PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072767

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072767

Spain Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

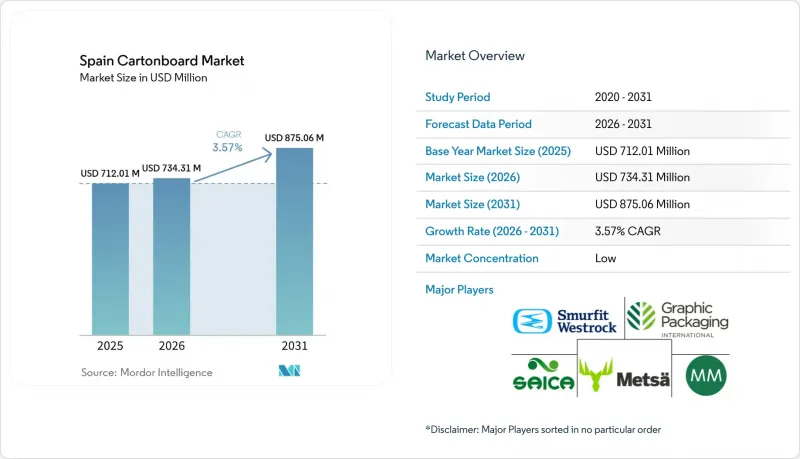

According to Mordor Intelligence, the spain cartonboard market size was valued at USD 712.01 million in 2025 and estimated to grow from USD 734.31 million in 2026 to reach USD 875.06 million by 2031, at a CAGR of 3.57% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Cartonboard Market Trends and Insights

Sustainable Packaging Substitution In Food And Beverage

The Spain cartonboard market is gaining direct support from tighter plastic packaging rules and rising producer responsibility costs for non-fiber formats. Spain's packaging framework increased pressure on brand owners to move toward recyclable packs with clearer end-of-life communication, making cartonboard a more practical commercial choice for food and beverage lines. Fresh and frozen food represented 29% of folding carton converter turnover in Spain in 2025, while beverages accounted for 21%, so substitution in these categories carries clear volume potential for the Spain cartonboard market. The December 2024 launch of the PaperSeal Shape tray in Spain showed that converters were already replacing conventional plastic trays with paperboard structures before the August 2026 compliance deadline. As more food formats shift to mono-material fiber packs, demand is growing for both premium virgin-fiber boards and recyclable retail formats in the Spanish cartonboard market. That shift favors suppliers that can provide substrate access, conversion quality, and regulatory documentation in one offer.

E-Commerce And Shelf-Ready Carton Demand

The Spain cartonboard market is also benefiting from the spread of shelf-ready packaging in retail and online fulfillment. Retailers increasingly prefer formats that protect goods in transit and move directly onto store shelves without extra handling, giving cartonboard a more functional role in logistics. This use case supports Folding Boxboard and White-Lined Chipboard formats that sit between plain transport packaging and premium retail presentation. In the Spain cartonboard market, that requirement is broadening carton use from a branded secondary pack into a tool for labor reduction and faster replenishment. It is also pulling lighter grammage boards into categories that previously used heavier structures, changing the grade mix for converters with multi-grade portfolios. The result is a more stable demand base for cartons linked to omnichannel retail rather than to store traffic alone.

Energy And Recycled-Board Cost Volatility

The Spain cartonboard market remains exposed to energy cost swings because paper and board production runs on continuous industrial schedules with limited operating flexibility. When electricity and gas prices rise, mills cannot easily reduce output in short intervals, so pressure moves quickly into margins and working capital. The recycled-fiber cost side is also important because European OCC prices stayed near EUR 120 (USD 135) per tonne in late 2025 before stabilizing closer to EUR 105 (USD 118) per tonne. That level keeps a higher cost floor in recycled grades than the market faced before 2022, which leaves less room for weaker Spanish mills in the Spain cartonboard market. Reno de Medici's closure agreement at Castellbisbal showed how prolonged cost pressure can translate into hard capacity decisions in Spain. The burden is most severe for operators without energy co-generation assets, renewable power contracts, or enough scale to pass cost moves through to customers.

Other drivers and restraints analyzed in the detailed report include:

- Processed Food And Export Packaging Growth

- Premium Secondary Packs For Pharma And Beauty

- Barrier Performance Trade-Offs Versus Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 33.14% of the Spanish cartonboard market share in 2025, making it the leading grade by volume and value. Its lead in the Spanish cartonboard market stems from broad use across secondary packs that require stiffness, surface brightness, and reliable print quality. Solid Bleached Board remained relevant in premium cosmetics and confectionery packs where a white surface finish supports premium positioning. Solid Unbleached Board served food-service and retail-ready formats where strength mattered more than high whiteness. White-Lined Chipboard continued to serve cost-sensitive cereals and processed food packs where recycled content was commercially acceptable and often preferred.

Liquid Packaging Board is projected to grow at a 4.63% CAGR through 2031, making it the fastest-moving grade in the Spanish cartonboard market. Spain's dairy, juice, and plant-based beverage base supports steady aseptic packaging demand, as these products require protection from light and oxygen. Royal Decree 1055/2022 also raised the importance of print quality from January 2025, which favored grades that can carry sorting information clearly and consistently. Food Service Board added another outlet through cups, trays, and carrier boards for out-of-home consumption, keeping the grade mix broader in the Spanish cartonboard industry. Stora Enso's new consumer packaging board line at Oulu began ramp-up in early 2025 and will widen European supply from 2027, which may ease some board availability pressure for the Spanish cartonboard market and change converter buying patterns across the Spanish cartonboard industry.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Mayr-Melnhof Karton AG

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- Saica Group

- Metsa Board Corporation

- Stora Enso Oyj

- Reno de Medici S.p.A.

- SIG Group AG

- Elopak ASA

- Huhtamaki Oyj

- Lecta, S.A.

- Holmen AB

- Billerud Aktiebolag

- Alzamora Group

- Cartondis S.A.U.

- Embalajes Vidal Albinana S.L.

- WORLD VYPMAR, S.L.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainable Packaging Substitution in Food and Beverage

- 4.2.2 E-commerce and Shelf-Ready Carton Demand

- 4.2.3 Processed Food and Export Packaging Growth

- 4.2.4 Premium Secondary Packs for Pharma and Beauty

- 4.2.5 2025 Printed Sorting-Label Compliance

- 4.2.6 Pharma Aggregation and Traceability Complexity

- 4.3 Market Restraints

- 4.3.1 Energy and Recycled-Board Cost Volatility

- 4.3.2 Barrier Performance Trade-Offs Versus Plastics

- 4.3.3 Artwork Complexity from Printed Sorting Labels

- 4.3.4 Recyclability Documentation Burden Before August 2026

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton AG

- 6.4.2 Graphic Packaging Holding Company

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Saica Group

- 6.4.5 Metsa Board Corporation

- 6.4.6 Stora Enso Oyj

- 6.4.7 Reno de Medici S.p.A.

- 6.4.8 SIG Group AG

- 6.4.9 Elopak ASA

- 6.4.10 Huhtamaki Oyj

- 6.4.11 Lecta, S.A.

- 6.4.12 Holmen AB

- 6.4.13 Billerud Aktiebolag

- 6.4.14 Alzamora Group

- 6.4.15 Cartondis S.A.U.

- 6.4.16 Embalajes Vidal Albinana S.L.

- 6.4.17 WORLD VYPMAR, S.L.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment