PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072803

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072803

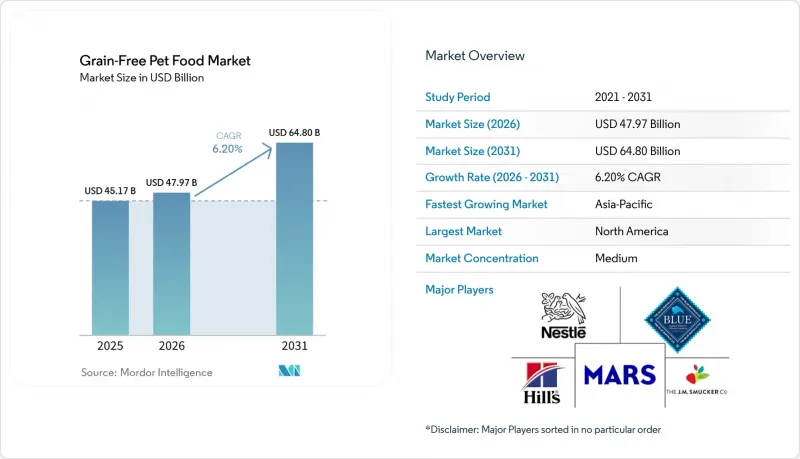

Grain-Free Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the grain-free pet food market is projected to grow from USD 45.17 billion in 2025 and USD 47.97 billion in 2026 to USD 64.80 billion by 2031, registering a CAGR of 6.2% between 2026 and 2031.

This report is Segmented by Product Type (Dry Kibble, Wet Food, Treats and Snacks, Freeze-Dried and Raw Formats, and More), by Pet Type (Dogs, Cats, Other Pets), by Ingredient Source (Animal-Based Proteins, Plant-Based Proteins, Insect and Alternative Proteins, and More), and by Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Grain-Free Pet Food Market Trends and Insights

Pet Humanization Fueling Premium Nutrition Spend

Households increasingly treat companion animals as family members, steering purchasing toward premium, grain-free recipes aligned with human clean-eating values. Millennials and Generation Z prioritize traceable supply chains and ethical sourcing, rewarding brands that demonstrate transparency through certifications and sustainability initiatives. According to the American Pet Products Association (APPA), total United States pet industry expenditure increased from USD 152 billion in 2024 to USD 158 billion in 2025, reflecting rising premiumization . Smaller family sizes and delayed parenthood further channel discretionary income into pets, while demand for limited-ingredient and single-protein diets continues to grow, reinforcing the grain-free segment's expansion.

Increasing Diagnosis of Grain Allergies/Intolerances

Advancements in diagnostic methods are enhancing the detection of food-related intolerances in pets, driving demand for grain-free diets. The Merck Sharp & Dohme Corp. (MSD) Veterinary Manual states that food allergies in animals are primarily identified through elimination diet trials, which involve removing and reintroducing specific ingredients to pinpoint triggers. This approach often promotes the use of simplified, limited-ingredient diets, including grain-free options, to isolate potential sensitivities. As veterinarians increasingly utilize dietary trials for diagnosis, pet owners are turning to grain-free pet food as an effective solution for managing suspected intolerances, thereby contributing to the growth of the grain-free pet food market.

United States Food and Drug Administration (FDA) Scrutiny Over Dilated Cardiomyopathy Link

Regulatory scrutiny continues to impact the grain-free pet food market due to ongoing concerns regarding canine heart health. As of 2024, the United States Food and Drug Administration (FDA) is still investigating reports of non-hereditary Dilated Cardiomyopathy (DCM) associated with both grain-free and grain-inclusive diets. This uncertainty has led to increased caution among veterinarians and pet owners, particularly for dog breeds considered at higher risk. Consequently, consumers are more likely to seek professional advice before selecting grain-free products, while manufacturers are modifying formulations and marketing strategies. These factors collectively reduce consumer confidence and hinder the wider adoption of grain-free pet food.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Online Direct-to-Consumer Channels

- Premiumization Toward High-Protein Clean-Label Diets

- Higher Raw-Material and Production Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry kibble accounted for the largest 40% of the grain-free pet food market share in 2025, driven by factors such as convenience, affordability, and extended shelf life. Its widespread retail availability and familiarity among consumers continue to support its dominance, particularly in cost-sensitive regions. However, shifting consumer preferences toward minimally processed nutrition are gradually increasing demand for premium formats. Wet food is gaining popularity, especially among aging pets and cats that require hydration support, while treats and snacks benefit from impulse purchasing behavior. Emerging formats, including air-dried and gently cooked products, are gaining niche acceptance in developed markets.

Freeze-dried and raw formats are projected to grow at the fastest 11.4% CAGR from 2026 to 2031, driven by rising demand for high-protein and minimally processed diets. These formats align with trends in pet humanization and advancements in cold-chain logistics. Manufacturers are expanding production capacities and introducing hybrid offerings that combine fresh and freeze-dried components. However, regulatory requirements related to food safety and pathogen control are increasing compliance costs, particularly for smaller manufacturers. Regional adoption varies significantly, with developed markets leading due to superior infrastructure, while developing regions remain dominated by dry formats due to cost constraints.

Complete Report Scope:

- By Product Type

- Dry Kibble

- Wet Food

- Treats and Snacks

- Freeze-Dried and Raw Formats

- Others

- By Pet Type

- Dogs

- Cats

- Others

- By Ingredient Source

- Animal-Based Proteins

- Plant-Based Proteins

- Insect and Alternative Proteins

- Mixed-Ingredient Formulations

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America commanded the largest 42% of the grain-free pet food market share in 2025, supported by high pet ownership rates and strong consumer spending on premium pet nutrition. The region benefits from a well-developed retail infrastructure, including specialty stores and e-commerce platforms, which enhance product accessibility. Growing consumer awareness of ingredient quality and pet health continues to fuel demand for grain-free formulations. Innovation in premium formats, such as freeze-dried and fresh pet food, is particularly notable, supported by established cold-chain logistics and strong veterinary engagement.

Asia-Pacific is projected to grow at the fastest 8.7% CAGR from 2026 to 2031, driven by rising pet ownership and increasing disposable incomes. Urbanization and evolving lifestyles are contributing to greater demand for premium pet food products. Digital commerce plays a significant role in market expansion, enabling brands to reach a broader consumer base. Countries such as China, Japan, and South Korea are leading in adoption, while emerging economies are gradually entering the premium segment. Consumer education and affordability remain critical factors influencing adoption rates across the region.

Europe maintains a balance between market size and growth through stringent labeling regulations, sustainability initiatives, and strong consumer demand for premium pet nutrition products. Germany, France, the United Kingdom, Italy, and Spain remain the largest regional consumption centers for grain-free pet food products. In October 2025, Farmina invested BRL 45 million (USD 7.7 million) to expand its distribution capacity in Brazil, enhancing international logistics and export capabilities to support broader pet food supply chains. The Middle East continues to generate demand for premium products, driven by affluent consumers seeking sustainable and specialized pet diets, while Africa represents an emerging market supported by urbanization and gradually increasing pet ownership trends.

- Nestle Purina PetCare Company

- Mars, Incorporated

- Hill's Pet Nutrition, Inc.

- The J. M. Smucker Company

- Blue Buffalo Company, Ltd. (General Mills, Inc.)

- Diamond Pet Foods, Inc. (Schell & Kampeter, Inc.)

- WellPet LLC

- Midwestern Pet Foods, Inc.

- Farmina Pet Foods Holding B.V.

- Heristo Aktiengesellschaft

- Tiernahrung Deuerer GmbH

- Unicharm Corporation

- Freshpet, Inc.

- Agrolimen S.A.

- Canidae Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pet humanization fueling premium nutrition spend

- 4.2.2 Increasing diagnosis of grain allergies/intolerances

- 4.2.3 Rapid expansion of online direct-to-consumer channels

- 4.2.4 Premiumization toward high-protein clean-label diets

- 4.2.5 Veterinary therapeutic adoption of grain-free formulas

- 4.2.6 Cost declines from insect and single-cell proteins

- 4.3 Market Restraints

- 4.3.1 United States Food and Drug Administration (FDA) scrutiny over dilated cardiomyopathy link

- 4.3.2 Higher raw-material and production costs

- 4.3.3 Intense competitive price pressure

- 4.3.4 Limited availability of starch-free extrusion capacity

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Dry Kibble

- 5.1.2 Wet Food

- 5.1.3 Treats and Snacks

- 5.1.4 Freeze-Dried and Raw Formats

- 5.1.5 Others

- 5.2 By Pet Type

- 5.2.1 Dogs

- 5.2.2 Cats

- 5.2.3 Others

- 5.3 By Ingredient Source

- 5.3.1 Animal-Based Proteins

- 5.3.2 Plant-Based Proteins

- 5.3.3 Insect and Alternative Proteins

- 5.3.4 Mixed-Ingredient Formulations

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Nestle Purina PetCare Company

- 6.4.2 Mars, Incorporated

- 6.4.3 Hill's Pet Nutrition, Inc.

- 6.4.4 The J. M. Smucker Company

- 6.4.5 Blue Buffalo Company, Ltd. (General Mills, Inc.)

- 6.4.6 Diamond Pet Foods, Inc. (Schell & Kampeter, Inc.)

- 6.4.7 WellPet LLC

- 6.4.8 Midwestern Pet Foods, Inc.

- 6.4.9 Farmina Pet Foods Holding B.V.

- 6.4.10 Heristo Aktiengesellschaft

- 6.4.11 Tiernahrung Deuerer GmbH

- 6.4.12 Unicharm Corporation

- 6.4.13 Freshpet, Inc.

- 6.4.14 Agrolimen S.A.

- 6.4.15 Canidae Corporation

7 Market Opportunities and Future Outlook