PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072776

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072776

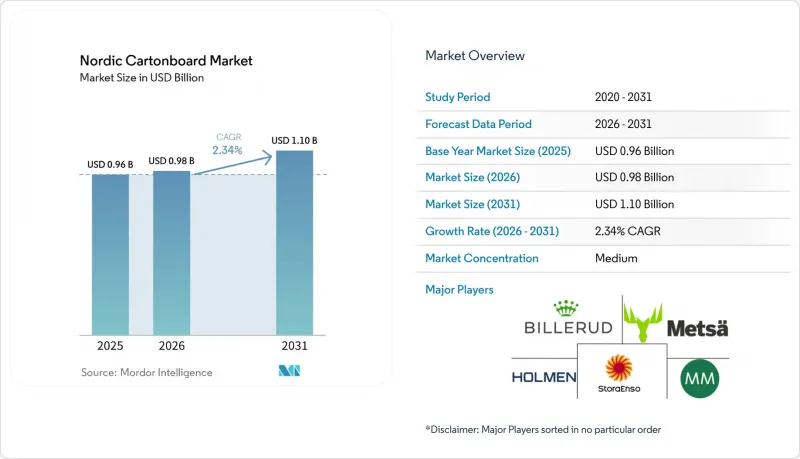

Nordic Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the nordic cartonboard market size is projected to expand from USD 0.96 billion in 2025 and USD 0.98 billion in 2026 to USD 1.10 billion by 2031, registering a CAGR of 2.34% over 2026-2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Nordic Cartonboard Market Trends and Insights

Recyclability-Ready Packaging Portfolio Shifts

The PPWR applies from August 12, 2026, and requires packaging placed on the EU market to be recyclable, making recyclability a direct commercial requirement rather than a voluntary packaging preference. In the Nordic cartonboard market, that timing has compressed decision cycles for FMCG and pharmaceutical buyers, who are now pre-qualifying recyclable carton structures before the formal application date. Demand is splitting within the same product grade because mills that can demonstrate design-for-recycling alignment are winning forward-book contracts earlier than those still adjusting barrier systems. The effect is especially visible in fresh-fiber folding boxboard and liquid packaging board, where converters want documented recyclability before they commit to new pack formats. UPM Specialty Materials and BASF formalized a collaboration in May 2026 to accelerate the adoption of recyclable fiber-based packaging by combining barrier-based papers with Joncryl HPB resin technology, demonstrating how the upstream chemical chain is moving toward fiber-compatible solutions. That progress is reducing technical hesitation across the Nordic cartonboard market and is making compliant premium grades easier to specify in commercial tenders.

Premiumization Of Fresh And Chilled Food Cartons

Fresh and chilled food categories are lifting value per unit in the Nordic cartonboard market, even though volume growth remains measured. Organic dairy, plant-based beverages, artisanal chilled foods, and convenience-led refrigerated formats all need strong print quality, food-contact reliability, and shelf appeal, in formats that still meet recycling rules. This is pushing brand owners toward fiber-based and low-emission board structures as standard purchase conditions rather than optional sustainability upgrades. The change matters because it supports better contract pricing for mills that can pair visual quality with credible environmental credentials. Elopak produced 16 billion cartons in 2025, and EMEA accounted for 69% of its revenue, which reflects the scale at which chilled and fresh liquid packaging demand is feeding into board procurement across Northern Europe. As retailers and consumer brands keep refining pack formats to align with real consumption habits, the Nordic cartonboard market continues to reward suppliers that can deliver premium grades without requiring filling-line changes.

High Nordic Energy And Fiber Input Costs

Cost pressure remains one of the clearest limits on faster expansion in the Nordic cartonboard market because board production still depends on energy-intensive assets and stable raw material sourcing. The International Energy Agency stated that the Nordic region saw fewer hours of negative-priced electricity in 2025 as battery deployment reduced excess renewable generation, meaning mills had less access to very low off-peak power than in prior periods. The same report noted that EU Emissions Trading System prices averaged EUR 75 per tonne of CO2 in 2025, which added to the operating costs of energy-intensive board machines. Internal price divergence between northern and southern bidding zones in Sweden and Norway is also creating uneven pressure across mill locations. That matters because mills near large demand centers may face a different cost profile than mills connected to lower-cost northern power zones. In the Nordic cartonboard market, this forces producers to balance energy hedging, on-site power projects, and boardline upgrades with the need to protect margins in premium product categories.

Other drivers and restraints analyzed in the detailed report include:

- Brand Migration From Plastic To Fiber Packs

- Shelf-Ready Secondary Packaging Demand

- PFAS Compliance And Reformulation Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held the largest share by product grade at 37.17% in 2025, which kept it at the center of demand across food, cosmetics, and pharmaceutical secondary packs in the Nordic cartonboard market. The segment's hold is supported by lightweighting, as producers continue to improve stiffness-to-weight performance and extend folding boxboard into uses that once leaned more heavily on solid bleached board. Solid bleached board still keeps a clear role in premium pharmaceutical packs and luxury cosmetics because those applications prioritize print quality, purity, and pack finish over cost. Metsa Board launched MetsaBoard Pro FBB Go in March 2026 as an OBA-free folding boxboard with hard sizing for frozen applications, produced at Husum in Sweden, and offered with short delivery windows across Europe.

Liquid packaging board is projected to post the fastest growth in the Nordic cartonboard market, with a CAGR of 3.19% from 2026 to 2031. That pace reflects strong demand from dairy producers and plant-based beverage brands that are redesigning cartons to increase fiber content and reduce reliance on aluminum and conventional polymers. Stora Enso launched Performa Natura Aqua in April 2026, a dispersion-coated folding boxboard for foodservice and bakery packaging that uses less plastic on the reverse side and allows faster repulping, which points to the broader direction of barrier development in the region. The food service board is also advancing as quick-service restaurants and workplace catering operators shift toward fiber-based single-material constructions that better align with national EPR and recyclability expectations.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Stora Enso Oyj

- Metsa Board Corporation

- Billerud Aktiebolag (publ)

- Holmen AB

- Mayr-Melnhof Karton AG

- MM Kotkamills Boards Oy

- Fiskeby Board AB

- Pankaboard Oy

- Elopak ASA

- Walki Group Oy

- Huhtamaki Oyj

- Graphic Packaging International, LLC

- Smurfit Westrock plc

- DS Smith Plc

- Sonoco Products Company

- FrontPac AB

- Moltzau Packaging AS

- Tetra Pak International S.A.

- Sappi Europe SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Recyclability-Ready Packaging Portfolio Shifts

- 4.3.2 Premiumization of Fresh and Chilled Food Cartons

- 4.3.3 Brand Migration From Plastic to Fiber Packs

- 4.3.4 Shelf-Ready Secondary Packaging Demand

- 4.3.5 PFAS-Free Barrier Innovation Adoption

- 4.3.6 Nordic Oat and Dairy Alternative Pack Expansion

- 4.4 Market Restraints

- 4.4.1 High Nordic Energy and Fiber Input Costs

- 4.4.2 PFAS Compliance and Reformulation Risk

- 4.4.3 Composite Liquid Carton Recycling Gaps

- 4.4.4 Supplier Base Rationalization by Large FMCG Buyers

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Stora Enso Oyj

- 6.4.2 Metsa Board Corporation

- 6.4.3 Billerud Aktiebolag (publ)

- 6.4.4 Holmen AB

- 6.4.5 Mayr-Melnhof Karton AG

- 6.4.6 MM Kotkamills Boards Oy

- 6.4.7 Fiskeby Board AB

- 6.4.8 Pankaboard Oy

- 6.4.9 Elopak ASA

- 6.4.10 Walki Group Oy

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Graphic Packaging International, LLC

- 6.4.13 Smurfit Westrock plc

- 6.4.14 DS Smith Plc

- 6.4.15 Sonoco Products Company

- 6.4.16 FrontPac AB

- 6.4.17 Moltzau Packaging AS

- 6.4.18 Tetra Pak International S.A.

- 6.4.19 Sappi Europe SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment