PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072657

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072657

China Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

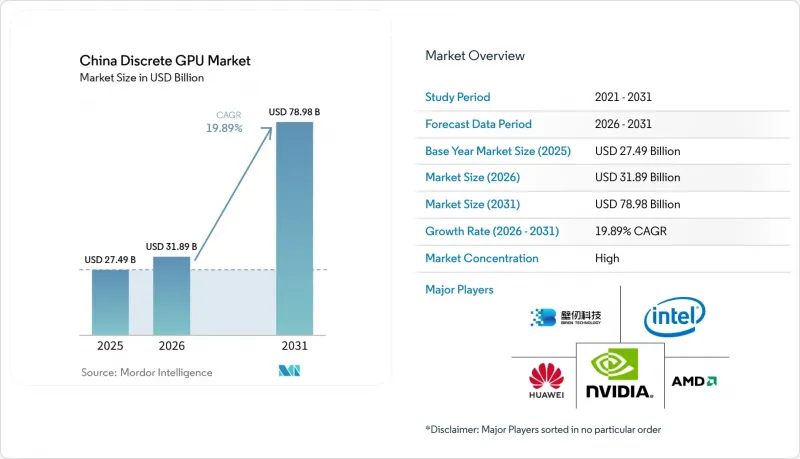

According to Mordor Intelligence, the china discrete GPU market size is projected to expand from USD 27.49 billion in 2025 and USD 31.89 billion in 2026 to USD 78.98 billion by 2031, registering a CAGR of 19.89% between 2026 and 2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

China Discrete GPU Market Trends and Insights

Surging Demand for AI Training and Inference Workloads in Chinese Hyperscale Datacenters

Hyperscale operators have moved GPU procurement to the top of capital-expenditure priorities. Alibaba Cloud spent USD 53 billion in fiscal 2025 and deployed more than 100,000 accelerators across domestic server halls. ByteDance earmarked USD 23 billion the same year to train its Doubao foundation model, an effort that required roughly 50,000 H100-class chips. Tencent doubled AI-related capex, rolling out new GPU clusters for its Hunyuan model. Baidu's Ernie 4.0 stack came online with about 20,000 discrete GPUs that delivered OpenAI-comparable performance. These deployments follow multi-year supply contracts that dampen demand cyclicality and encourage joint silicon-software co-design with local vendors to mitigate export-control risks.

Government Incentives for Domestic Semiconductor Self-Reliance and GPU Innovation

China's National Integrated Circuit Industry Investment Fund Phase III committed CNY 344 billion (USD 47 billion) in 2024, explicitly listing GPU development as a strategic domain. A State Council directive from the same year mandates that half of all government and state-owned enterprise IT procurement source domestic semiconductors by 2027, creating guaranteed demand for homegrown graphics processors.Shanghai offered CNY 2 billion (USD 280 million) in direct grants to GPU startups during 2025, a model replicated by Shenzhen and Wuhan municipalities. The Ministry of Industry and Information Technology sets an 80% semiconductor self-sufficiency goal by 2030, further aligning fiscal resources with road-map milestones. Talent incentives have attracted more than 3,500 engineers back from overseas positions, enlarging the domestic skills pool required for advanced GPU architecture.

U.S. Export Controls Limiting Access to Cutting-Edge GPU IP and HBM Memory

Revisions to United States export rules in January 2025 introduced performance ceilings that restrict bidirectional transfer rates and floating-point throughput for GPUs bound for China DOC.GOV. NVIDIA responded with H20, L20 and L2 variants that deliver about one-third less training throughput than the H100, yet still consumed 15% of 2025 datacenter revenue. AMD's MI308 navigated a protracted licensing process that delayed broad availability until the third quarter of 2025. Supply pressure intensified after the United States urged SK Hynix and Micron to scale back HBM3 exports, reducing allocations to Chinese buyers by roughly 40%. Domestic firms are experimenting with GDDR6X-based chiplet layouts as stop-gaps, but these alternatives incur higher power draw and cooling overhead.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Growth of PC Gaming and Esports Ecosystem in China

- Rapid Adoption of Discrete GPUs in Automotive ADAS and Autonomous-Driving Platforms

- Fragmentation of CUDA-Alternative Software Ecosystems Hindering Domestic GPU Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators accounted for 39.17% of 2025 revenue in the China discrete GPU market, underscoring the structural shift away from purely consumer graphics boards. The segment benefits from multi-year capacity reservations by Alibaba Cloud, Tencent, ByteDance, and Baidu, each scaling fleets that now exceed a combined 300,000 AI accelerators. This procurement discipline stabilizes quarterly demand and supports vendors that can satisfy compliance rules while offering competitive price-performance ratios. Professional visualization and workstation cards trail datacenter silicon but still monetize creative workflows, capturing roughly 12% of the 2025 total as content studios embrace generative AI in video editing and architectural rendering.

The gaming PC and workstation category remains large by volume, yet its revenue share is slowing as average selling prices plateau. Gaming cafes and home enthusiasts continue to refresh rigs, helped by lower-tier domestic GPUs that deliver esports-class frame rates at sub-USD 400 price points. Automotive GPUs, though starting from a smaller base, are on a steep climb. Annual shipments are projected to top 2 million units by 2027 as Li Auto, NIO, and XPeng push centralized compute boxes into mainstream trims. Edge devices covering industrial vision and retail analytics form a nascent but promising slice, favored by data-localization policies that discourage cloud offloading and thus raise on-premises inference demand.

Complete Report Scope:

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Memory Type

- GDDR-Based GPUs

- HBM-Based GPUs

- By Performance Tier

- Low-Cost GPUs (less than 100 USD)

- Mainstream GPUs (100 USD to 400 USD)

- High-Performance Consumer GPUs (400 USD to 1,200 USD)

- Data Center / AI Accelerator GPUs (greater than 1,200 USD)

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Huawei Technologies Co. Ltd. (HiSilicon)

- Biren Technology

- Moore Threads Intelligent Technology Co. Ltd.

- Jingjia Microelectronics Co. Ltd.

- Cambricon Technologies Corp. Ltd.

- Zhaoxin Semiconductor Corp. Ltd.

- Hygon Information Technology Co. Ltd.

- Innosilicon Technology Ltd.

- Tianshu Zhixin Semiconductor Co. Ltd.

- VeriSilicon Holdings Co. Ltd.

- Colorful Technology Co. Ltd.

- Galaxy Microsystems Ltd.

- Micro-Star International Co. Ltd.

- ASUSTeK Computer Inc.

- Lenovo Group Ltd.

- Inspur Electronic Information Industry Co. Ltd.

- Giga-Byte Technology Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AI Training and Inference Workloads in Chinese Hyperscale Datacenters

- 4.2.2 Continuous Growth of PC Gaming and Esports Ecosystem in China

- 4.2.3 Government Incentives for Domestic Semiconductor Self-Reliance and GPU Innovation

- 4.2.4 Rapid Adoption of Discrete GPUs in Automotive ADAS and Autonomous Driving Platforms

- 4.2.5 Rising Demand from Domestic Cloud-Based GPUaaS Providers Targeting SME AI Workloads

- 4.2.6 Expansion of Refurbished GPU Exports Creating Domestic Upgrade Cycle and Price Normalization

- 4.3 Market Restraints

- 4.3.1 U.S. Export Controls Limiting Access to Cutting-Edge GPU IP and HBM Memory

- 4.3.2 Global Semiconductor Supply-Chain Constraints Raising Bill-of-Materials Costs

- 4.3.3 Cooling and Power Infrastructure Limitations in Tier-2 Chinese Datacenters

- 4.3.4 Fragmentation of CUDA-Alternative Software Ecosystems Hindering Domestic GPU Adoption

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-Based GPUs

- 5.2.2 HBM-Based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (less than 100 USD)

- 5.3.2 Mainstream GPUs (100 USD to 400 USD)

- 5.3.3 High-Performance Consumer GPUs (400 USD to 1,200 USD)

- 5.3.4 Data Center / AI Accelerator GPUs (greater than 1,200 USD)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Huawei Technologies Co. Ltd. (HiSilicon)

- 6.4.5 Biren Technology

- 6.4.6 Moore Threads Intelligent Technology Co. Ltd.

- 6.4.7 Jingjia Microelectronics Co. Ltd.

- 6.4.8 Cambricon Technologies Corp. Ltd.

- 6.4.9 Zhaoxin Semiconductor Corp. Ltd.

- 6.4.10 Hygon Information Technology Co. Ltd.

- 6.4.11 Innosilicon Technology Ltd.

- 6.4.12 Tianshu Zhixin Semiconductor Co. Ltd.

- 6.4.13 VeriSilicon Holdings Co. Ltd.

- 6.4.14 Colorful Technology Co. Ltd.

- 6.4.15 Galaxy Microsystems Ltd.

- 6.4.16 Micro-Star International Co. Ltd.

- 6.4.17 ASUSTeK Computer Inc.

- 6.4.18 Lenovo Group Ltd.

- 6.4.19 Inspur Electronic Information Industry Co. Ltd.

- 6.4.20 Giga-Byte Technology Co. Ltd.

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment