PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072658

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072658

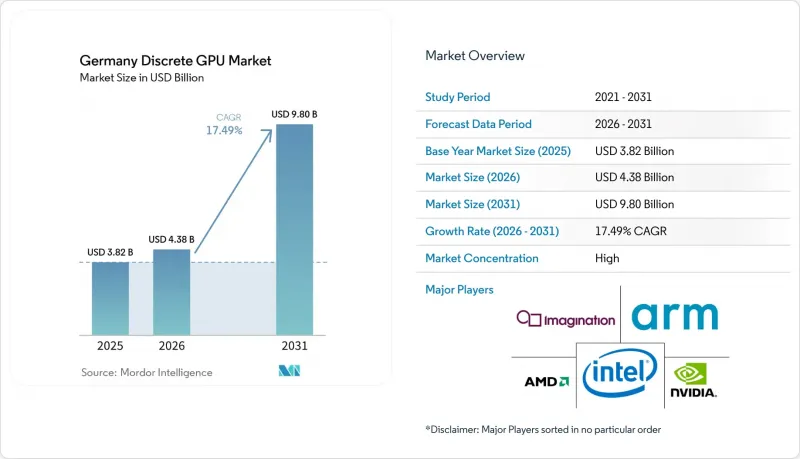

Germany Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany discrete GPU market size is expected to increase from USD 3.82 billion in 2025 to USD 4.38 billion in 2026 and reach USD 9.80 billion by 2031, growing at a CAGR of 17.49% over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), and Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

Germany Discrete GPU Market Trends and Insights

Surging Demand for AI and HPC Workloads in German Data Centers

Germany's sovereign-AI strategy has tilted GPU supply toward enterprise racks. Deutsche Telekom's Tucherpark campus in Munich operates more than 1,000 DGX B200 systems, each drawing 12 MW of renewable power and delivering almost half an exaflop of compute. Early adopters, including Siemens, Agile Robots, and Quantum Systems, train digital twins and simulation workloads locally to comply with EU data-residency rules. Similar GPU clusters at Julich, Freiburg, and Hamburg bring the national total to nearly 40,000 new accelerators, prompting consumer shortages as retail allocations shrink.

Robust PC Gaming and Esports Ecosystem in Germany

German gamers spent EUR 9.4 billion (USD 10.6 billion) in 2025, with hardware outlays up 12% year on year. Despite the enthusiasm, weekly discrete GPU sales at top retailers slid from roughly 2,800 cards to 675, evidencing a 76% unit collapse. Price elasticity remains high: average selling prices rose to EUR 1,100 (USD 1,243) for NVIDIA and EUR 585 (USD 661) for AMD, yet revenue still advanced.Federal grants for game studios climbed to EUR 125 million (USD 141 million) in 2026, ensuring a steady pipeline of domestic titles that rely on high-end graphics.

Supply Chain Disruptions and GPU Shortages

TSMC's limited CoWoS packaging lines and tight HBM3E supply from SK Hynix, Micron, and Samsung have pushed German retail inventories to historic lows. Street prices for an RTX 5090 exceed USD 4,000, double the launch MSRP, and even AMD's mid-range cards face multi-week backorders. The government's sovereign-cloud push intensifies the squeeze as operators lock in bulk orders, sidelining consumer channels.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of GPU-Accelerated Workstations for Professional Visualization

- Energy-Efficiency Mandates Driving Upgrades to Advanced GPU Nodes

- High Up-Front Cost of High-Performance GPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators contributed 40.73% of 2025 revenue to the Germany discrete GPU market share, reflecting the rapid installation of sovereign-AI clusters. The segment is projected to post a 17.75% CAGR to 2031, ensuring it remains the linchpin of Germany discrete GPU market growth. Consumer PCs and professional workstations together form the second pillar, yet their volumes have fallen sharply as supply diverts toward enterprise racks. Gaming consoles and handhelds remain niche because they bundle custom APUs rather than discrete cards, while integrated GPUs in thin-and-light notebooks further erode entry-level demand.

Germany discrete GPU market size for servers will continue to swell as Deutsche Telekom, Google, and Schwarz Group collectively add another 30,000-plus accelerators in sites scheduled for completion by 2027. Automotive edge servers running digital twins, along with Industry 4.0 gateways that need local inferencing, strengthen long-tail adoption. Conversely, mobile and tablet categories lean on ARM-based SoCs with embedded GPUs, undercutting discrete attach rates.

Complete Report Scope:

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Memory Type

- GDDR-based GPUs

- HBM-based GPUs

- By Performance Tier

- Low-Cost GPUs (less than 100 USD)

- Mainstream GPUs (100 USD to 400 USD)

- High-Performance Consumer GPUs (400 USD to 1,200 USD)

- Data Center / AI Accelerator GPUs (greater than 1,200 USD)

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Imagination Technologies Limited

- ARM Limited

- QUALCOMM Incorporated

- Samsung Electronics Co., Ltd.

- Apple Inc.

- HUAWEI Technologies Co., Ltd.

- MediaTek Inc.

- VIA Technologies Inc.

- Zhaoxin Semiconductor Co., Ltd.

- Tachyum s.r.o.

- Graphcore Limited

- Tenstorrent, Inc.

- SiPearl SAS

- SAPPHIRE Technology Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AI and HPC Workloads in German Data Centers

- 4.2.2 Robust PC Gaming and Esports Ecosystem in Germany

- 4.2.3 Growing Adoption of GPU-Accelerated Workstations for Professional Visualization

- 4.2.4 Energy-Efficiency Mandates Driving Upgrades to Advanced GPU Nodes

- 4.2.5 Federal Subsidies for Semiconductor Investment Under Germany's IPCEI Microelectronics Program

- 4.2.6 Industry 4.0 Edge Computing Pilots Requiring Embedded Discrete GPUs

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions and GPU Shortages

- 4.3.2 High Up-Front Cost of High-Performance GPUs

- 4.3.3 Stringent EU Environmental Regulations Increasing Lifecycle Compliance Costs

- 4.3.4 Competition from Integrated GPUs in Entry-Level Segments

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (less than 100 USD)

- 5.3.2 Mainstream GPUs (100 USD to 400 USD)

- 5.3.3 High-Performance Consumer GPUs (400 USD to 1,200 USD)

- 5.3.4 Data Center / AI Accelerator GPUs (greater than 1,200 USD)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Imagination Technologies Limited

- 6.4.5 ARM Limited

- 6.4.6 QUALCOMM Incorporated

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 HUAWEI Technologies Co., Ltd.

- 6.4.10 MediaTek Inc.

- 6.4.11 VIA Technologies Inc.

- 6.4.12 Zhaoxin Semiconductor Co., Ltd.

- 6.4.13 Tachyum s.r.o.

- 6.4.14 Graphcore Limited

- 6.4.15 Tenstorrent, Inc.

- 6.4.16 SiPearl SAS

- 6.4.17 SAPPHIRE Technology Limited

- 6.4.18 ASUSTeK Computer Inc.

- 6.4.19 Micro-Star International Co., Ltd.

- 6.4.20 Gigabyte Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment