PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073271

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073271

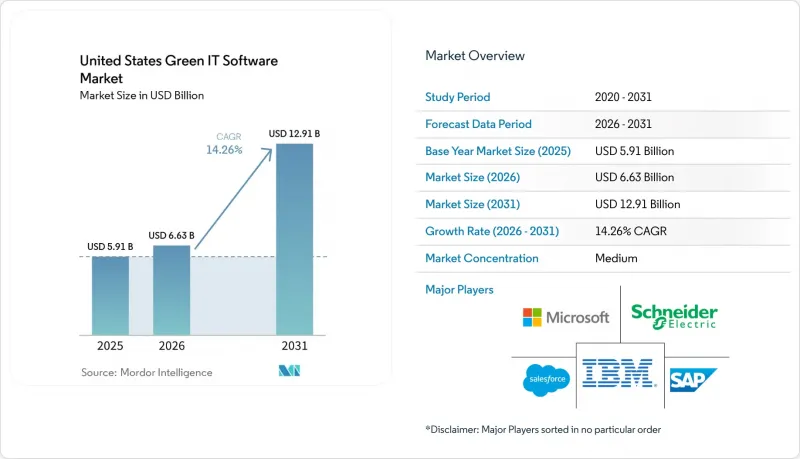

United States Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states green IT software market size is expected to increase from USD 5.91 billion in 2025 to USD 6.63 billion in 2026 and reach USD 12.91 billion by 2031, growing at a CAGR of 14.26% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, and More), Solution Type (Carbon Management and Accounting Software, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Information Technology and Telecommunications, Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Green IT Software Market Trends and Insights

Regulatory Pressure for Scope 1 To Scope 3 Reporting Automation

California has become the clearest near-term trigger for enterprise buying in the United States green IT software market because CARB adopted initial implementing regulations for SB 253 on February 26, 2026, and set August 10, 2026 as the first disclosure deadline for Scope 1 and Scope 2 emissions for covered companies doing business in the state. The law reaches beyond companies headquartered in California because the revenue threshold applies to firms that do business in the state, which widens the addressable buyer base across sectors and operating regions. Scope 3 obligations will activate from 2027, so many buyers are acting in 2026 because supplier data systems, controls, and internal review processes take time to build and test at audit-ready quality. This timing is lifting demand for software that can manage emissions inventories, supplier submissions, evidence trails, and framework-ready outputs in one controlled environment. The SEC's proposal to rescind its climate-related disclosure rules in May 2026 has not removed the underlying need for repeatable reporting systems among large enterprises that still face disclosure expectations from investors, lenders, customers, and boards. Vendors that align workflows with accepted emissions accounting practices and verification requirements are therefore gaining ground because buyers want tools that remain usable across both mandatory and voluntary reporting settings.

Enterprise AI Shift Toward Continuous Sustainability Intelligence

AI is shifting the value of the United States green IT software market from simple data collection toward software that can monitor, interpret, and organize sustainability information on a continuous basis. Salesforce launched Agentforce for Net Zero Cloud in June 2025 with AI agents that can draft disclosure content, monitor Scope 1, Scope 2, and Scope 3 inventories, and surface issues during the reporting cycle rather than after it closes. SAP stated in May 2026 that its sustainability AI agents will reach general availability by the end of 2026 and will support side-by-side decarbonization scenario work while addressing the variability found in average emissions factors. This changes buyer expectations because sustainability teams no longer want software that only stores past-period data. They want systems that can flag data gaps, compare scenarios, compress reporting timelines, and support internal decision-making during the year. The advantage is moving toward vendors that can combine AI functions with governance controls, traceability, and integration into finance and operating systems, because those features reduce manual effort without weakening audit discipline.

High Integration Complexity With Legacy ERP and Facility Systems

Integration remains the clearest operational barrier in the United States green IT software market because core sustainability data still originates inside older ERP, procurement, facility, and building systems that were not designed for emissions reporting. Many buyers must connect several transactional systems before they can produce usable carbon calculations or disclosure-ready records, and that work can stretch implementations and raise total cost. Oracle launched Oracle Fusion Cloud Sustainability in September 2024 inside its existing Fusion Cloud Applications Suite, which directly addresses this issue by embedding data capture and reporting functions within software environments that already hold enterprise transactions. IBM's Envizi Supply Chain Intelligence also targets this problem by connecting ERP transactions to Scope 3 calculations and by prioritizing supplier-specific data over broad averages where better source data exists. Even with these improvements, data quality and system compatibility still vary widely across buyer environments, which means integration effort remains a real brake on adoption speed. This restraint gives a durable advantage to vendors that control the ERP layer or have strong pre-built connectors, because buyers want shorter implementation cycles and fewer external data handoffs.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Native Carbon and Energy Optimization Adoption in Data Center Workloads

- Procurement Requirements Linking Software Selection to Verified ESG Data

- Weak Supplier Data Quality Slowing Scope 3 Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are projected to grow at a 19.26% CAGR through 2031, which makes them the fastest-expanding part of this segmentation in the United States green IT software market. That growth reflects the need for implementation support, data architecture work, reporting design, and change management as disclosure obligations become more detailed. Many large buyers still need outside help to connect emissions workflows with ERP, procurement, and facility data before the software can operate at scale. Services also remain relevant because supplier-data programs, assurance preparation, and internal governance processes often require sustained support after initial implementation. At the same time, software held 46.41% of revenue in 2025, which shows that licensed platforms still anchor how enterprises govern sustainability data and reporting programs.

Software remains the installed-base core because the control layer, workflow logic, and evidence management all sit inside the product rather than inside a consulting engagement. Workiva introduced Intelligent Finance, GRC, and Sustainability in September 2025 with AI-enabled automation for disclosure drafting, benchmarking, materiality work, peer comparison, and compliance workflows, which shows how vendors are expanding software value even as services demand stays strong. As automation improves, service spend is likely to shift away from repetitive assembly work and toward higher-value areas such as governance setup, decarbonization planning, and assurance readiness. That pattern helps explain why services are growing quickly without displacing software as the larger revenue base. The United States green IT software industry is therefore evolving toward combined software and delivery models rather than a pure license-only structure.

Cloud-based deployment accounted for 63.94% of revenue in 2025 and is projected to grow at a 16.12% CAGR through 2031, which leaves it as both the largest and fastest-growing deployment model in the United States green IT software market. This dual position shows that buyer preference is consolidating around cloud-native sustainability architecture rather than moving through an early transition stage. Large enterprises need continuous synchronization across business units, geographies, and reporting frameworks, and cloud environments make that easier than isolated on-premise systems. Cloud deployment also supports the always-on data feeds that AI-enabled sustainability functions require for anomaly detection, scenario work, and in-cycle review. For that reason, cloud adoption is now tied as much to workflow design and system interoperability as it is to hosting choice.

IBM's January 2026 Excel add-in for Envizi Emissions Calculations shows how cloud-based sustainability tools can be inserted into established user workflows instead of forcing users into a separate operating environment. IBM also released ESRS Omnibus framework configurations in February 2026 inside Envizi Sustainability Reporting Manager, which reflects the advantage of managed cloud frameworks that can be updated as standards evolve. On-premise deployment still has a role in more regulated settings where data residency and infrastructure control remain important. Hybrid models are also relevant where companies want cloud analytics but need tighter control over selected employee, financial, or operational datasets. One sentence with direct scale relevance is that cloud-based deployment held 63.94% of the United States green IT software market size in 2025, which confirms that deployment leadership already sits with scalable hosted models.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- IT and Telecommunications

- Manufacturing

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Energy and Utilities

- Healthcare and Life Sciences

- Retail and E-Commerce

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- Salesforce, Inc.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Schneider Electric SE

- Oracle Corporation

- Workiva Inc.

- Diligent Corp.

- Wolters Kluwer N.V.

- Persefoni AI, Inc.

- Watershed Technologies, Inc.

- EcoVadis SAS

- Intelex Technologies ULC

- Sphera Solutions, Inc.

- Benchmark Gensuite LLC

- FigBytes Inc.

- Measurabl, Inc.

- Cority Software Inc.

- Dakota Software Corporation

- EnergyCAP, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Pressure for Scope 1 to Scope 3 Reporting Automation

- 4.2.2 Cloud Native Carbon and Energy Optimization Adoption in Data Center Workloads

- 4.2.3 Enterprise AI Shift Toward Continuous Sustainability Intelligence

- 4.2.4 Procurement Requirements Linking Software Selection to Verified ESG Data

- 4.2.5 Utility Price Volatility Increasing Demand for Consumption Optimization

- 4.2.6 Fragmented Multi-Framework Reporting Burden Across Public and Private Firms

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity With Legacy ERP and Facility Systems

- 4.3.2 Weak Supplier Data Quality Slowing Scope 3 Automation

- 4.3.3 Cybersecurity and Data Residency Concerns for ESG Data Platforms

- 4.3.4 Budget Sensitivity Among Mid-Market Buyers Despite Compliance Need

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Solution Type

- 5.3.1 Carbon Management and Accounting Software

- 5.3.2 ESG Reporting and Compliance Software

- 5.3.3 Sustainability Data Management Platforms

- 5.3.4 Decarbonization Planning Software

- 5.3.5 Energy and Resource Optimization Software

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Manufacturing

- 5.5.3 Banking, Financial Services, and Insurance (BFSI)

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Retail and E-Commerce

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Salesforce, Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 SAP SE

- 6.4.5 Schneider Electric SE

- 6.4.6 Oracle Corporation

- 6.4.7 Workiva Inc.

- 6.4.8 Diligent Corp.

- 6.4.9 Wolters Kluwer N.V.

- 6.4.10 Persefoni AI, Inc.

- 6.4.11 Watershed Technologies, Inc.

- 6.4.12 EcoVadis SAS

- 6.4.13 Intelex Technologies ULC

- 6.4.14 Sphera Solutions, Inc.

- 6.4.15 Benchmark Gensuite LLC

- 6.4.16 FigBytes Inc.

- 6.4.17 Measurabl, Inc.

- 6.4.18 Cority Software Inc.

- 6.4.19 Dakota Software Corporation

- 6.4.20 EnergyCAP, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Assessment