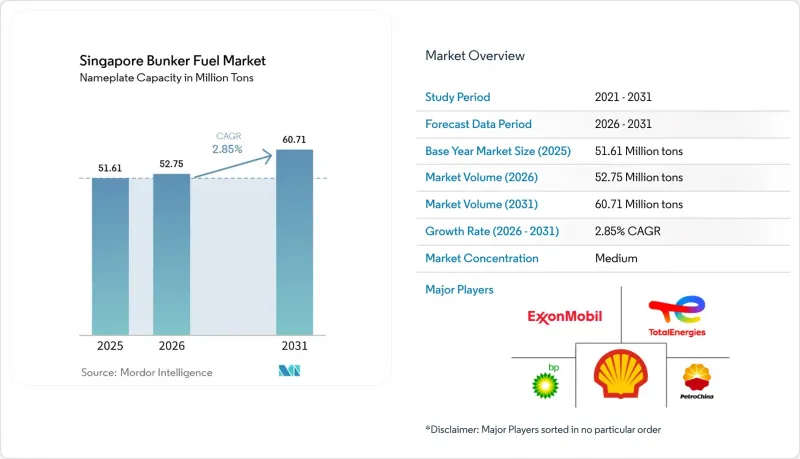

According to Mordor Intelligence, the singapore bunker fuel market size in terms of nameplate capacity is projected to be 51.61 million tons in 2025, 52.75 million tonnes in 2026, and reach 60.71 million tonnes by 2031, growing at a CAGR of 2.85% from 2026 to 2031.

This report is Segmented by Fuel Type (HSFO, VLSFO, ULSFO, MGO, LNG, Methanol, Bio-/Synthetic Fuels, Ammonia, and More), Bunkering Method (Ship-To-Ship, Port-To-Ship, LNG Barge-To-Ship, and Portable Tanks and Containers), and Vessel Type (Container, Tanker, Bulk Carrier, General Cargo, Passenger/Ro-Pax, and Offshore and Specialized). The Market Sizes and Forecasts are Provided in Terms of Volume (MT).

Singapore Bunker Fuel Market Trends and Insights

IMO 2020 Sulfur-Cap Compliance Boosting VLSFO Demand

The IMO's 0.50% sulfur ceiling, active since January 2020, pushed VLSFO to a 55.3% share in 2025 and simultaneously triggered an HSFO rebound as scrubber economics improved when the HSFO-VLSFO spread touched USD 150-180 per ton in late 2024. Scrubber payback periods fell below 18 months for fuel-intensive VLCCs and capesize bulkers, motivating owners to fund retrofits even amid freight-rate volatility. Suppliers must now carry parallel VLSFO and HSFO inventories, inflating working-capital needs by roughly 15-20% compared with pre-2020 practice. The IMO's 2023 GHG strategy requiring 5-10% emission cuts by 2030 accelerates interest in LNG and methanol, likely tapering VLSFO's dominance beyond 2028. Maersk's successful 2023 ship-to-ship methanol bunkering in Singapore shows the technical feasibility of alternatives, yet methanol's lower energy density forces compromises on cargo capacity.

Singapore's Position as the World's Largest Bunkering Hub

The port sold 54.92 MT of fuel in 2024, equaling about 18% of global marine demand and benefitting from 24/7 operations and over 50 licensed suppliers. Red Sea diversions boosted Asia-Europe voyages via the Cape, adding 8,500 nautical miles and 33% more fuel burn, translating into an extra 2-3 MT of bunkering volume. Jurong Island's land scarcity restricts storage expansion to roughly 20.5 million cubic meters, nudging some buyers toward Malaysia's Port Klang and Indonesia's Batam when space constraints pinch. Regional refinery build-outs in India and Vietnam could erode as much as 5-8% of Singapore's share by 2030 unless the city-state sustains its alternative-fuel lead. The Green Ship Programme's 2024 payouts for 460,000 ton of LNG and 880,000 ton of biofuels underscore the pivot to future fuels that aims to cement hub relevance over the long run.

Oil-Price Volatility Compressing Trader Margins

Brent crude oscillated between USD 70 and USD 90 per barrel in 2024, squeezing bunker-trader margins to 3-5% from the 6-8% typical in 2020-2022 as suppliers struggled to pass cost swings to shipowners on quarterly contracts. Maersk's average bunker expense fell to USD 569 per ton in Q1 2025, down 9% year-on-year, yet price transmission lagged crude by four to six weeks, spotlighting timing mismatches. Independents lacking upstream integration must pre-fund inventories 30-45 days ahead, exposing them to spikes that can erase quarterly profit. An HSFO price rally in October 2024 widened the HSFO-VLSFO spread to USD 150-180 per ton, prompting a 15% uptick in scrubber-equipped calls but forcing suppliers to widen bid-ask spreads by 5-7% to manage risk. Hedging remains limited for smaller firms because margin calls tie up scarce working capital.

Other drivers and restraints analyzed in the detailed report include:

- Rising Container Throughput from E-Commerce-Driven Trade

- Government Incentives for LNG Bunkering Infrastructure

- Decarbonisation Shift Toward Ammonia & Methanol Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Singapore bunker fuel market size for very-low-sulfur fuel oil reached 29.2 MT in 2025, corresponding to a 55.3% share as vessels complied with the IMO 2020 sulfur cap. LNG volumes, though starting from a small base, are rising at a 28.9% CAGR through 2031 on the back of 460,000 tons sold in 2024 and the arrival of additional LNG bunker barges. HSFO rebounded in 2024 when the price gap to VLSFO widened, with scrubber-fitted ships capturing savings and cutting payback periods below 18 months. Methanol, biofuels, and ammonia collectively remain below 2% today, yet regulatory clarity and pilot infrastructure signal an inflection from 2028 onward.

Longer term, alternative fuels are expected to challenge VLSFO dominance as shipowners future-proof fleets against impending carbon levies. The Singapore bunker fuel market is therefore likely to exhibit a dual-track profile: stable demand for conventional fuels through 2028, overlapped by accelerating uptake of LNG, methanol, and advanced biofuels thereafter. Feedstock constraints on waste-oil-based biodiesel and safety questions around ammonia keep supply tight, but early movers in these niches could secure premium margins once regulation mandates zero-carbon fuels.

Complete Report Scope:

- By Fuel Type

- High-Sulfur Fuel Oil (HSFO)

- Very-Low-Sulfur Fuel Oil (VLSFO)

- Ultra-Low-Sulfur Fuel Oil (ULSFO)

- Marine Gas Oil (MGO)

- Liquefied Natural Gas (LNG)

- Methanol

- Bio-/Synthetic Fuels

- Ammonia

- Other Fuel Types

- By Bunkering Method

- Ship-to-Ship

- Port-to-Ship (Truck/Pipeline)

- LNG Barge-to-Ship

- Portable Tanks and Containers

- By Vessel Type

- Container

- Tanker

- Bulk Carrier

- General Cargo

- Passenger/Ro-Pax

- Offshore and Specialized

List of Companies Covered in this Report:

- PetroChina International (Singapore)

- Sentek Marine & Trading

- Ocean Bunkering Services

- Equatorial Marine Fuel

- Shell Eastern Trading

- TotalEnergies Marine Fuels

- ExxonMobil Asia Pacific

- BP Singapore

- Chevron Singapore

- Glencore Singapore

- Trafigura - TFG Marine

- Minerva Bunkering

- Vitol Bunkers

- Bunker One (Singapore)

- Pavilion Energy

- CMA CGM Fuel Singapore

- Maersk Oil Trading Singapore

- Hafnia Bunkers

- Mitsui & Co. Energy Trading

- Itochu Petroleum Singapore

- Sinanju-Consort Bunkers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IMO 2020 sulfur-cap compliance boosting VLSFO demand

- 4.2.2 Singapore's position as the world's largest bunkering hub

- 4.2.3 Rising container throughput from e-commerce-driven trade

- 4.2.4 Government incentives for LNG bunkering infrastructure

- 4.2.5 Emerging bio-/e-fuel bunkering pilots under Green Ship Programme

- 4.2.6 Digital bunkering platforms lowering transaction costs

- 4.3 Market Restraints

- 4.3.1 Oil-price volatility compressing trader margins

- 4.3.2 Decarbonisation shift toward ammonia & methanol alternatives

- 4.3.3 Land-scarce storage expansion limitations

- 4.3.4 Stricter mass-flow-meter enforcement raising OPEX

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 High-Sulfur Fuel Oil (HSFO)

- 5.1.2 Very-Low-Sulfur Fuel Oil (VLSFO)

- 5.1.3 Ultra-Low-Sulfur Fuel Oil (ULSFO)

- 5.1.4 Marine Gas Oil (MGO)

- 5.1.5 Liquefied Natural Gas (LNG)

- 5.1.6 Methanol

- 5.1.7 Bio-/Synthetic Fuels

- 5.1.8 Ammonia

- 5.1.9 Other Fuel Types

- 5.2 By Bunkering Method

- 5.2.1 Ship-to-Ship

- 5.2.2 Port-to-Ship (Truck/Pipeline)

- 5.2.3 LNG Barge-to-Ship

- 5.2.4 Portable Tanks and Containers

- 5.3 By Vessel Type

- 5.3.1 Container

- 5.3.2 Tanker

- 5.3.3 Bulk Carrier

- 5.3.4 General Cargo

- 5.3.5 Passenger/Ro-Pax

- 5.3.6 Offshore and Specialized

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PetroChina International (Singapore)

- 6.4.2 Sentek Marine & Trading

- 6.4.3 Ocean Bunkering Services

- 6.4.4 Equatorial Marine Fuel

- 6.4.5 Shell Eastern Trading

- 6.4.6 TotalEnergies Marine Fuels

- 6.4.7 ExxonMobil Asia Pacific

- 6.4.8 BP Singapore

- 6.4.9 Chevron Singapore

- 6.4.10 Glencore Singapore

- 6.4.11 Trafigura - TFG Marine

- 6.4.12 Minerva Bunkering

- 6.4.13 Vitol Bunkers

- 6.4.14 Bunker One (Singapore)

- 6.4.15 Pavilion Energy

- 6.4.16 CMA CGM Fuel Singapore

- 6.4.17 Maersk Oil Trading Singapore

- 6.4.18 Hafnia Bunkers

- 6.4.19 Mitsui & Co. Energy Trading

- 6.4.20 Itochu Petroleum Singapore

- 6.4.21 Sinanju-Consort Bunkers

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment