PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072780

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072780

India Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

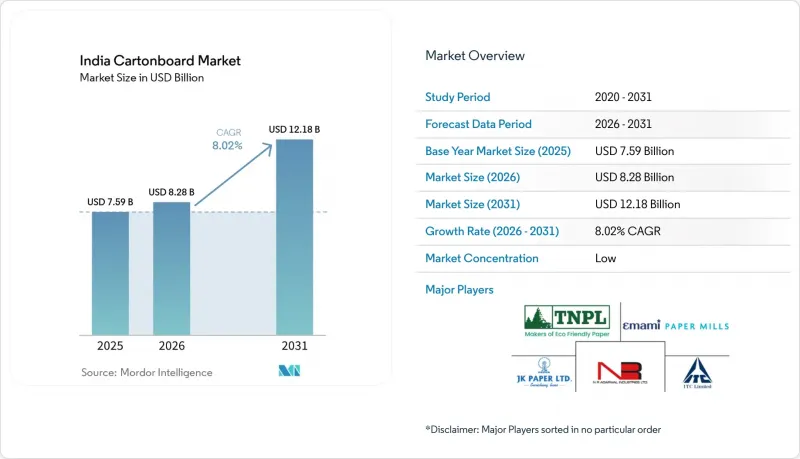

According to Mordor Intelligence, the india cartonboard market size is projected to expand from USD 7.59 billion in 2025 and USD 8.28 billion in 2026 to USD 12.18 billion by 2031, registering a CAGR of 8.02% between 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Cartonboard Market Trends and Insights

EPR-Ready Paper Packaging Compliance Advantage From 2026

The India cartonboard market is gaining support from the growing stringency of plastic compliance obligations for brand owners that rely heavily on rigid plastic formats. India's single-use plastic enforcement has already shown that regulation is not merely symbolic, as penalties collected in Delhi and Karnataka exceeded INR 198 million (USD 2.2 million) through 2024. That enforcement backdrop is pushing packaging teams to look for formats that reduce compliance friction and simplify audit trails. Cartonboard benefits by helping lower dependence on plastic in secondary packs and selected foodservice applications, which matters more as environmental reporting becomes part of commercial procurement. Mills and converters that can document supply origin, substrate quality, and customer-specific compliance are therefore improving their position in annual sourcing cycles. The India cartonboard market is also becoming more selective, as large buyers increasingly favor suppliers that can pair board performance with documentation discipline, rather than the lowest selling price.

Substitution Of Single-Use Plastics With Paperboard

The India cartonboard market is also moving higher as paper-based formats replace plastic in a wider set of everyday packaging uses. The continued enforcement of the single-use plastic ban encouraged a shift toward kraft bags, molded-fiber trays, and food-contact cartonboard in foodservice and takeaway applications. This change matters because it widens cartonboard demand beyond traditional folding cartons and brings in categories that were once served by low-cost plastic or expanded polystyrene packs. At the same time, food-contact applications require improved grease resistance, cleaner barrier performance, and greater reliability in compliance with India's packaging rules regarding migration. That is improving the demand mix for food service board and other higher-specification grades rather than only adding more recycled board volume. The India cartonboard market is therefore capturing both substitution demand and quality upgrading simultaneously, making the shift more durable than a short-term policy response.

Wastepaper, Pulp, And Energy Cost Volatility

Input cost volatility remains the most immediate operating restraint for the India cartonboard market. Hardwood pulp prices moved above USD 615 per metric tonne in early 2026, driven by supply tightness due to mill maintenance shutdowns and raw material disruptions in Indonesia. Domestic mills also faced a sharp rise in wood and recovered fiber costs, which increased raw material pressure and made it more difficult to maintain price discipline on lower-value grades. This matters most for mills that rely on imported pulp or purchased wastepaper, because they have less room to protect margins when customers resist price increases. Integrated producers are better positioned because in-house access to pulp or fiber provides them with a structural cost buffer during volatile periods. The India cartonboard market is therefore seeing a clearer split between suppliers that can absorb cost shocks through integration and those that remain more exposed to sudden changes in global fiber and energy conditions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Premiumization In Food And Pharma Folding Cartons

- Aseptic Dairy And Juice Expansion Supporting Liquid Packaging Board

- Price-Led Competition From Cheap Imports And Regional Duplex Mills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White-lined chipboard held 37.19% of the Indian cartonboard market share in 2025, which reflects the continued strength of recycled-fiber board in mass-market secondary packaging. The grade remains widely used across toys, apparel, and fast-moving consumer goods because it offers acceptable printability and cost efficiency at scale. Its position has also become more resilient because improvements in topcoats and surface treatments have narrowed part of the historical finish gap between recycled grades and premium virgin-fiber options. That allowed brand owners to maintain shelf presence while still using a lower-cost base board in many secondary applications. The India cartonboard market has therefore maintained a broad recycled-fiber foundation even as customer expectations for appearance and consistency have risen.

The food service board market is projected to expand at a 9.17% CAGR from 2026 to 2031, and this segment of the India cartonboard market is strengthening as restaurant chains, delivery platforms, and takeaway formats shift toward paper-based food packaging. Demand is rising because foodservice applications need grease resistance, migration compliance, and better forming performance than basic recycled trays can deliver under stricter packaging scrutiny. Folding boxboard and solid bleached board remain the premium end of the India cartonboard industry, serving higher-value pharmaceutical, cosmetics, and confectionery packaging where brightness, stiffness, and print performance matter more. Tamil Nadu Newsprint and Papers Limited also continued to reposition its board mix toward higher-realization folding boxboard, and its board unit reached 200,075 metric tonnes of production in FY26. Solid unbleached board still serves niche industrial and heavy-goods secondary packaging, but its role remains smaller because the strongest growth is moving toward food-contact and premium printed cartons rather than utility-heavy transport formats.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- ITC Limited

- N R Agarwal Industries Limited

- JK Paper Limited

- Tamil Nadu Newsprint and Papers Limited

- Emami Paper Mills Limited

- West Coast Paper Mills Limited

- Andhra Paper Limited

- Pakka Limited

- TCPL Packaging Limited

- Parksons Packaging Limited

- Canpac Trends Private Limited

- Borkar Packaging Private Limited

- Galaxy Offset India Pvt. Ltd.

- Pragati Pack (India) Private Limited

- Kumar Printers Pvt Ltd

- Huhtamaki India Limited

- Tetra Pak India Private Limited

- UFlex Limited

- Oji India Packaging Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Substitution of Single-Use Plastics With Paperboard

- 4.2.2 Rising Premiumization in Food and Pharma Folding Cartons

- 4.2.3 Aseptic Dairy and Juice Expansion Supporting Liquid Packaging Board

- 4.2.4 Organized Retail, E-Commerce, and Quick-Commerce Packaging Demand

- 4.2.5 EPR-Ready Paper Packaging Compliance Advantage From 2026

- 4.2.6 FSSAI-Compliant Food-Contact Paperboard Adoption

- 4.3 Market Restraints

- 4.3.1 Wastepaper, Pulp, and Energy Cost Volatility

- 4.3.2 Price-Led Competition From Cheap Imports and Regional Duplex Mills

- 4.3.3 PFAS-Free Barrier Transition Raises Qualification Costs

- 4.3.4 Flexible Packaging Still Wins in High-Barrier, Low-Cost Applications

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ITC Limited

- 6.4.2 N R Agarwal Industries Limited

- 6.4.3 JK Paper Limited

- 6.4.4 Tamil Nadu Newsprint and Papers Limited

- 6.4.5 Emami Paper Mills Limited

- 6.4.6 West Coast Paper Mills Limited

- 6.4.7 Andhra Paper Limited

- 6.4.8 Pakka Limited

- 6.4.9 TCPL Packaging Limited

- 6.4.10 Parksons Packaging Limited

- 6.4.11 Canpac Trends Private Limited

- 6.4.12 Borkar Packaging Private Limited

- 6.4.13 Galaxy Offset India Pvt. Ltd.

- 6.4.14 Pragati Pack (India) Private Limited

- 6.4.15 Kumar Printers Pvt Ltd

- 6.4.16 Huhtamaki India Limited

- 6.4.17 Tetra Pak India Private Limited

- 6.4.18 UFlex Limited

- 6.4.19 Oji India Packaging Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment