PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072551

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072551

Asia Pacific IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

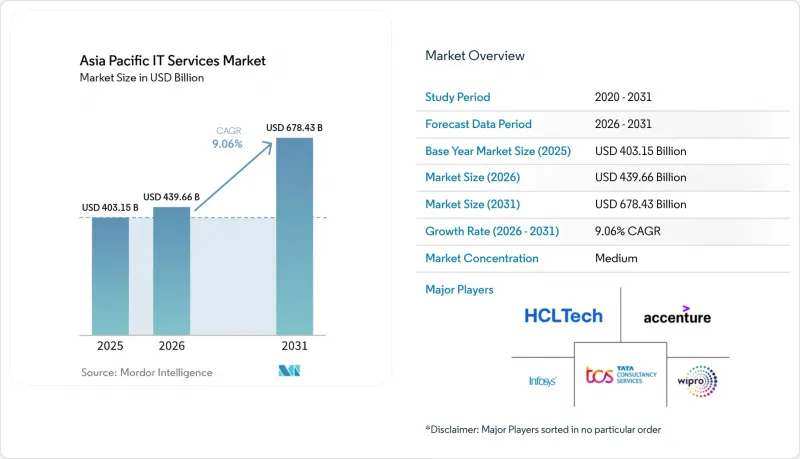

According to Mordor Intelligence, the asia pacific IT services market size is projected to expand from USD 403.15 billion in 2025 and USD 439.66 billion in 2026 to USD 678.43 billion by 2031, registering a CAGR of 9.06% between 2026 to 2031.

This report is Segmented by Service Type (IT Consulting and Implementation, IT Outsourcing, and More), Deployment Model (On-Premises, Public Cloud, Private Cloud, and More), Enterprise Size (Large, Medium-Sized, and Small and Micro), End-User Industry (BFSI, Manufacturing, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific IT Services Market Trends and Insights

Rapid Digital Transformation Across Industries

Financial institutions, manufacturers, and retailers are rebuilding core systems around API-driven microservices to support real-time analytics and omnichannel engagement, redirecting substantial capital toward cloud migration and integration consulting. A regional survey found that 73% of organizations plan to raise transformation budgets, yet capability gaps persist, with only 42% of Thai executives maintaining detailed roadmaps. This mismatch fuels steady demand for advisory partners that can bridge legacy mainframes and cloud platforms. Banks in Singapore and Japan are rolling out real-time payments and AI-based credit scoring, while retailers invest in edge analytics for dynamic pricing to counter e-commerce rivals. The resulting project pipeline spans cloud migration, data-platform unification, and omnichannel customer-experience design, each feeding multi-year managed-service contracts focused on optimization and support.

AI and Generative-AI Managed-Services Boom

Generative AI adoption is accelerating as firms seek to boost developer productivity and automate call-center workflows. Weekly usage among knowledge workers reached 78% in 2024, the highest global rate, yet just one-third of companies have formal governance, opening the door for managed service providers that bundle model selection, fine-tuning, and responsible-AI controls. Pilot programs in India demonstrated 43-45% productivity gains, prompting rapid scaling across software, insurance, and telecom firms. Providers that deliver pre-trained vertical models, continuous monitoring, and cost-optimized inference infrastructure are capturing premium margins. Early adopter markets such as Singapore and South Korea are now moving from proofs of concept to enterprise-wide rollouts, driving double-digit growth in AI-operations outsourcing.

Severe Talent Shortages and Wage Inflation in Tier-1 Hubs

Cloud architects, cybersecurity analysts, and AI engineers remain in short supply, driving double-digit wage jumps in Bengaluru, Shenzhen, and Singapore. Korn Ferry forecasts a regional deficit of 4.7 million skilled professionals by 2030, with India alone lacking up to 1.5 million experts. Providers face margin compression as labor costs rise 10-15% annually and clients resist billing-rate hikes. To mitigate, vendors are automating routine service-desk tasks, reskilling mid-level engineers in cloud security, and shifting delivery to secondary cities in Vietnam and the Philippines. While these measures relieve pressure, the supply-demand imbalance is projected to persist through 2027, constraining growth in high-complexity services.

Other drivers and restraints analyzed in the detailed report include:

- Sovereign-Cloud Mandates Reshaping In-Region Delivery

- Cost-Efficiency Push Driving ITO and BPO Adoption

- Escalating Cybersecurity and Data-Sovereignty Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed cloud and XaaS services are forecast to grow at a 10.11% CAGR as enterprises opt for elastic consumption over fixed-capacity contracts. The Asia-Pacific IT Services market size for IT outsourcing remained dominant in 2025, holding a 32.74% share and underpinning infrastructure management and application support requirements. However, demand is tilting toward outcome-based bundles that integrate infrastructure, platform, and software layers under unified SLAs. Vendors differentiate through industry blueprints, Kubernetes orchestration, and cloud-cost optimization. Meanwhile, IT consulting retains strategic relevance for large-scale modernization projects, particularly in banking core-system replacement and plant-floor digitization within automotive manufacturing. Business-process outsourcing continues to attract retailers and telecom operators seeking cost efficiency in finance and human resources workflows. Support and maintenance services face price erosion as self-service portals and AIOps reduce ticket volumes, yet they sustain recurring revenue and client stickiness. Collectively, these dynamics pivot the Asia-Pacific IT Services market toward as-a-service delivery, reshaping partner ecosystems around cloud-centric reference architectures.

In parallel, hyperscalers are embedding managed-service toolkits into their marketplaces, enabling smaller providers to white-label monitoring, backup, and security features without investing in proprietary platforms. Flexera recorded that 89% of global enterprises pursue multi-cloud strategies, a pattern mirrored in Asia-Pacific where clients engage managed providers to navigate interoperability across Amazon Web Services, Microsoft Azure, and Google Cloud. This multi-cloud complexity sustains above-average revenue growth for integration specialists even as commoditization pressures intensify in traditional infrastructure outsourcing.

Hybrid and multi-cloud environments are expanding at a 10.46% CAGR, reflecting regulatory, latency, and cost considerations. Public cloud accounted for 49.73% of spending in 2025, but many financial institutions and governments maintain sensitive workloads on private infrastructure to comply with residency mandates. The Asia-Pacific IT Services market share attached to on-premises systems is steadily declining, yet manufacturing and energy companies still prioritize local processing for latency-critical applications such as machine-vision inspection and SCADA control. Hybrid architectures provide a pragmatic bridge, allowing gradual migration while preserving existing investments. HashiCorp reported that 72% of Asia-Pacific enterprises had integrated at least two cloud providers by 2024, underscoring the premium placed on interoperability tooling. Service partners now bundle policy-as-code governance, FinOps, and workload-placement analytics, enabling clients to optimize spend while satisfying compliance auditors.

Edge computing is further amplifying hybrid demand, particularly in logistics and retail where near-real-time analytics enhance route optimization and in-store personalization. Vendors that can extend single-pane observability across edge, private-cloud, and hyperscale regions are commanding higher margins. As AI inference moves closer to data sources, hybrid models become indispensable, reinforcing their centrality to the Asia-Pacific IT Services market trajectory.

Complete Report Scope:

- By Service Type

- IT Consulting and Implementation

- IT Outsourcing (ITO)

- Business-Process Outsourcing (BPO)

- Managed Cloud and XaaS

- Support, Maintenance and Other Services

- By Deployment Model

- On-premises / Captive

- Public Cloud

- Private Cloud

- Hybrid / Multi-cloud

- By Enterprise Size

- Large Enterprises

- Medium-sized Businesses

- Small and Micro Businesses

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- Manufacturing and Industrial

- Government and Public Sector

- Healthcare and Life Sciences

- Retail, E-Commerce and Consumer Goods

- Telecom and Media

- Transportation and Logistics

- Energy and Utilities

- Other End-user Industries

- By Country

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Singapore

- Taiwan

- Thailand

- Australia

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Accenture plc

- Tata Consultancy Services Ltd.

- Infosys Ltd.

- Wipro Ltd.

- HCL Technologies Ltd.

- Tech Mahindra Ltd.

- Cognizant Technology Solutions Corp.

- Capgemini SE

- Fujitsu Ltd.

- NTT DATA Corp.

- NEC Corp.

- Samsung SDS Co., Ltd.

- LG CNS Co., Ltd.

- Alibaba Cloud Computing Co., Ltd.

- Tencent Cloud Computing (Beijing) Ltd.

- IBM Corp.

- DXC Technology Co.

- Deloitte Touche Tohmatsu Ltd.

- Ernst and Young Global Ltd.

- PricewaterhouseCoopers International Ltd.

- KPMG International Ltd.

- Singtel NCS Pte. Ltd.

- PCCW Solutions Ltd.

- Datacom Group Ltd.

- UST Global (Singapore) Pte. Ltd.

- Nihon Unisys, Ltd.

- Hitachi Vantara LLC

- Amazon Web Services Singapore Pte. Ltd.

- Google Cloud Asia Pacific Pte. Ltd.

- Huawei Cloud Computing Technologies Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Digital Transformation Across Industries

- 4.2.2 Sovereign-Cloud Mandates Reshaping In-Region Delivery

- 4.2.3 Cost-Efficiency Push Driving Ito And Bpo Adoption

- 4.2.4 Ai / Gen-Ai Managed-Services Boom

- 4.2.5 Smart-City Mega-Projects In Asean And India

- 4.2.6 Climate-Tech And Green-It Compliance Outsourcing

- 4.3 Market Restraints

- 4.3.1 Severe Talent Shortages And Wage Inflation In Tier-1 Hubs

- 4.3.2 Escalating Cybersecurity / Data-Sovereignty Compliance Costs

- 4.3.3 Legacy Tech-Debt In State-Owned Enterprises

- 4.3.4 Geopolitical Digital Blocs Fragmenting Supply Chains

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 IT Consulting and Implementation

- 5.1.2 IT Outsourcing (ITO)

- 5.1.3 Business-Process Outsourcing (BPO)

- 5.1.4 Managed Cloud and XaaS

- 5.1.5 Support, Maintenance and Other Services

- 5.2 By Deployment Model

- 5.2.1 On-premises / Captive

- 5.2.2 Public Cloud

- 5.2.3 Private Cloud

- 5.2.4 Hybrid / Multi-cloud

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Medium-sized Businesses

- 5.3.3 Small and Micro Businesses

- 5.4 By End-user Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Manufacturing and Industrial

- 5.4.3 Government and Public Sector

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Retail, E-Commerce and Consumer Goods

- 5.4.6 Telecom and Media

- 5.4.7 Transportation and Logistics

- 5.4.8 Energy and Utilities

- 5.4.9 Other End-user Industries

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Indonesia

- 5.5.6 Malaysia

- 5.5.7 Singapore

- 5.5.8 Taiwan

- 5.5.9 Thailand

- 5.5.10 Australia

- 5.5.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Tata Consultancy Services Ltd.

- 6.4.3 Infosys Ltd.

- 6.4.4 Wipro Ltd.

- 6.4.5 HCL Technologies Ltd.

- 6.4.6 Tech Mahindra Ltd.

- 6.4.7 Cognizant Technology Solutions Corp.

- 6.4.8 Capgemini SE

- 6.4.9 Fujitsu Ltd.

- 6.4.10 NTT DATA Corp.

- 6.4.11 NEC Corp.

- 6.4.12 Samsung SDS Co., Ltd.

- 6.4.13 LG CNS Co., Ltd.

- 6.4.14 Alibaba Cloud Computing Co., Ltd.

- 6.4.15 Tencent Cloud Computing (Beijing) Ltd.

- 6.4.16 IBM Corp.

- 6.4.17 DXC Technology Co.

- 6.4.18 Deloitte Touche Tohmatsu Ltd.

- 6.4.19 Ernst and Young Global Ltd.

- 6.4.20 PricewaterhouseCoopers International Ltd.

- 6.4.21 KPMG International Ltd.

- 6.4.22 Singtel NCS Pte. Ltd.

- 6.4.23 PCCW Solutions Ltd.

- 6.4.24 Datacom Group Ltd.

- 6.4.25 UST Global (Singapore) Pte. Ltd.

- 6.4.26 Nihon Unisys, Ltd.

- 6.4.27 Hitachi Vantara LLC

- 6.4.28 Amazon Web Services Singapore Pte. Ltd.

- 6.4.29 Google Cloud Asia Pacific Pte. Ltd.

- 6.4.30 Huawei Cloud Computing Technologies Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment